I continue to add mid level quality preferreds to our portfolios–some might say low quality for some of the issues–it is starting to feel like the ‘olden days’ after tending toward higher quality issues for the last 9 months. I will continue to hold plenty of dry powder–around 20 to 25%.

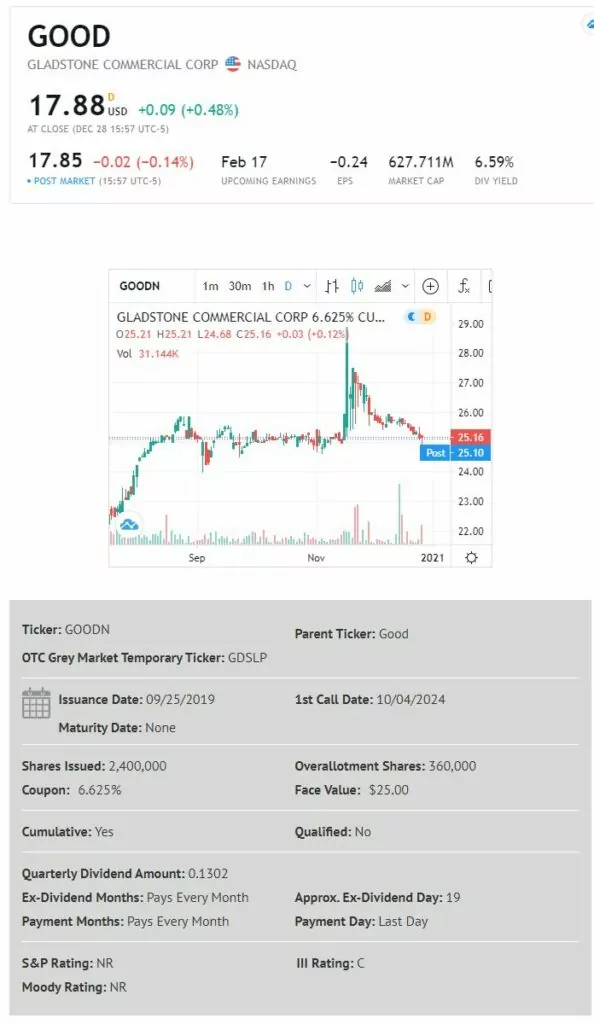

Today I added a 1/2 position in the Gladstone Commercial (GOOD) 6.625% monthly paying, cumulative, perpetual preferred (GOODN)

Gladstone Commercial is a triple net lease REIT focused office and industrial properties. I am not impressed by their financials, but they do cover their $1.50/share common stock dividend, which gives a nice level to safety for preferred shares. They have collected 99% of their lease payments in the most recent months–but personally one has to wonder about the future with ‘work from home’ likely to cut into office demand to some level.

The companies most recent earnings release can be read here.

These preferred shares trade up last month–a bunch, but now are back down to earth–seems like a good time to put a few shares in the portfolio.

Just a note that the REIT has a 7% issue outstanding (GOODM) as well which is trading at the same level as the 6.625% issue . An investor could well purchase this issue, but it has call protection only until 5/21 so the holding could be short term if bought–but either if fine.