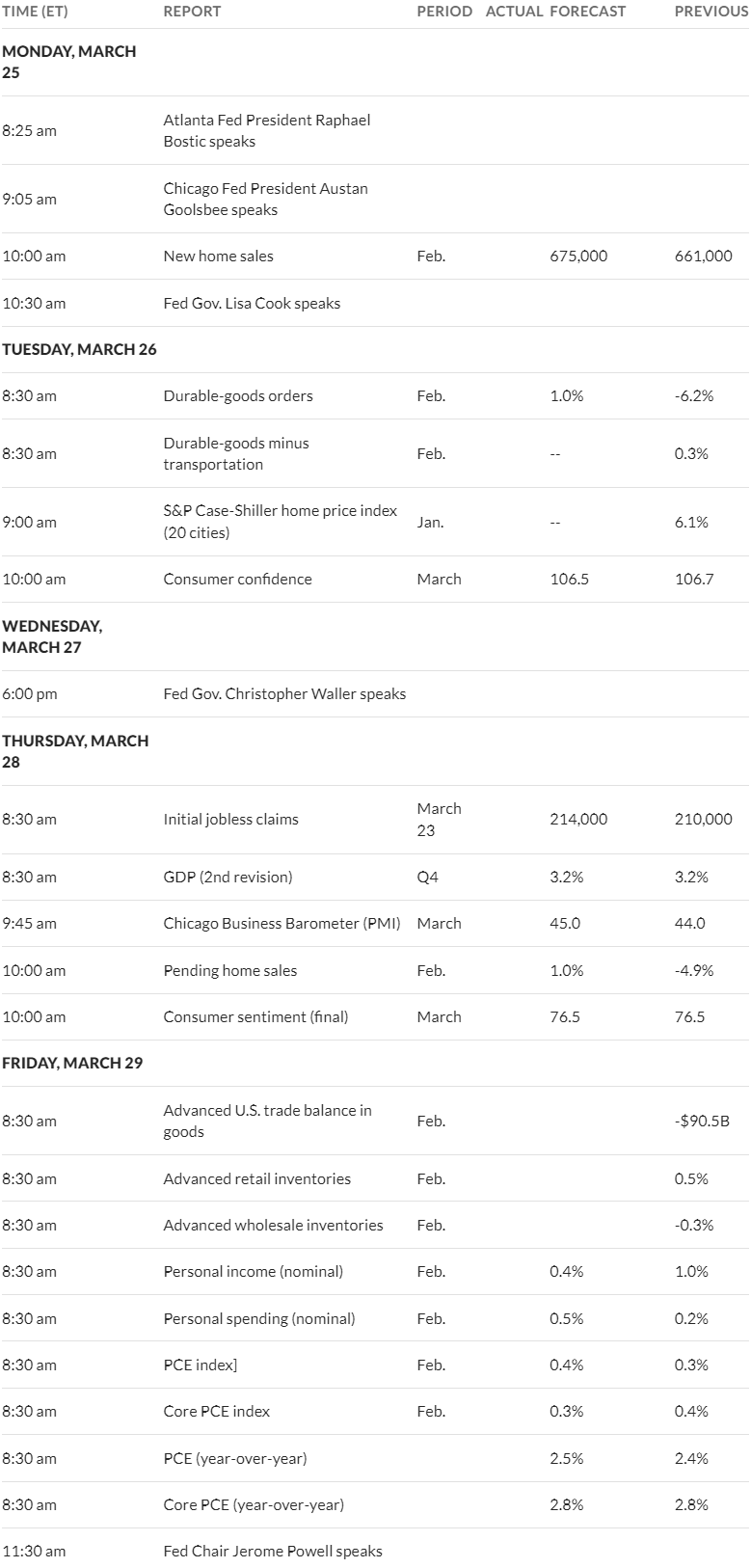

Lately it seems that we are always awaiting ‘news’—in particular inflation news. This week we have the personal consumption expenditures (PCE) data on Friday and just watching interest rates yesterday and this morning it appears that it is highly likely that rates will drift in the 4.15% to 4.30% area. Watching paint dry is kind of boring, but it is always fine with me as long as I am making money–really it is simply what we do.

