The S&P500 moved higher by 1.3% last week–a week of some contrasting economic news and some fairly large intraday swings. Jobs numbers, ADP on Wednesday and the official government jobs on Friday showed contrasting numbers–ADP coming in lighter than forecast and the official report coming in much hotter than forecast.

Interest rates were also knocked around with some large moves. The 10 year treasury moved in a range of 4.27% to 4.47%–closing the week at 4.43% which turns out to be 8 basis points below the 4.51% close the previous Friday. The 4.43% Friday close was 15 basis points higher than the Thursday close.

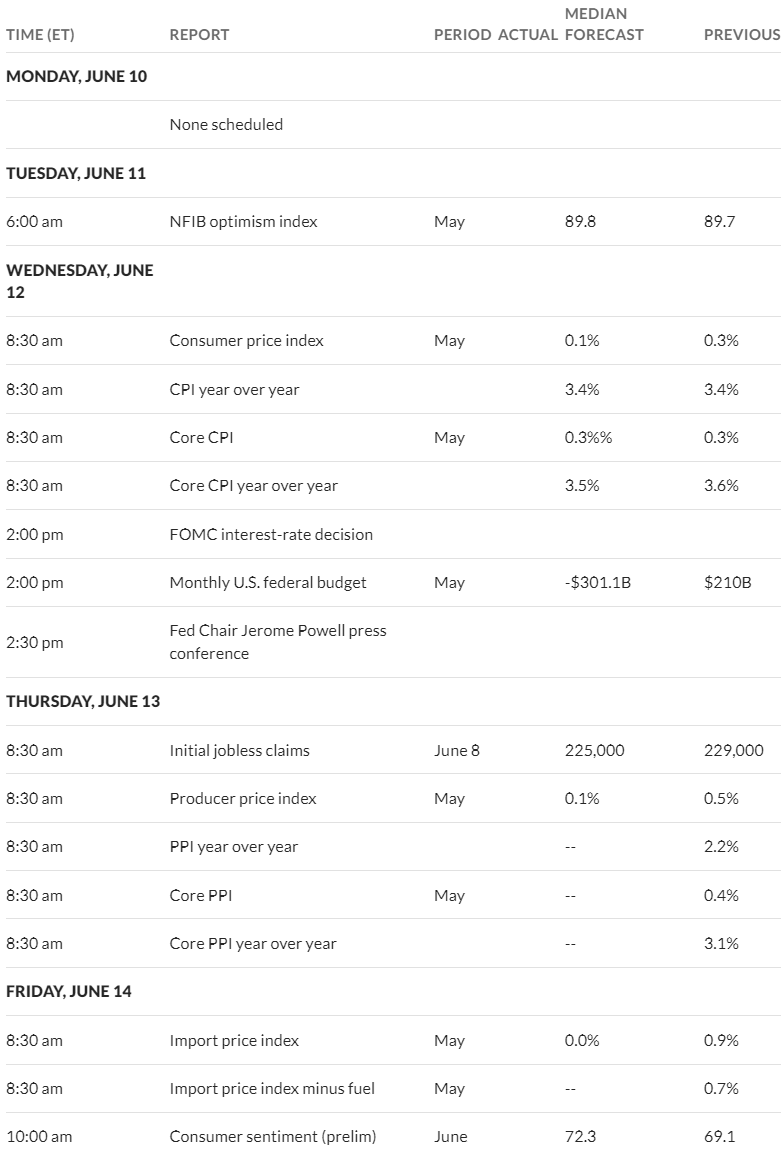

After last weeks news there is little time to rest on our laurels as we have important news for the coming week starting on Wednesday with the consumer price index (CPI). This is followed by the end of the FOMC meeting and the presser with Jay Powell. Follow this up with the producer price index (PPI) on Thursday and we could see some real moves in equities as well as interest rates. Well buckle up and we’ll see what the numbers bring.

The Fed Reserve balance sheet fell by $28 billion last week–a higher than trend fall. The balance sheet will move below $7 trillion this year–a good fall from the $9 trillion peak.

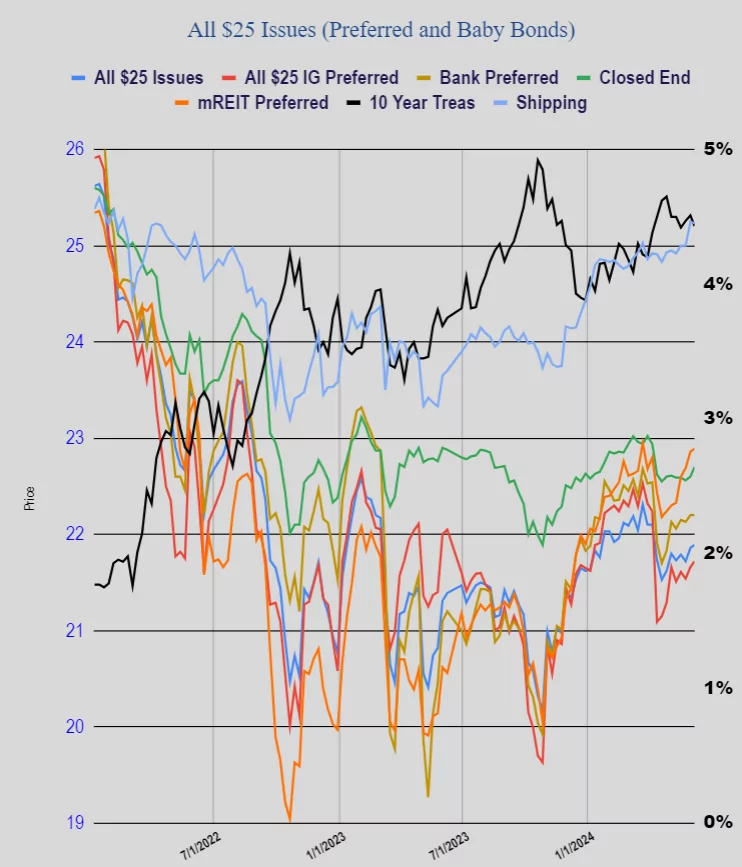

The average $25/share preferred and baby bond rose by 5 cents last week. Investment grade issues moved 6 cents higher, banks were flat, mREIT preferreds moved 3 cents higher. All in all a week where interest rates moved bunches–BUT income issues didn’t respond nearly as one might have expected–but with CPI, FOMC and PPI this week we can count on large potential movements to come.

Last week we didn’t have any new income issues price.