So much for treading water until Thursday and Fridays economic reports–equities are ripping with the S&P500 up 1.27% right now.

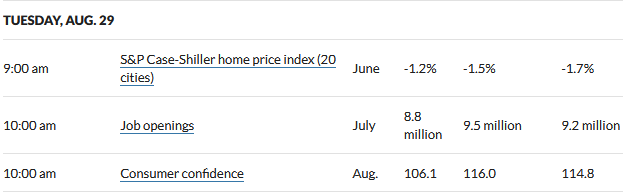

Along with equities ripping interest rates are tumbling pretty good as the consumer confidence numbers came in soft this morning and the Case Shiller home price index remains on the negative side of pricing–but slightly better than forecast. Right now the 10 year treasury is at 4.11% – down 10 basis poits on the day.

The job openings and labor turnover report (JOLTS) showed just 8.8 million jobs open right now – which while plenty high is a fair drop from 9.2 million last month and a forecast of 9.5 million.

Any report on employment is likely to get the FEDs attention – they absolutely want to see soft employment numbers – I am convinced it is 1 of just a handful of numbers that the FOMC committee wants to see soft as they are convinced inflation can’t be tamed without employment softening.