Today we have durable goods orders being released at 7:30 a.m (central). It is unlikely that anything in this economic release will move markets. At 8 a.m. we have the Case Shiller housing price index–it will show prices continue to rise–no surprise to me. The supposed high mortgage interest rates are more and more being accepted by folks as the new norm–the ‘haves’ don’t worry as many, many are paying cash for new houses–the ‘have nots’ are simply screwed. Yes they may qualify for government backed loans–i.e. FHA, but my experience says that the more houses sold with FHA, VA and other government backed programs that occur the more likely we will see a housing event of some sort when/if a recession comes.

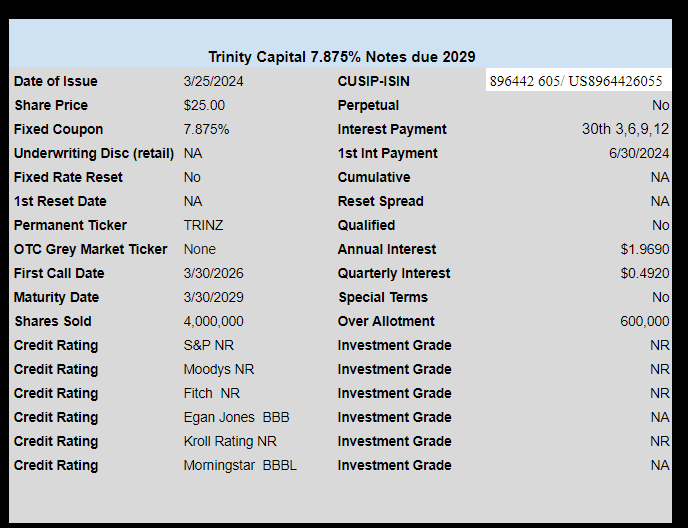

As everyone knows business development company Trinity Capital (TRIN) sold a new baby bond yesterday with a coupon of 7.875%–right in the area of other BDC baby bonds sold recently. The company may use some of the proceeds to redeem some of their 7% baby bond due 2025 (TRINL). I own some of the TRINL issue and thus lost a bit yesterday as the shares moved lower by 22 cents–no big deal. I own TRINL for the 7% coupon and for the stability of the share price being that short maturity issues will trade at $25 plus accrued and this has not changed. If they redeem some of the issue it will be on a pro rata basis that is ok–I can buy more shares if I desire.

Well equity prices are higher this morning–we’ll see if this holds up–no reason to think markets will tumble–all news is good news.

BDC Trinity Capital (TRIN) has priced their new issue of notes due 2029.

The issue prices at 7.875% for 4 million shares plus 600,000 more available for overallotment.

The notes are rated BBB by Egan-Jones and BBBL by Morningstar (not sure how Morningstar rates debt so will have to do some digging).

The company ‘use of proceeds statement is as follows–

The Issuer expects to use the net proceeds from this offering to pay down a portion of its existing indebtedness under the KeyBank Credit Agreement and, depending on the remaining amount of net proceeds after such use, to redeem a portion of its outstanding 2025 Notes.

Well we had a week with some important economic news last week–but Jay Powell and the FOMC news was good news–at least equity markets took it as good news.

The S&P500 moved up on the week by a solid 2.3% from the close the previous Friday. Investors took the news from the FOMC to imply 3 rate cuts yet to come this year—as always we’ll see–no one, including Fed folks, can know what with any certainty what will occur yet this year.

The 10 year treasury closed the week at 4.22% which was down 8 basis points from the Friday before. The yield moved in a 12 basis point range on the week–4.20% to 4.32% which all things considered is a pretty tight range. This week as always there is plenty of economic news, but the biggie for the week will be the personal consumption expenditures (PCE) which will be released on Friday. Also now that the FOMC meeting has been held we will have Fed yakkers during the week so one of them could ‘throw a bomb’ of some sort.

The Federal Reserve balance sheet assets fell by $27 billion–which is a continuation of the $95 billion monthly runoff.

