In a week that could have seen big moves in the S&P500 – we didn’t see them. The S&P500 closed less than 1/10th of 1% lower over the previous week. The total range during the week was less than 2% bottom to top. With the PCE release on Friday I was expecting large moves and it simply didn’t happen. Lack of movement is fine with me–boring is good.

The 10 year treasury close 9 basis points higher on Friday at 4.34% in spite of some economic data which should have been favorable to rates. This morning rates are at 4.41%–up another 7 basis points.

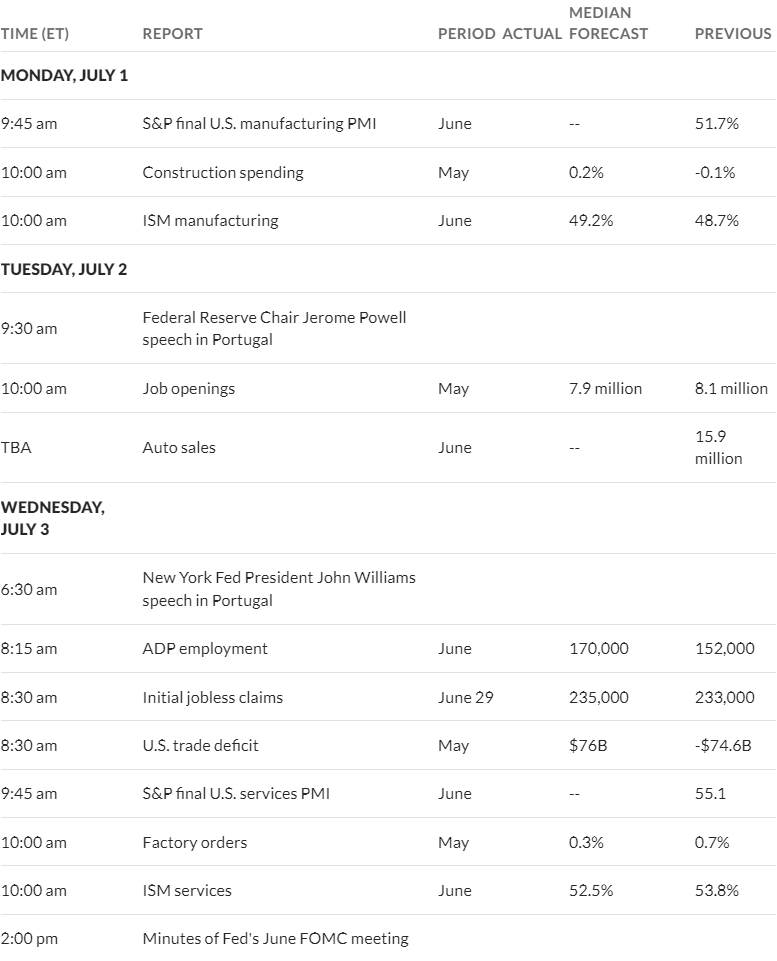

This week we have only modest amounts of economic news–importantly we have the employment numbers on Friday. We do have the release of the FOMC minutes for the June meeting on Wednesday.

The Fed balance sheet assets fell by $21 billion last week to move the balance sheet assets to $7.31 billion–along ways to go, but of course we will never–ever seen assets under 5-6 trillion in our lifetimes.

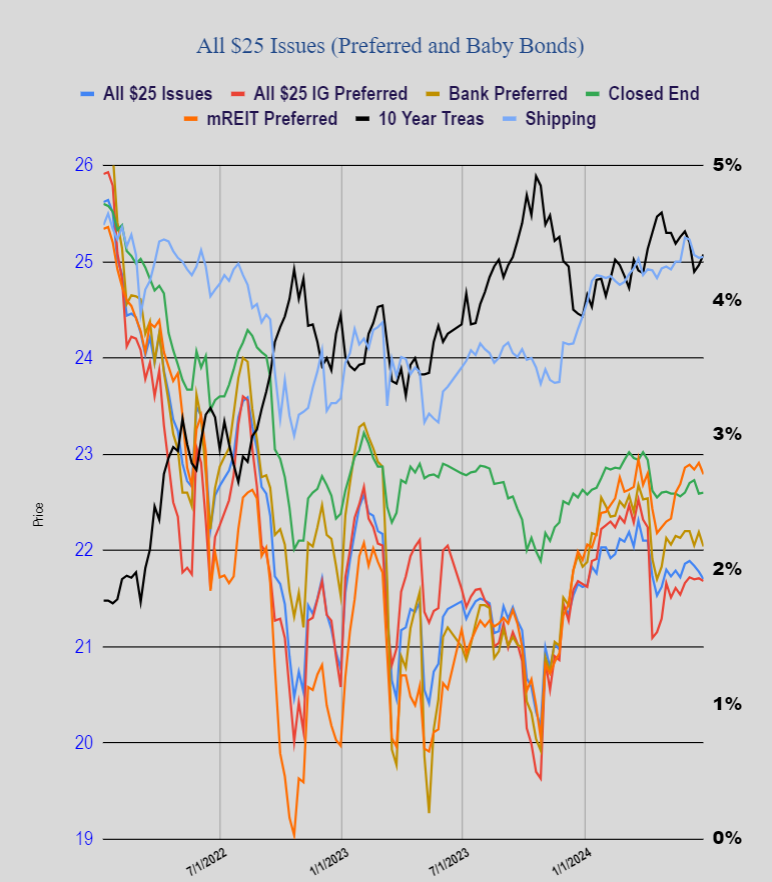

The average $25/share preferred and baby bond fell a little last week–8 cents. Investment grade issues were off 3 cents, banking issues fell 12 cents. CEF issues were up 1 cent with mREIT issues down 12 cents. It has been 10 weeks since we have seen the average share price move higher–we are living off dividend and interest payments–no capital gains to speak of.

