After Monday of this week the investment gains have been pretty stellar for everyone–whether you were in preferred stocks, bonds or obviously common stocks. Seems common shares should be peaking out (or not moving higher) all things considered, but there remains massive amount of money available to ‘buy the dip’.

The 10 year treasury is trading at 2.148% right at this moment which is down about 10 basis points from the high of the week. This rate has numerous Fed rate hikes built into it already so I am not looking for much higher rates for now–maybe later. Also if the Fed were to start quantitative tightening by selling securities to reduce the size of the balance sheet we could see somewhat higher rates.

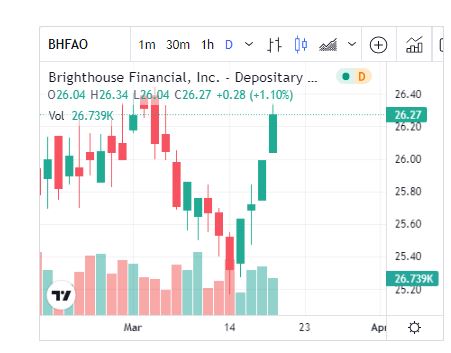

My accounts were up maybe 3/4% this week as we got some bounce back in oversold issues. I added 3 investment grade issues–2 new and an addition to my Brighthouse Financial 6.75% perpetual preferred (BHFAO)–the move in this issue was typical of what we saw in many issues this week. Didn’t sell even 1 share.

The other issues I bought were American International Group 5.85% (AIG-A) perpetual and Assurant 5.25% notes (AIZN). Actually would have bought a little more but I have been hammered at my ‘real job’ so just couldn’t get around to finalizing more buys. Oh well there will be plenty of time to find decent buys in the weeks and months ahead—besides it is always my plan to ‘leg in’ to positions.

Grid,

When you say 10.5%, are you talking about iBonds? Last I checked they were at 7.1%.

Akj, Camroc owns the oldies with the 3% fixed add on adjustment.

https://schrts.co/RCuuutRf

Now that the fed has got inflation religion. I expect the 2/10 will invert some time this year and now my focus is on the 3m/10y curve. How they sell off their balance sheet will effect how quickly this inverts. The bond market sees the fed funds rate near 2% later this year. If the 10y doesn’t rise much from here we will see this invert some time next year. Months after this inverts we will enter a bear market worse than what we are experiencing now. Until then I think we get a blow off top in SPX 5000+. Time to prepare. ATB

Tim..I love your site..I assume the only way to get involved with your data and insights is to “reply”? There is no description whatsoever in all your toggles how your service or site works from what I can gather? Is the only way to communicate is to simply “reply”?? thanks

For the week, the low coupon, high quality preferreds (Canaries) were up +0.35% but are still down -15.6% YTD. All preferreds were up +.90% but are down -4.3% YTD. Babys/terms +.43%/-2.9%.

Tex,

SPPREF down ~9.4% YTD. Is the -4.3% an unweighted average?

TIA

NH, the -4.3% YTD is an unweighted aka equal weight of 624 preferreds that I track, of all par values and including convertibles. It does not include babys/terms. The 624 had to trade on both 12/31/21 and 3/18/22 to be included. The largest preferred ETF, PFF, is down -8.27% YTD, so the unweighted is more optimistic. Possibly because when you cap weight issues, the banks take a larger allocation. And banks broadly speaking are higher quality, lower coupon issues which have taken a bigger hit this year. Bottom line to me is that the difference is not surprising.

Tex,

That’s pretty much what I had figured.

My experience with preferreds does not go back as far as many here. But a few months ago I had expected that when the rise in interest rates came, all issues would generally be affected the same – that is, the credit spreads would be pretty much maintained. (If anything, I believe that, in the past, credit spreads generally widened when there were sharp spikes in interest rates). However, based on what you say, and my own observations as well, that seems not to be what has happened so far this year. The high quality, low coupon issues have been torched, while the carnage in the higher coupon issues has in general been relatively less, which would imply that there has been something of a reduction in credit spreads.

I read Innovative Income almost everyday and I see your comments prominently displayed with good insights in addition to Tim and others. As an active term preferred and baby buyer, I have no clue how to sign up or get involved other than replying to comments. For example, I know you keep an active database of the 900 plus preferred offerings. Can I buy that, subscribe, access? Thanks

Hi Chip, I feel an obligation like several others to contribute to III whenever it might add something useful. Preferreds/terms/babys while interesting are not our primary focus. We allocate a lot more time and $’s to some other asset classes. We publish a few snippets of our data here but it is generally for our own use and is not available for anyone else to access.

As Tim knows all too well, it takes a LOT of time attempting to keep the data up to date. The closer you want to get to 100% accurate, the more time it takes. Automation helps some but is not complete. For example, I published a list last year showing issues I thought had suspended payouts. It took something like 10+ replies to correct the list. Justin knew that an issue had been paying out in stock, not cash, which did not show up in my database.

