Just a few severe discrepancies in pricing I noted this weekend. I know that some folks have discussed these issues before–but the pricing variances are so wide I thought I would highlight them.

The 3 company’s with wide variations in very similar baby bonds and/or preferred stocks are B Riley (RILY), Sachem Capital (SACH) and Priority Income Fund (not listed). This is not a recommendation for any particular security, but I personally own some of the Priority Income Fund term preferreds.

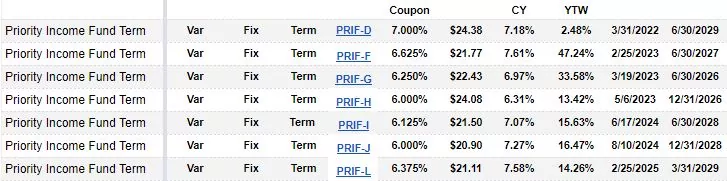

NOTE that the yield to worst on these charts are based on 1st possible redemption date–these charts were put together when those dates were meaningful (i.e. many issues were being called on the first possible redemption date).

Take note of the wide spread in current yields as well as the yield to worst (based on 1st call date). Investors may want to make changes in the issues owned–there are opportunities.

B Riley issues have a few differences–primarily that some pay a ‘bonus’ payment if called prior to maturity. 1 issue has the ability to call prior to the 1st call date as well with payment of a make whole payment (current value of future interest payments).

Priority Income Fund issues are all essentially the same with the exception of coupons, 1st call dates and mandatory redemption dates. You can see that the PRIF-F 6.625% issue is substantially under priced at this time.

Sachem Capital issues are all relatively the same issue with different coupons and dates.

MBINM vs MBINO could be another price mismatch. M priced over $4 higher because of the higher divvy now. But unlikely to pay much more than $2 or $2.50 extra before they both float in 2027. Though harder to evaluate that far out and because we’re comparing Tresaury float to Libor float.

I switched RILY-M for N back during the lockdown due to a major price discrepancy. So I own N and L currently. I don’t see much advantage in me switching out my current holdings w/recent price action. Hopefully, they can pull some more magic out of their hat as they’ve done in the past cause they are taking hits from CORZ, FAZE, and BW to name 3.

Don’t forget EOSE…I put that in my ultra high risk, throwaway money bucket. Boy I sure named that bucket right… At least I didn’t put $100 mil into it like one of the Koch brothers did.. Probably not a scale tipping sized investment for RILY (or Koch) but percentage down is huge and I don’t think they’ve sold their shares…. Is anyone else reminded of Michael Milken when thinking about B. Riley?

Tim-

I’m pretty sure that RILY – G, K, & Z have make whole provisions.

Thanks Gary—I didin’t re-read the prospectus but will do so and update the security page.

TIM-

Also, SCCD dates are : 12/20/23 & 12/30/26

Great tables / info. — thanks

Great info. I traded my PRIF-J to PRIF-F. Would love if they called the latter in January

Wash sale. In a taxable Etrade account I’m thinking of selling PRIF-L and buying PRIF-F and thereby harvest a tax loss while making the switch to something slightly better. But I wonder if Etrade will flag it as a wash sale. What if I buy PRIF-F first, then a day later sell PRIF-L at a loss. Does that help any? Thanks.

Trading between similar issues has not been considered a Wash Sale. They are not exactly the same. Might not be consistent with the loose definition of wash sale but that’s how taxes have been treating it.

In the gray area but probably yes.

“They are not exactly the same. Might not be consistent with the loose definition of wash sale”

The legal standard for a wash sale is “substantially identical”. Its a very high standard, which basically refers to the same security, or perhaps a convertible one where the conversion is nearly guaranteed in an upcoming merger or something. Different preferred stocks with different coupons and different maturity dates are nowhere close to this standard.

S&P 500 etfs run by different companies still have different voting rights, securities lending procedures, index tracking strategies, etc. Those might get ruled to be substantially identical one day, but that IRS hasn’t done that yet so anything more different is totally in the clear with regard to current guidance.

