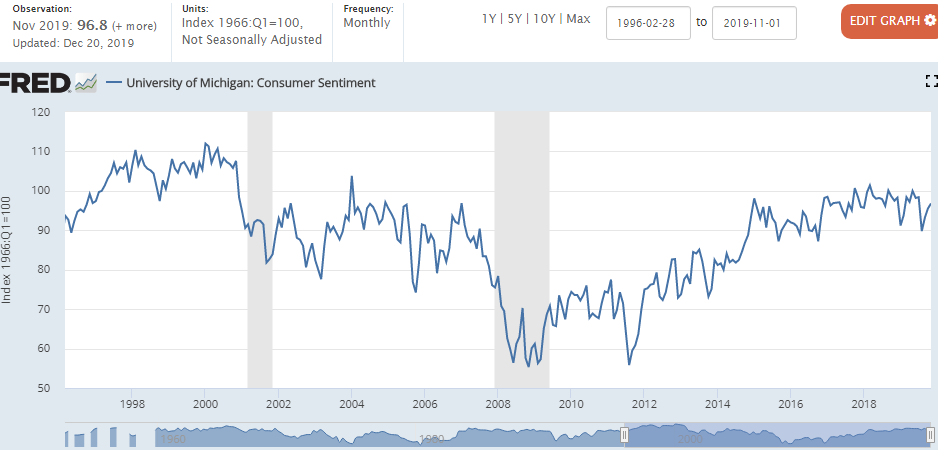

I have always watched the consumer for weakness in the economy–sometimes I simply watch the Univ of Michigan consumer sentiment survey (below)-

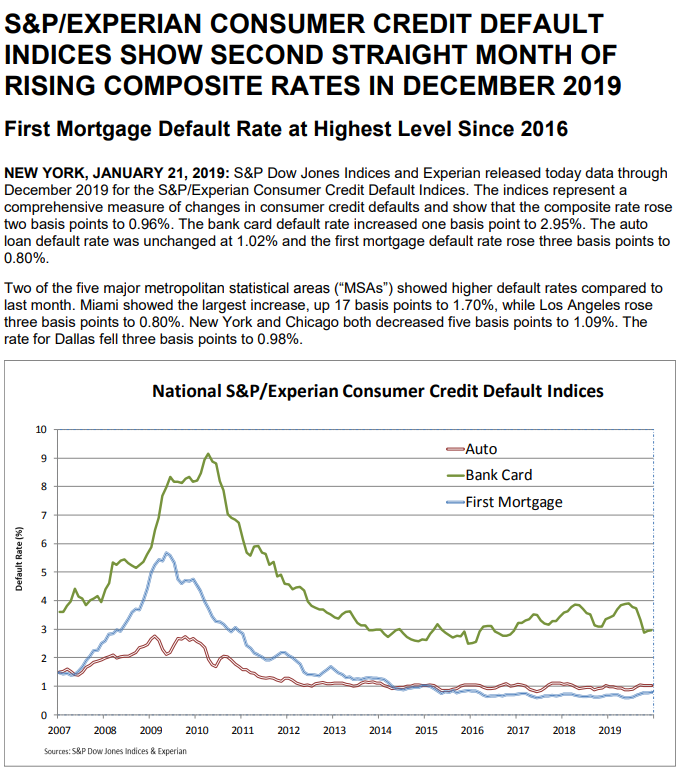

At other times I watch some data which is a little more detailed–plus it comes to me in a RSS feed. Below you can see the consumer credit defaults for auto loans, credit cards and mortgages.

Property of Standard and Poors

While I seldom have worries about my investment grade holdings–the net asset value may moves, but I know the income stream will remain in tact. On the other hand many other holdings that are unrated or just ‘junky’ I worry most about a recession and the consumer being 70% of the economy will likely signal ‘recession ahead”.

It is only common sense that the above data should dovetail nicely with employment–so, of course, we watch those number closely as well.

I know the charts above are a bit hard to read–but I think they show that the consumer is generally healthy–coupled with employment being strong–I think it is safe to say if the status quo remains we are good for the next number of months (short of a black swan).

The S&P500 traded in a range of 3268 to 3330 last week which is where the index closed–up darn near 2%.

The 10 year treasury traded in a range of 1.78% to 1.85% and closed the week at 1.84%–which is exactly where it had closed the previous week.

The FED Balance Sheet rose by $26 billion last week. Recall that the balance sheet fell by $24 billion the week before–I was under no illusion that the FED would reduce overall liquidity for more than a week as equity markets would throw a tantrum.