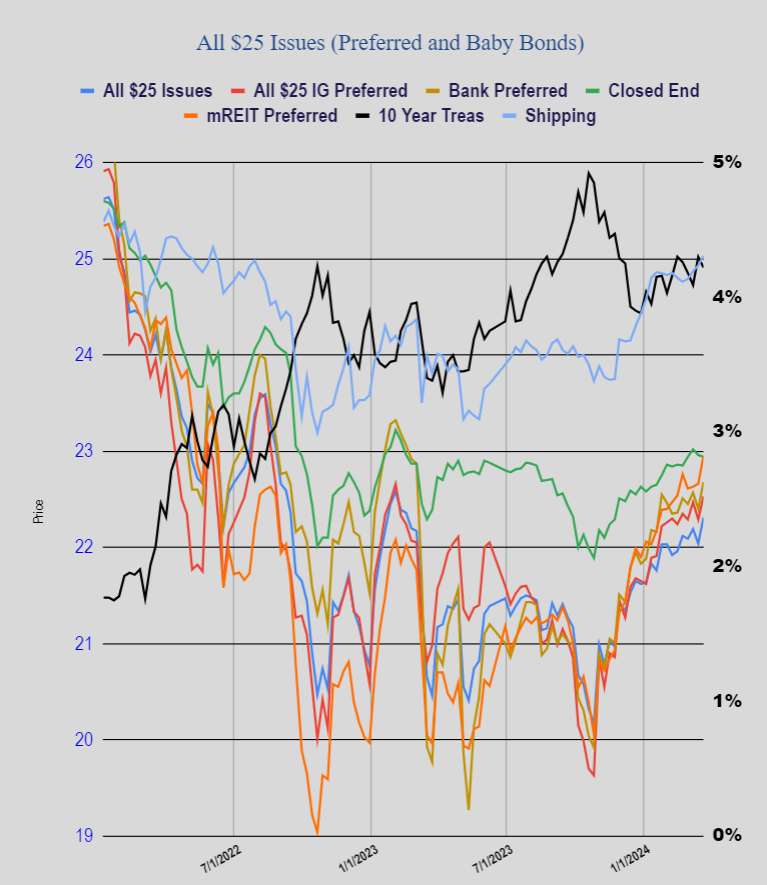

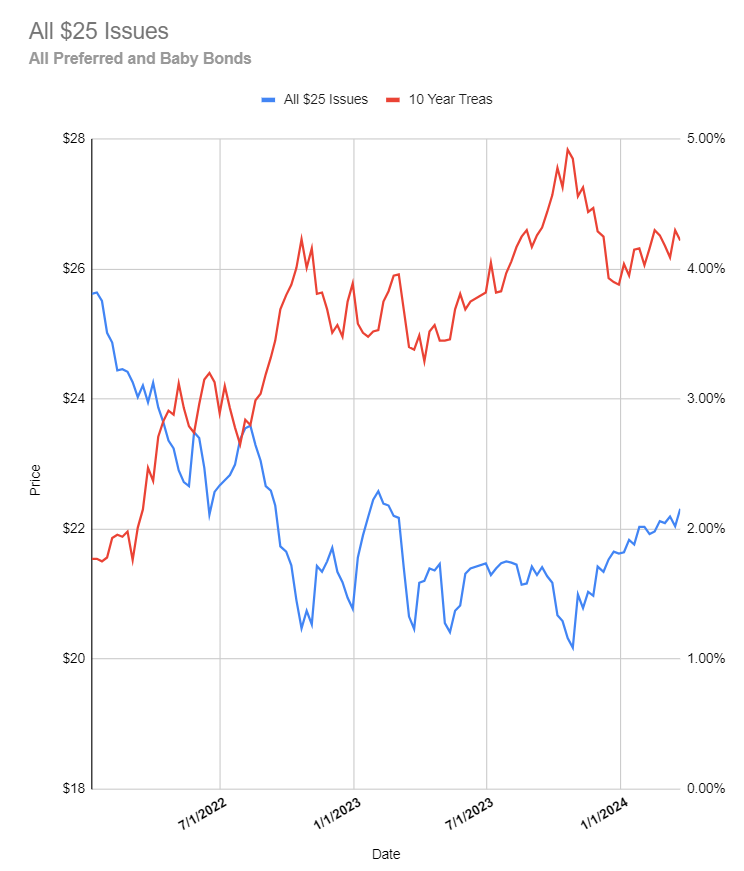

Last week was a surprisingly strong week for $25/share preferred stock and baby bonds. The average share price moved higher by 27 cents–I am fairly certain this gain was affected by the large number of ex-dividends the previous Friday—shares bounced up after being ‘marked down’ the previous Friday. Investment grade issues bounced 26 cents, banks moved up 28 cents, mREITS by 32 cents, shippers were higher by a dime. A very nice week for income investors.