Do what you want, but I follow the guidance of justice Learned Hand

“Any one may so arrange his affairs that his taxes shall be as low as possible; he is not bound to choose that pattern which will best pay the Treasury; there is not even a patriotic duty to increase one’s taxes. “

Nice quote and the Helvering v. Gregory, 69 F.2d 809 (2d Cir. 1934) is interesting to read.

Etrade (don’t know about other brokerages) automatically assigns a “W” if it deems a trade a wash sale, so there is no opportunity to arrange things to my advantage, but I could sell in the Etrade account and then buy in another brokerage account the identical security, and nobody (IRS) would be the wiser (at least not yet).

A broker will never flag a wash sale unless it’s exactly the same CUSIP and the same account. The IRS rules are more stringent and apply across accounts (and even to your spouse’s accounts).

However, as already mentioned, PRIF-L and PRIF-F are not substantially identical.

Also, you should report the correct wash sale status on your tax return even if the broker made an error.

For those interested, The Heisenberg has posted his first article on SA in about 2yrs.

I find him insightful, and I am not the only person judging by comments who finds him a difficult read with the level of comprehension needed for the words he uses.

But It does make me think. He voiced exactly what I have thought this past two years that inflation Is a result of supply side issues and not the result of demand. Although that has some effect.

His point that he repeated several times is that increasing interest rates is not going to solve the problem. Could break the system, and rates will not stay high long term..

He also mentioned Vincent Cigneralla”s article on Bloomberg there is a chance the treasury bond market could freeze up and take the stock market and economy with it. Basically even with higher rates the bonds are not attracting interest. Finally he said the same thing I have been thinking, look overseas for something to happen first.

So I might be whistling past the graveyard this Halloween. Still be buying, but good quality and IG with low ball bids out there. The higher risk keep on a 2 to 5yr short leash. No interest in RILY bonds at this time

yes Joseph Stiglitz the Nobel economist echoed same on inflation a few mos ago, raising int rates destroys tepid demand but does not bring more supply. Heisy comes and goes, he had another article recently. Must be looking for subscribers- or SA enticed him back they need help! lol.

I dont think they know from day to day anymore what they are doing tbh. My avg yield on pfd/bb’s on cost is around 8.5%+ now (buoyed by a slug of NSS) and even if infl settles at 3-4%, it meets my required yield to hold them. If JP/CN use their Treasuries sold to buoy the yen/yuan vs US$, coupled w FED QT, Treasuries could blow out further and hit what I hold more but I am ok as long as I feel underlying pump out the income to reinvest. This kind of income is nothing to sneeze at when you are receiving it and scanning hot/watch lists for the money. Still lucky I don’t need the income yet to live on and can keep investing it. Oh well, volatility continues. Bea

Bea right there with you. But not sure where my average return is at currently. Been shooting for a 7% return, but even in this up market there are areas that are down and the babies getting thrown out with the bathwater. I been looking at REIT preferred and some good ones have been in a 6 month down trend. I put in some bids to collect a 7% return if they hit. Kinda like the spider sitting in it’s web

Charles – after reading your “non-interest” in RILY issues I reviewed their financials and promptly sold my holdings. The balance sheet equity is rapidly eroding and could be a deficit in the next year thus putting all RILY etd’s at risk.

I lost interest in them long ago. They are aggressive investors. And in this economy and interest rates it makes me nervous. Im not smart enough to analyze all that is under their hood. They about blew themselves up about 8 years ago, when the common stock dropped to under .25 cents a share.

Heisenberg is exactly correct. Either the FED is as dumb as all hell or they have some vested interest in a recession. Remember, Powell was a Trump appointee.

Tim – your spreadsheet shows a maturity date for RILYO of 5/31/25. I think this is incorrect as Quantum and FIDO show a 5/31/24 maturity date. I have a large position in this mainly due to the fact that of all the RILY issues it is the first in line to be redeemed. I added to it on Friday’s dump. Thanks for the heads-up on PRIF-F. I just bought PRIF-D at it’s 52 week low of $22.16, but PRIF-F is still superior as it matures 2 years earlier than the D – will try to swap this week. While some may opt for the highest YTM amongst these issues, I have my “default fear cap” on and have focused on the shortest matuities in the “Term” arena -SCCB, OXLCM, RILYO, OXSQL, PFXNL, RMPLR.