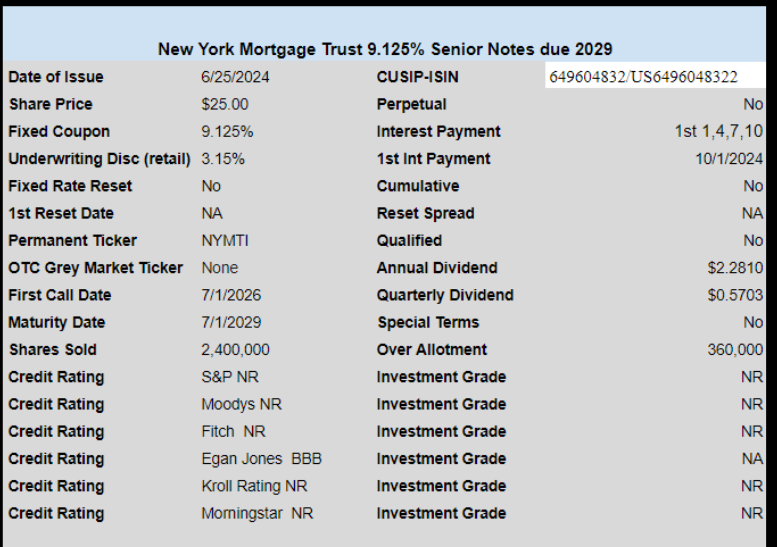

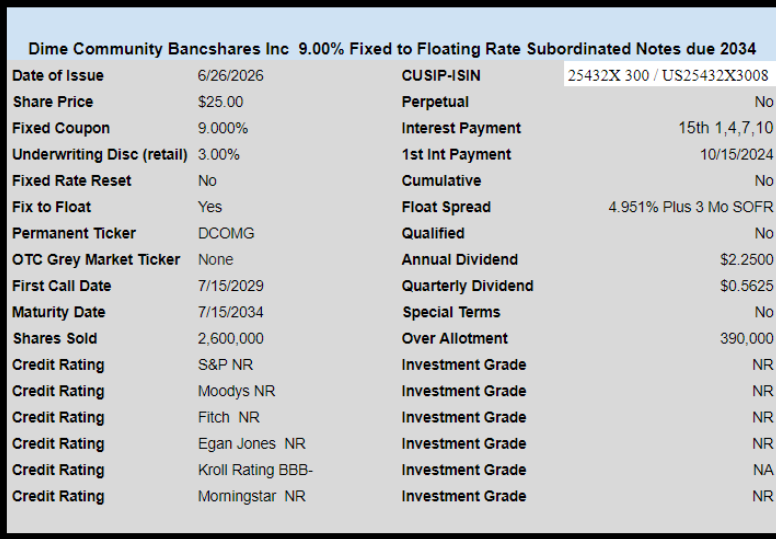

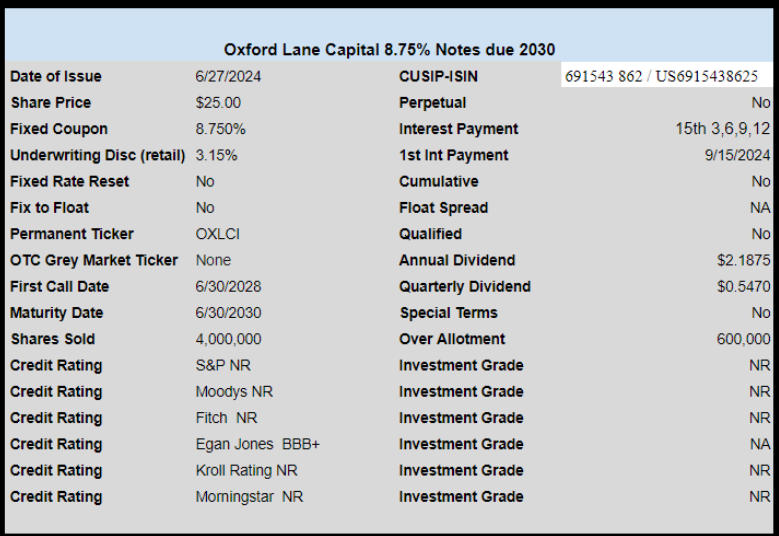

Last week we had 3 new issues priced–all baby bonds and all with fairly high coupons. It is interesting to note that over the course of the last year the number of baby bonds issued vastly outnumber the number of preferred issues that have been sold.

I’ll buy them all the first trading day