There were 173 p/t/b’s that did not trade Friday (3/18). Was there a ticker change, a call, buyout, went “dark” or is everything still good? To approach 100% accuracy, you have to track down each of these “no trades” very regularly, say each week. I did that last week and send Quantumonline, three updates to their database. Last year I sent ~ 18 updates to them listing ~ 30 changes. “It takes a village!”

thanks Tex for the reply. When you say ‘we” are you with a brokerage/investment firm? My broker does not have an orientation towards fixed income like me. I like preferreds,baby’s in particular but play golf everyday in retirement. I’m looking for brokerage firm that has a focus on fixed income in that I dont buy stocks. Thanks again for reply and I really pay attention to your replies on Tim’s site

It only takes some dip buying to trigger a more massive amount of short covering, which makes snap back rally days even more extreme than the larger down days, as the short covering feeds on itself. It was not a very productive week for those looking for better prices than we already had, but the feel good factor was certainly there. That contradiction is always present, obviously

no buys or sells on the week did satisfy my remaining “RMD” with an in kind dist. @25.14 ex div. today of GDV-H , hoping it will survive a long time past call, in my sock drawer?

What do you mean by saying you have taken an “in kind” distribution for your remaining RMD?

sorry assumed everyone was aware https://www.irahelp.com/slottreport

Thanks, mike – yes it is pretty straight forward actually… I’ve just never thought much about doing an in kind RMD distribution because I always have too much cash hanging around anyway… But it is something worth considering and also strategizing about – whether to take out appreciated securities or those that you think might be temporarily crushed…. For those like myself who have never given them much thought, here’s TD Ameritrade’s explanation on “in kind” RMD distributions:

“How to Take In-Kind Distributions from Your Traditional IRA

January 1, 2020

….

“You can do in-kind distributions from your IRA if you want to,” said Dara Luber, senior manager of retirement product at TD Ameritrade. “For some retirees, this can be a way to pursue their goals without selling investments they’d rather keep.”

An in-kind IRA distribution means moving stock from your tax-advantaged retirement account into a taxable investment account—such as a brokerage account—without liquidating the shares first.

Here’s what you need to know before you decide to take an in-kind distribution from your IRA.

Reasons Retirees Take In-Kind IRA Distributions

Deciding to take an in-kind IRA distribution is about your personal preferences and goals. A retirement specialist or tax advisor can help you evaluate your situation to help decide if it’s the right move for you. According to Luber, retirees might choose in-kind IRA distributions for several reasons:

The market is down. Some retirees don’t like the idea of selling their investments when the market is low. An in-kind IRA distribution lets you keep your assets intact.

Fondness for a stock. If you like a stock and think it might do even better in the future, you may not want to sell it just yet. An in-kind IRA distribution allows you to keep the stock.

Don’t need the cash. Maybe you just don’t need the liquid money right now. Taking an in-kind distribution allows you to move assets to a taxable investment account and even potentially get favorable long-term capital gains treatment down the road.

No matter what the reason, it’s important to evaluate your unique situation and figure out if an in-kind IRA distribution can help you pursue your retirement goals.

Tax Treatment of In-Kind IRA Distributions

“You still have to pay taxes when you use an in-kind IRA distribution,” said Luber. “The IRS wants the money. That’s the point of RMDs in the first place.”

Here are some of the tax considerations involved with in-kind IRA distributions.

You pay taxes on the value of the assets you transfer. Some retirees prefer to use in-kind transfers during a stock market downturn because you’re taxed on the value of the assets you transfer, Luber explained. If you paid $20,000 for a stock a few years ago, but now the value of those shares is $15,000, you’ll pay taxes on the current, lower value of the distribution. But it’s important to pay attention to your total RMD amount. Although a lower value can mean lower taxes, it’s also possible that the value of your in-kind distribution may not meet the minimum. You might need to move additional assets, or even withdraw some of your RMD in cash, in order to make up the difference.

An in-kind IRA distribution resets the basis. “When you use an in-kind RMD, your basis resets,” said Luber. “The IRS sees the value at transfer as your new basis.” Suppose you originally bought shares of a stock for $12,000. Now those shares are worth $17,000. With the in-kind RMD, you’ll pay taxes on the higher amount, but it also becomes your new basis. If you sell the shares for $20,000 later on, you’ll only pay taxes on the $3,000 gained since your new basis. But keep in mind that the new basis also resets the time frame. The date of your transfer is considered the starting point for capital gains, so if you want the favorable long-term rate, you’ll need to keep the assets in your taxable account for more than a year before you liquidate them.

How to Complete an In-Kind IRA Distribution

“Taking an in-kind distribution from your IRA is fairly straightforward,” said Luber. “Figure out how much you’re supposed to withdraw and then let your IRA custodian know you want to transfer the shares into your taxable account.”

Look in IRS Publication 590-B to find the factor for your age. Then divide your account balance (as it stood on December 31) by that factor. That’s the value of your in-kind IRA distribution. Your IRA custodian should be able to help you with the transfer. With TD Ameritrade, for example, it’s possible to go into your IRA online and move the shares into your TD Ameritrade brokerage account.