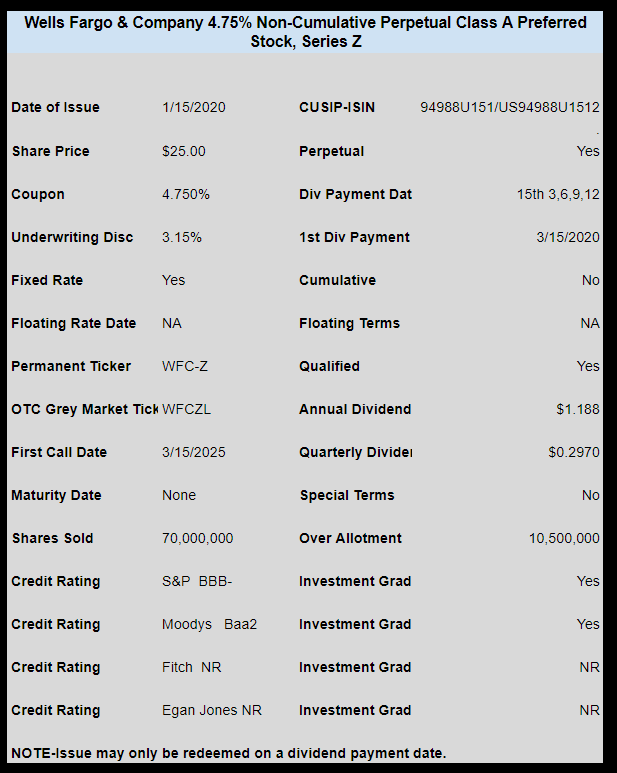

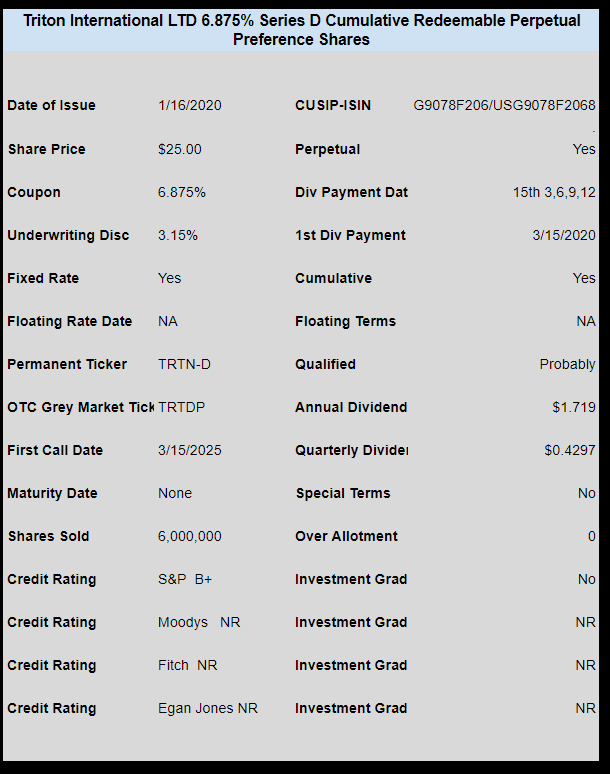

Last week we had a couple of new income issues sold.

Wells Fargo & Company (WFC) sold a new issue of perpetual preferred stock with a 4.75% coupon.

The issue is trading on the OTC Grey Market under temporary ticker WFCZL and last traded at $25.04 last week.

Container leasing company Triton International LTD (TRTN) sold a new issue of perpetual preferred shares which carry a coupon of 6.875%. This issue opened strong at around $25.25 and closed the week at $25.50

