UPDATE–OTC grey market ticker is BWCXP

Babcock & Wilcox Enterprises (BW) has priced the previously announced preferred stock.

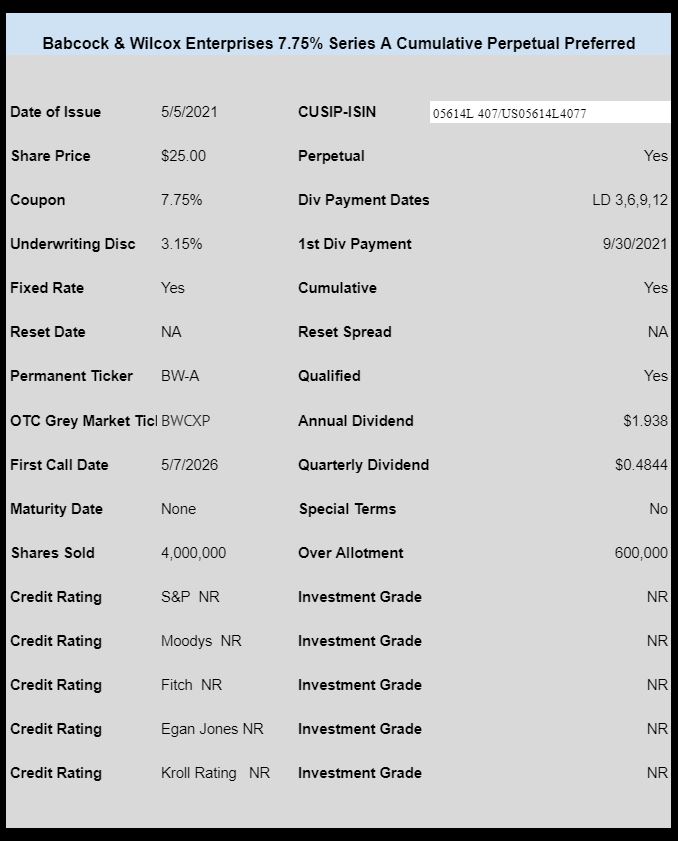

The issue prices at 7.75%. The issue is unrated, cumulative and will be qualified if the company has income (if a company does not have income dividends are generally classified as ‘return of capital’).

Thus far no OTC grey market ticker has been announced–I would expect one to be announced today.

CAUTION–at the time of the filing of the preliminary prospectus the company had NO ability to pay preferred stock dividends because of various covenants in debt agreements. Here is the preliminary prospectus again with this info–3rd paragraph from the top. BW is currently negotiating with lenders on this item, BUT if they are not successful they will not be able to pay cash dividends.

The pricing term sheet is here.

A tangled web, at the very least. One to avoid, methinks.

We should give them some credit for truth in advertising.

🙂

Happily Long BWSN

Greg–of course no one reads the prospectus except all the smart folks on this site.

or we should give their lawyers credit for educating them about securities fraud.

There seems to be so much self dealing going on here that it’s nigh impossible to follow the bouncing ball. B. Rily Securities, a sub of B. Rily Financial, [RILY], Babcock&Williams Enterprises’ largest shareholder, is underwriting this thing, and yet the A&R Credit Agreement that needs to be negotiated in order for dividends to paid on this is with B. Rily Financial (RILY) in the first place. That makes me wonder why would they choose to come to market with this BEFORE negotations are completed with themselves… Given RILY has been on such a tear itself lately, I’d have to think there’s no way they would put their name on the chopping block by underwriting this thing without essentially knowing there will be a positive end to the negotiation, but personally, I’m not coming close to this issue… passed on BWSN as well

2wr–so the question is given the extreme low quality of this issue will folks buy the issue? I will be curious to see how this trades.

Tim – that may be a question to be asked of Mr. Barnum – P T, that is…. lol. Still, it feels as though there is so much at stake for RILY underwriting this thing that at least in the short term, the likelihood of it working out is higher than would appear in the 3rd paragraph of the prospectus. Right now, my 7 3/4% type money is in RC-D and BRG-C, but as per my usual bent for stories that should work themselves out in a short time period, with the expectation that neither one will be a long term play… I suppose you could say the same thing for BW-A in a way, but comparatively speaking, imho, with a much higher degree of credit risk.

