REIT CorEnergy Infrastructure Trust has suspended the dividend today on the 7.375% perpetual preferred (CORR-A).

The share price has been butchered–from $17.xx down to $8.08

J mentioned this in the Readers Alerts section early today.

5/28/2025

Our site runs on donations to keep it running for free. Please consider donating if you enjoy your experience here!

REIT CorEnergy Infrastructure Trust has suspended the dividend today on the 7.375% perpetual preferred (CORR-A).

The share price has been butchered–from $17.xx down to $8.08

J mentioned this in the Readers Alerts section early today.

I normally have smaller capital gains and smaller capital losses than maybe the typical perpetual preferred investor–and I give up some higher potential coupons in doing so.

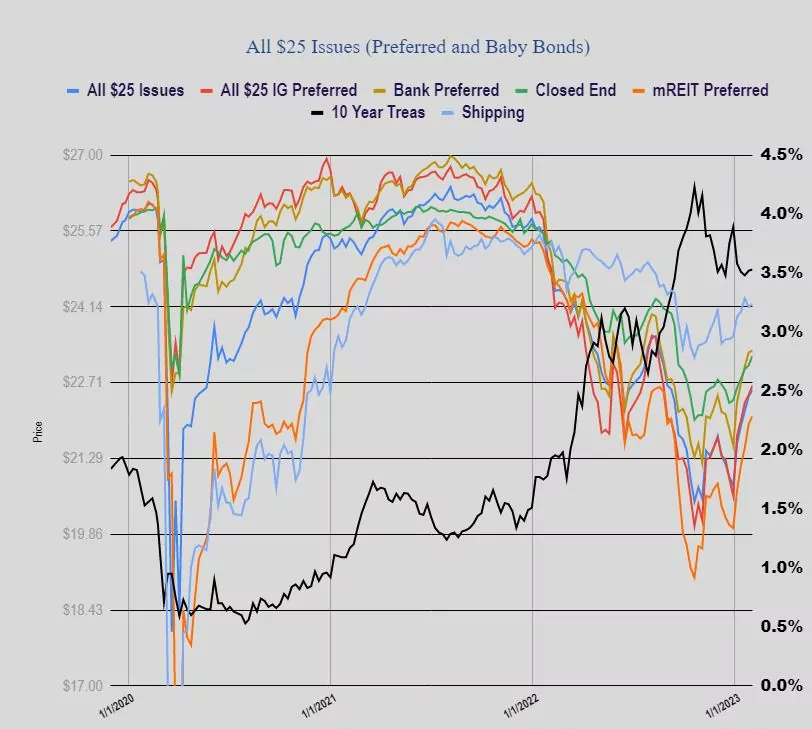

Closed end funds (CEF’s) can typically sell lower coupon preferreds because some of them sell ‘term preferred’ issues. A term preferred has a stated mandatory redemption date–not unlike most bonds–versus a perpetual preferred which has no mandatory redemption date whatsoever and may be outstanding for 100 years (of course no one knows for sure). This typically means that the ‘term preferred’ is less volatile than a perpetual preferred and the losses and gains that occur over the course of a year or 2 are minimized–all due to the ‘date certain’ redemption date which is typically 5-6 years or less.

Additionally CEF’s have to maintain a 200% asset coverage ratio on their ‘senior securities’ (debt and preferred shares). This is an added level of safety.

My 2 largest holdings–by far are the RiverNorth Capital and Income Fund 5.875% term preferred (RMPLP or RMPL- or RMPL-P or others as all brokers have a different ticker for this one) and the 6.50% XAI Octagon Floating Rate and Alternative Income Term Trust term preferred (XFLT-A).

Note that the mandatory redemption on the RiverNorth issue is 10/2024 and the XAI issue is 3/2026.

The reason I hold these–and have for years–is because it is a reasonable coupon, they have to maintain a 200% asset coverage and the movement of the share price is relatively minimal (compared to a perpetual).

Do I like the closed end funds–not really–to me they are dogs and in the case of the RiverNorth issue is not well managed. This means I keep an eye on the funds even though I don’t hold the common shares–this is not a ‘set it and forget it’ investment (to me there are no such things).

Here is the RiverNorth issue for the last 4 years. Compared to a perpetual it has had a tight range.

At this point in time these 2 issues should only be bought around $25–and both have been trading near there for the last month.

