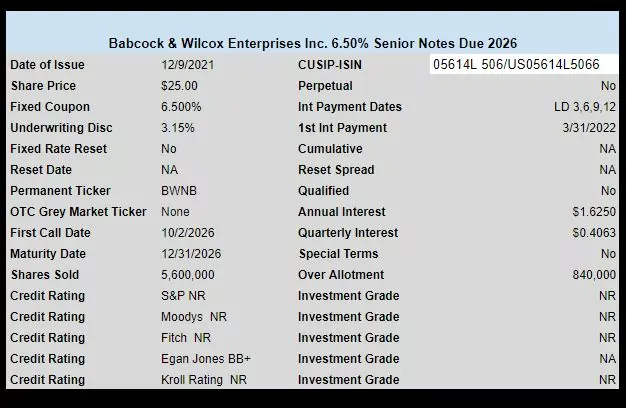

Babcock & Wilcox Enterprises (BW) has priced their previously announced senior note offering.

The issue prices at 6.50% for 5.6 million shares (bonds) with another 840,000 available for over allotment.

The issue carries a BB+ rating from Egan Jones.

The issue will have a maturity date of 12/31/2026. An optional redemption period is available to the company starting on 10/2/2026

There will be no OTC trading. The permanent ticker will be BWNB when it begins trading on NASDAQ in a week or so.

The pricing term sheet can be found here.

BWNB begins trading today

24.73

Not impressed with the Balance Sheet…Declining revenue and negative cash flow for the last 5 years and close to 1B in debt. Small current cash position as well. May need the $$$ to stay afloat and can’t issue anymore common. I’m staying away!

Got a good sale on the last issue with new contracts coming in at that time. Won’t wade in here either.

BW-A looks better. Is having a redemption date worth a full 1%? Plus dividends are Unqualified so it’s 1.5 to 2% in a taxable account.

Looks like about a .714% advantage for BW-A (@25.50), using their call dates- per Fidelity’s calculator, unless I messed up

Based on yield to call though it doesn’t account for accumulated dividends stripped price isn’t much above 25. No argument if a maturity date is that important to some people , I’m just giving my view.

Even better with the accumulated div– like it.

thx

Today I got BW-A at par $25 plus .40 accumulated dividends. Why do I feel like I just got hosed?

Right on cue, BWSN trading at $26 with a big seller showing up.

From all indications, 8.125% BWSN is toast on 3/1/22 at $25.75 + interest. BW would be crazy not to pay that off with the 162.5 basis points garnered on this BWNB “refinancing”. The share count of both issues is the same (6.4 million). This is nearly $3 million annually in lower interest costs.

Probably- although, they didn’t say the new one would go toward a call. Maybe they have enough $ besides the new one- playing it cool for some reason?

Rob – Not that I disagree with the potential likelihood of BWSN’s fate, but your case overstates the economics dramatically once you take into account the .75 premium needed to be paid to call BWSN and the 3.15% discount to par eaten up by issuance costs for that 6.50% new coupon. In other words, 6.50% to the investor is much higher than 6.50% cost to BW, but then again same goes for BWSN issue for them too… There are also accounting concerns that always come into play when an issue is called which all go on the books as losses in the year taken…. not that I’m an expert on any part of the accounting but I do know that calling normally shows up as a loss generator in the year of call due to such things as having to account for amortized costs etc., and that might not be something BW would be interested in doing… I think the normal rule of thumb is that there has to be between 75 and 100 basis of coupon saving to make a call economical and that’s when the call is at par, NOT at a premium, so I think the savings for a call, though still there, might not be that dramatic, particularly when the new issue didn’t do much in the way of extending debt payments for a low grade company like BW [“low grade” not meant to be a dig, but a way of defining a company that might benefit from extending its scheduled debt and also sensitive to loss generating events]. For the record, I do own BWSN

2WR:

Understood. Have to balance one-time earnings hit versus recurring lower quarterly interest expense.

Since BW is a RILY-sponsored outfit, we can probably expect many quarters and feet-dragging before they actually announce a redemption! Also own BWSN, but not buying any more at current prices.

I’m in the boat rowing right behind you, Rob…. own BWSN, not buying any more and on the fence on the new one……

Thanks, Tim.

In the table, “Maturity Date” says “None”.

By the way, they can redeem it at any time prior to the 1st call date of 10/2/2026:

“On any date prior to October 2, 2026 (the “Par Call Date”), the Issuer may, at its option, redeem the Notes for cash, in whole or in part, at any time or from time to time, at a redemption price equal to (i) 100% of the principal amount of the Notes to be redeemed, plus (ii) a Make-Whole Amount (as defined in the preliminary prospectus supplement, dated December 6, 2021), if any, plus (iii) accrued and unpaid interest to, but excluding, the date of redemption.”

Thanks mbg