2wr–I have been a bit surprised about all the self dealing deals RILY has been doing. Bryant Riley seems to be a bit on the gamblers edge. He has been involved in many deals which, at least on paper (their financials) have worked out great. I have been searching for some super aggressive accounting, but don’t think those things will pop up until we go to recession (are areal recession–not a covid recession).

Tim – Can’t say I disagree, but for now I have hitched my wagon to this star and have owned the equity since Feb ’17 and have played the notes in increasing amounts all along. But as per usual, with an eye more toward doing them one by one, with attention on the shorter maturities, not the highest yield of any persuasion… right now I own RILYG in anticipation of the call and RILYH. Unquestionably Bryant has a lot of riverboat gambler in his blood but he also tends to back that up with an esoteric mix of what should be steady revenue generators for the firm under any economic scenarios… I do like that approach but do keep a careful watch. It’s not all been cookies and crearm though as I also took a flyer on their EOSE and though that may have been a trader’s dream to trade actively, for the buy and hold approach it’s been a dud so far…When I take these flyers, it’s alway with a tiny starter amount in anticipation of it going down, so theoretically I should be thrilled with EOSE ability to be getting closer to allowing me in for more… yippie

Tim, this is an important lesson for anyone that would buy preferreds. There is NOTHING too junky, too incestous, too risky NOT to bring to market. There will be a buyer at some price. As the saying goes: “there are no bad bonds, only bad prices.” IMO, it will be sold out on IPO. Stated differently, the Investment Banks that bring these issues to market are NOT your friend.

Agree Tex the 2nd

Tex – they are not your friends and never have been. In theory, as underwriters, they vet deals and keep the bad ones from getting to market but at the end of the day money talks. One would think underwriters would have concern for their reputation if their deals tank frequently but memories are very short and they depend on that.

A good read:

https://www.amazon.com/Where-Are-Customers-Yachts-Street/dp/0471770892/ref=sr_1_1?dchild=1&keywords=where+are+the+customers+yachts&qid=1620247894&sr=8-1

PS – I say the same about government. It’s not your friend.

My days in high-yield go all the way back to Michael Milken and Drexel, don’t think I’ve ever seen an issue with that type of clause. Similar to payment-in-kind. This is actually great for BW as far as improving their chances of survival, their stock has gone from $2.50 to $9.00. Kind of like the zombies in “I Am Legend” that begin to evolve!

I worked in the workout area of Drexel in Beverly Hills. We worked with issuers that had trouble in servicing their debt. We had a shark’s head on the wall and used to put preliminary prospectuses in the shark’s mouth to predict future trouble for the issuer. Remember Simmons’ “Burning Bed” issue? (Drexel’s solution to our predictions was to remove us from the circulation list for preliminary debt prospectuses.) Given the flow of challenged preferred issuers, another shark’s head might be appropriate around here?

Ha. We could have had a chance to work together then, Potter. Back in the day, Drexel came knocking on my door looking to recruit me to MM’s Beverly Hill’s den, but at the time, we were long 2 houses on LI, having just moved but had no buyer in sight for the house we were leaving, so we passed… I’ve always wondered what might have been had we picked up and gone Left Coastal.

The last year was awful. If the government hadn’t put Drexel under, the market would have because there were so many bad issues. The joke got to be to be sure that the proceeds were large enough to cover two years of debt service.

Dang, you folks have really been around the block a few times! To some of our younger III readers, Michael Milken and Drexel Burnham Lambert revolutionized the bond markets. They basically created a whole new market segment where high risk companies could issue “junk bonds.” Milken and his team managed to find buyers for all of the junk. Prior to Milken, traditional Wall Street banks would NOT float new bonds for junky companies like that. Fast forward to this offering from Babcock & Wilcox. It would have been a proud offering by Milken. . .

BWCXP

Hurry on down!

If this is not proof that the world of preferreds is gone nuts nothing will be.

7.75% (maybe/ maybe not will be paid) just a few months after they issued 5 year senior notes at 8.125%. No thanks.

Bizzarro world. Presumably it is a done deal that the dividend payment restriction will be lifted before issuance, but its crazy to even come to market with such a clause out there. And the interest differential with the senior notes you pointed out is crazy too. Could be a sign of a top in these bubble-licous markets.

Rvert–correct.

Insanity.

Such a good deal, that the offering was upsized form $50 to $100 million!