I have a similar take on these — the RILYO and RILYM appear to have a much lower default risk given that they are both paid earlier and are smaller issues than the later RILYT and RILYZ tickers.

Tim, you list RILYH and I show that it was called in full for 9/4/21. Also, many of the RILY* issues had premiums above $25.00 depending on when they were called. For example if RILYZ is called on its first date of 8/31/23, the principal amount would be $25.75. RILYK has a make whole provision. I don’t know if you incorporated these into your YTW calculations or not, but I am showing different YTW’s. These changes might account for some of the differences you see between the different RILY* issues.

Another severe pricing discrepancy. NLY-F 24.04 vs NLY-I 20.33. They float at the same rate beginning July 2024. Until then F will pay about a dollar more in dividends. So it should be priced about a dollar higher.

I calculated the Yield to Maturity values for the PRIF issues using Excel.

PRIF-D 7.81%

PRIF-F 10.70%

PRIF-G 10.15%

PRIF-H 7.36%

PRIF-I 9.80%

PRIF-J 10.02%

PRIF-L 10.14%

If anyone gets different (or indeed, the same) values using a program that calculates these, please post them.

I use this Yield calculator : https://quantwolf.com/calculators/bondyieldcalc.html

Yields calculated by RS are close to true, accuracy depends on the settlement after purchase date . All things equal i would buy now the longest maturities in each Baby Bond for the cash flow income . PRIF-L -9.65 yield to Maturity through 03/2029 RILYZ – 13.08 yield to Maturity though 08/31/28 SCCG -13.68 Yield to Maturity through 09/30/2027

Nikolas – I only checked one of your three examples, PRIF-L and found that your https://quantwolf.com/calculators/bondyieldcalc.html comes up with exactly the same YTMs, both “clean” and “dirty,” as Fidelity’s https://digital.fidelity.com/prgw/digital/priceyieldcalc/. Good to know a convenient alternative calculator that may be a little bit easier to use. I do have one question, though: In your calculator, is there any explanation anywhere as to what “Annual Equivalent Rate” is supposed to mean? I don’t understand what that is implying. Thnx

Trying to answer my own question, is this a good explanation of “Annual Equivalent Rate?” https://www.investopedia.com/terms/a/aer.asp

“The AER is the actual interest rate that an investor will earn for an investment, a loan, or another product, based on compounding. The AER reveals to investors what they can expect to return from an investment (the ROI)—the actual return of the investment based on compounding, which is more than the stated, or nominal, interest rate.

Assuming that interest is calculated—or compounded—more than once a year, the AER will be higher than the stated interest rate. The more compounding periods, the greater the difference between the two will be.”

Thanks for posting this, Nikolas and 2WR. The AER “dirty” from the quantwolf site for PRIF-L is 10.137%, very close to the 10.143% I got by using Excel and Goalseek. I probably won’t dig in to figure out why I’m off by six thousandths of a percent. The bottom line for me is that I should probably sell my puny holding in PRIF-J and use the funds to buy PRIF-F. (Thanks, Tim for that insight.)

It is very unlikely that any of these issues will be called with rising rates , upcoming recession and weakening credit markets . I would be looking mostly to on YTM not YTW. Do You have YTM calculations on the site ? . Thanks

Sachem is cutting div on common, per wsj Div changes column.

SACH paid $0.12 in April 2019, July 2019, October 2019, and January 2020. Then the company skipped a dividend, and went back to paying $0.12 per quarter from August 2020 to April 2022. The July 2022 dividend was an increase to $0.14 per share, and the recently declared dividend payable on November 14th, 2022 was reduced to $0.13 per share. So yes, the dividend was cut, but only by a penny, and it’s still above most of the recent dividends.

https://www.dividend.com/stocks/financials/specialty-finance/mortgage-finance/sach-sachem-capital-corp/