Last week we had 1 new issue price as Brookfield BRP priced a new perpetual subordinated note at 7.25%.

It is tough to get away from CDs at 5.3% or 5.35% for a non callable 3 or 6 month issue. I bought a handful again today.

As I have written about many times in the last few months I want my preferreds and baby bonds to average around 7% yield at my cost and thus far that has been pretty easy to accomplish. Near 6% on the safe issues balanced with around 8% on baby bonds from many of the business development company’s (BDCs)–this gets me my 7%.

Of course, the time will likely come when I have to forgo further purchases of CDs because the yield will slip into the 4.xx% area. As I review my holdings each day I am surprised at the amount of CDs that I have out into 2025 and 2026–noncallable issues around 5.25%–I won’t have to worry about these for a while. Whether I have to worry about less than 5% on CDs this year is anyone’s guess.

For the time being I am targeting around 50/50 split between preferreds and baby bonds and CDs–it could be 60/40 or 40/60 –but in the area of an even split. Obviously when the time comes to move to a heavier weighting of securities it will be difficult to maintain a 7% average, but for now I am not going to lose sleep over it.

I just added to my current position in the Spire 5.9% perpetual preferred (SR-A). I paid $24.75 – not a bargain, but it goes in my ‘sock drawer’ bucket with a current yield just under 6%. The issue becomes optionally redeemable on 8/15/2024.

Well it has been a somewhat decent week–for common stocks and for income issues. Of course we had important economic news with the FOMC meeting and Jay Powell presser which markets decided was somewhat dovish–all news was good news I guess.

Interest rates as represented by the 10 year treasury have fallen a bit through the week—but the reduction was minimal given the rise in the S&P500. The 10 year treasury is at 4.27%–down a measly 3 basis point from last Friday–with the dovish Fed news one could have expected a 10 basis point reduction in yields.

The S&P500 is up almost 2% on the week and equity futures are up a bit this morning. One has to feel like equities are overvalued–but honestly compared to valuations we have seen in the past–huge price/earnings ratios–40, 50 and 60 times this market is just a bit overvalued and those traders who go short the ‘market’ may see bunches of pain ahead. Of course something could ‘break’ at any time, but as always one who invests in preferreds and baby bonds doesn’t want to see a huge equity tumble–it is not helpful to anyone. When one looks at the amount of ‘dry powder’ available that could move into the equity markets I think there is a higher odds of a ‘melt up’ than a ‘melt down’.

I see Brookfield BRP priced a new issue of perpetual subordinated notes last night–7.25%. The pricing term sheet is here. These are investment grade, but being a Canadian company interest payments are subject to 15% withholding in some acccounts.

Also last night JPMorgan put out a redemption notice on a bunch of $1,000/share fixed to floating preferreds–the press release is here.

I am back in the office after 6 days out and will do a little buying today–not sure which issue–we will see–lots of near cash on hand (money market). Accounts continue to hit almost daily new highs as giant sized CD maturities hit–most of which pay interest only at maturity

While we know there will be no Fed Funds rate cut today we don’t know what will happen at the press conference which will happen at 1:30 p.m (central). Are markets ready for some ‘I told you so’ from Powell. At each press conference on previous FOMC days Powell has warned of reigniting inflation so now he can thumb his nose at the so called financial reporters at the press conference. We know that there will be no promises of rate cuts–the only question I have is how much of a hawkish tone he will set. We’ll see-no one knows.

This morning markets are eerily quiet–when the DJIA, S&P500 and NASDAQ all are trading with less than a 1/10% movement you know markets are prepping for big news. I would be shocked if interest rates moved more than a couple basis points lower today–but not surprised if it moved higher. I have no illusions great bargains being created anytime soon in the income issue arena–no visible catalyst.

Lots of cash, in particular in the Fidelity Government Cash Reserves (FDRXX) @ 5.02% today–waiting for a more permanent home. That 5.02% certainly removes the urgency to invest quickly–no all bad taking time to ponder moves.