Nothing pre market today indicated that the S&P500 would be lower by 2.70% (right now), but markets are taking the administration seriously about getting rid of Fed Chairman Powell.

At about 9:40 a.m. (central) DJT tweeted–

“Preemptive Cuts” in Interest Rates are being called for by many. With Energy Costs way down, food prices (including Biden’s egg disaster!) substantially lower, and most other “things” trending down, there is virtually No Inflation. With these costs trending so nicely downward, just what I predicted they would do, there can almost be no inflation, but there can be a SLOWING of the economy unless Mr. Too Late, a major loser, lowers interest rates, NOW. Europe has already “lowered” seven times. Powell has always been “To Late,” except when it came to the Election period when he lowered in order to help Sleepy Joe Biden, later Kamala, get elected. How did that work out?

And down equities go–more.

We can debate Powell all day long–good or bad–but these tweets could be ended, although that is not going to happen. In the end the uncertainty is what drives the markets and we have plenty of that to go around.

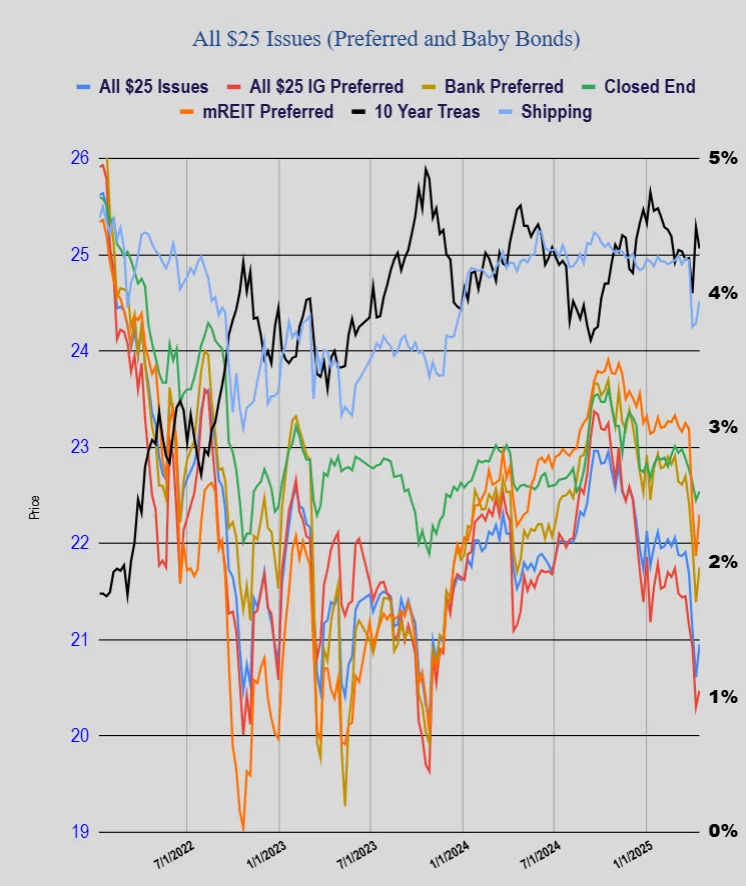

Interest rates are really not moving on DJT tweets–but right now the 10 year yield is up about 4-5 basis points. Preferreds and baby bonds are ever so slightly red–but really hardly moving. Let’s see what the afternoon brings.