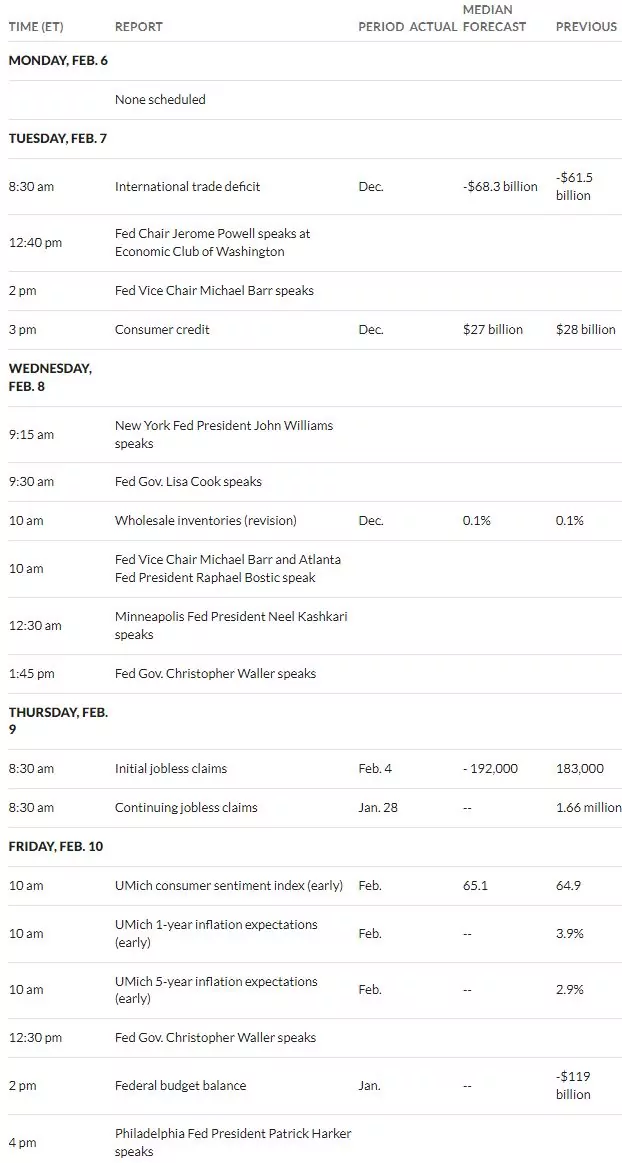

All in all a decent week for the Standard and Poor’s 500 with a gain of 1.6% over the previous Friday close. The range for the weeks was over 4% as we had a couple high importance economic news items – the FOMC rate hike decision and the release of a very strong employment report on Friday. This morning we have the S&P500 futures off about 1%–for what that is worth.

The 10 year treasury yield closed almost where it had closed the previous Friday at 3.53% (versus 3.51% the previous Friday). The strong employment report on Friday kicked yields up by 13 basis points we gave us a rare loss in income issues on Friday. We are starting off the new week with higher rates as the 10 year treasury is up 7 basis points this morning to 3.60%

For the coming week we have few economic reports coming out–one can never tell what will move markets though. Of course we have Fed yakkers–and any one of them can move markets.

The Federal Reserves balance sheet fell by 37 billion from the previous week–now at $8.433 trillion. So since April when the balance sheet peaked out at $8.965 trillion we are down about 1/2 trillion–another 10-15 years we will have a zero balance sheet–ain’t going to ever, ever, ever happen, but if we can get down a trillion or 2 we might have a shot of re-inflating the economy out of the next deep recession.

Last week was a decent week for income issues with the average issue up 13 cents. On Friday we saw a drop of maybe 1% though on the employment report and subsequent levitating of interest rates. Investment grade issues rose 18 cents, banking issues rose 4 cents and mREIT issues were up 14 cents on the week.

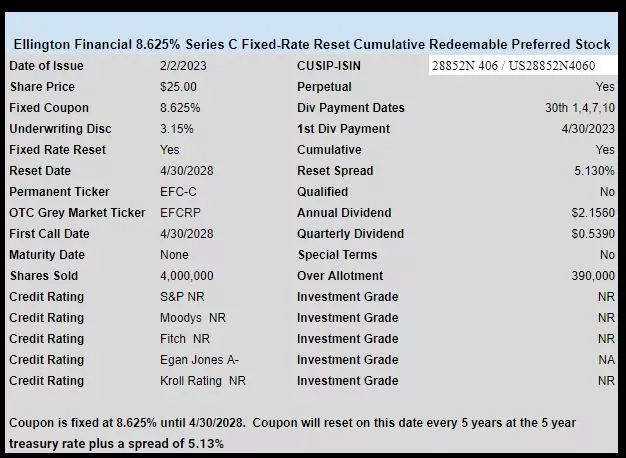

Last week we had one new income issue priced–a fixed-rate reset issue from mREIT Ellington Financial (EFC). The issue is trading on the OTC right now and last priced at $24.58.

As might be expected when you have a ‘blow-out’ new jobs number (over 500,000 new jobs) interest rates have taken a pretty big jump higher–up 12 basis points on the 10 year treasury yield to 3.52%. While in years past a 12 basis point move higher would likely send prices of income issues tumbling hard–that is not the case now.

Overall prices are generally red, but maybe only by 15 cents or so – on average. My accounts are negative, but only by maybe 1/5%. There are still buyers out there stepping in to make buys–keeping losses pretty minimal. I do note that the investment grade AIG-A 5.875% perpetual preferred is off $1.50/share in the last 2 days and now yielding 6.10%–I assume it is off based on the sacking of the CFO a couple days ago. This is a decent issue if one can get it here at $23.98 or so.

The employment number sets Jay Powell and the FOMC committee for another rate hike on March 22nd (the end of the next meeting). We will have substantially more data , including more employment numbers, by the time the next meeting rolls around but I think it is highly unlikely that the FOMC will be deterred from further hikes.

So on to the weekend–I am looking forward to it – mostly because the temperature will rise here in Minnesota to the 30’s–right now it is almost 1 p.m. and it is still -4 degrees – too cold for old people like me.

Below is the pricing information on the new Ellington Financial (EFC) fixed-rate reset perpetual preferred.

The issue should be trading on the OTC market today under ticker EFCRP.