As you go through the steps, though, it’s important to take market fluctuations into account. It takes time to move assets, so if share prices drop during the transfer, you may not meet your RMD. Verify that the final value of the shares you transfer meets your RMD—and take steps to solve the problem if you fall short.

In the end, only you can decide whether it makes sense to take your RMD as an in-kind distribution. Carefully consider the implications and speak with a professional to help run the scenarios and figure out if it’s the right move for you.”

We manage an IRA account that is constrained to only hold FDIC insured CD’s and/or US Treasury paper. We try to keep it fully invested at all times, so there is insufficient cash to take out the RMD each year. We do a like kind CD position transfer to a taxable account to make the RMD. We do this several months in advance so that the brokerage shows the like kind amount counting against the RMD. If there was some kind of problem with the amount, you sure do NOT want to get into the situation where the brokerage/IRS claims you did NOT take out the RMD with the attendant penalty. Better to make sure it is all clear well in advance.

Mike.. I have been taking “in kind” RMDs right along. My strategy has been to find high yielding common stocks or reits with the highest percentage of capital appreciation in my IRA. Now I get to enjoy continually receiving that high yield on my original basis, while at the same time have my RMD actually cost me around half its value at the time of transfer. In addition if it messes up in the future and I sell it, I get a little “rebate” on my taxes due to the increase in basis realized upon transfer. An IRA and taxable account with the same broker makes it real easy.

“lucky and others” one step ” further” since 2010 prior to my Rmd time and passed 59 1/2 i was able to do, backdoor roth conversions now exceeding $200m but those days are now gone. Some thing for the younger guys to think about.

Yes, Tim, its been a great week. I feel so much smarter when my issues go up in price, ha. Some have been jumpy up and down, and I have sold, and bought the same issues a couple of times each day.

My wife states that I not only look smarter this week. I smell better. Interesting article for those who invest in oil service stocks. Interesting article on FT.Com entitled Western Oilfield services companies stay the course in Russia -Schlumberger, Haliburton and Baker Hughes are partners in state backed Rosneft and Gazprom Russian oil companies. The three major oilfield service companies do the frontline work in Russia doing the drilling of wells and producing oil and gas. The US companies conduct billions of dollars of business in Russia. The sanctions of the US only ban new investments in the Russian energy sector. Even though sanctions were put in place in 2014 after the invasion into Crimea, the oilfield companies have worked around the sanctions. Vanguard 500 index fund and Capital Group are major holders of the above stocks. Thus, Americans are funding the companies who are keeping the tap running for Putin. Very interesting times for investors in these companies once this story makes headlines

I have a contrary approach. Following the bottom line is not a good measure of wheteher you had a good week. Prices go up, prices go down. You can lose money making good trades in a down week, and you can make money with bad trades in a good week. It’s all about making good trades in any kind of market and the ups and downs take care of themselves.

Don’t call me Pendy, but I no longer track gains, just income. I stopped a couple of years ago, about 25 into my retirement. My goal is to receive irrationally high but sustainable (mostly tax deferred) income. I don’t concern myself with market price so long as the company is strong and the dividend ( or distribution in the case of an MLP) is sustainable.

I don’t like to trade stocks, though I occasionally catch Gridbird fever when I see something especially volatile. Recently that was KNTK, which bounced up and down from high 50s to high 70s for several weeks before its acquisition and rebirth. But mostly I invest for income, as described.

Back when I was in my early 40s and living the good life working in Europe, I was driving my new beemer to a delightful weekend at an posh inn in the Alsace and some Michelin 3-star dining. Somewhere on the road that night it suddenly occurred to me that I would never be able to retire on a pension that was only 55% of my salary, however good it was. Well, duh. So…. After my eureka moment, I finally began to save and invest in earnest, because I, ever the hedonist, was very late to the game and really behind the curve.

Fast forward to 2022. My other income is now triple my current pension, which has been somewhat inflation-protected all these years and is now triple what it was in my first year of retirement (1995).

So today I have the luxury of not churning my portfolio for capital gains. Just give me the safe and steady or rising income.

Have I made misjudgements along the way? Oh, yes, but nothing that put me in the ditch before I could correct. And I have rejiggered a bunch of my holdings this tumultuous year. Almost all my sock drawer illiquid utes are sadly gone. It’s now all about inflation protection. We’ll see what other surprises these interesting times will surely bring us.

“It just goes to show ya! It’s always something!” –Roseanne Roseannadanna

GLTA

Camroc, well I hate to tell you this but you are already disqualified from being a PennilessY wanna be. Mostly because you buy income issues that well, actually pay out income instead of it getting cut or suspended. Plus you dont have the appearance to want to obfuscate any, ha.

Besides who are you kidding. Forget all your investments, you could live a good life on your SS, pension, and present IBond income alone! 10.5% guaranteed puts a lot of beans on the dinner table, doesnt it. 👍Oh, and its looking more and more like you will be able to say its 11.5% guaranteed in another month…..