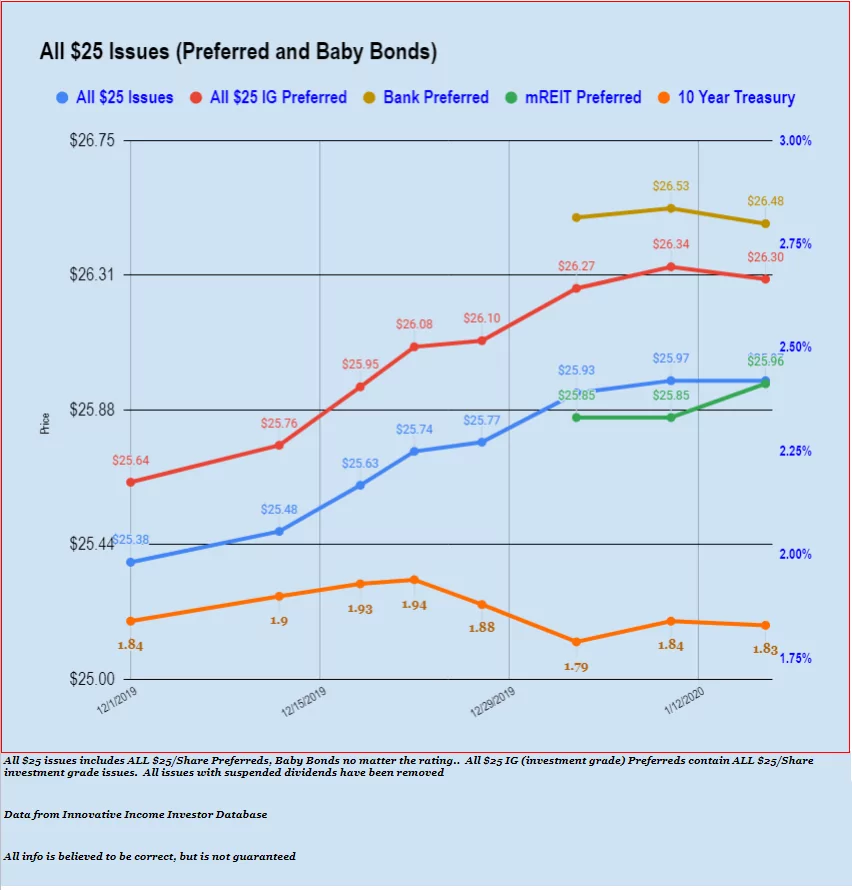

The average $25 preferred and baby bonds closed a bit lower last week–2 cents overall. Banks were the only sector that closed notably lower being down 8 cents. We will have a total of around 17 issues going ex-dividend this week. Next week we will see around 30 issues going ex-dividend.

With today being Martin Luther King day all markets in the U.S. are closed–so I guess we will have to leave the Canadian investors to themselves for today.

We will kick the week off tomorrow with the Tuesday morning kickoff.

The weather is lousy in Minnesota with a big snowstorm and high winds forecast–I hate this weather–guess I need to go to AZ on a permanent basis. Oh well, guess I am stuck here with my wife who isn’t likely to move 1000 miles away from the grandkids. So I will just take a look at markets and see if there is any cheer there.

After the December holidays the new issue market doesn’t seem to be very active–am sure it will change. This week we had the new 4.75% perpetual priced by Wells Fargo (which I bought for hopefully a steak dinner flip–won’t hold too long) and the Triton International 6.875% perpetual, which I had hoped to buy, but decided not to chase it as it opened high and has traded in the 25.28 to 25.50 area.

Some folks on the Reader Initiated Alert page have noted that Seaspan (SSW) is going to delist their 7.25% baby bonds (SSWA) and plans to call them on 10/10/2020. Seaspan is doing some reorganization into a holding company structure. The press release is here.

The Fed has done relatively normal type REPO operations the last couple of days. Yesterday they did $39 billion in an overnight operation as well as a $35 billion term operation (14 day). Today they did a $53 billion 4 day operation (because of Martin Luther King day on Monday). As I noted earlier in the week the REPO plans for the next month were released and beyond a $5 billion reduction in the 14 day operation mid February it looks like liquidity will continue to be required at the levels we have seen in the last month or two.

The FED Balance Sheet data was released today and overall (REPO balances and FED buys/sells) the balance sheet grew by $26 billion in the last week–so ‘party on’ like its 1999. I didn’t think we would see multiple down weeks, because the ‘ball babies’ in stocks would cry.

Of course everybody is aware of the very low coupons we are seeing in the U.S.–but it is nothing compared to the rest of the globe. Giant self-storage company Public Storage (PSA) just sold a 500,000,000 Euro note with maturity in 2032 and a coupon of .875%–YIKES!! We are going to have to rewrite the playbook if this comes to the U.S.

At 1:30 PM CST we have the following pricing in preferreds and baby bonds. You can see that for the 1st time in 6 weeks $25 preferred stocks and baby bonds have tilted lower–not by much, although banking issues are off 5 cents in a week. Much of this downward tilt may be because we saw 72 issues go ex-dividend this week, but on the other hand we had big ex date weeks in December (for instance the end of December we had a week with about 130 issues going ex) that didn’t tilt the average price lower. So does this mean we have seen a peak? Guess we’ll know for sure in a few weeks.

I had hoped to buy some of these shares for a quick ‘flip’, but am not going to pay this price for the shares so I will move on.

Potential buyers of this new issue can consider the 7.375% TRTN-C issue which has a current yield of 7.04%. Note the yield to worst is lower, but with almost 5 years to first call date this is a minor factor.

Folks are saying that Fidelity is charging an extra $50 charge on commissions for Triton being foreign. I know eTrade doesn’t charge this, but some others may.