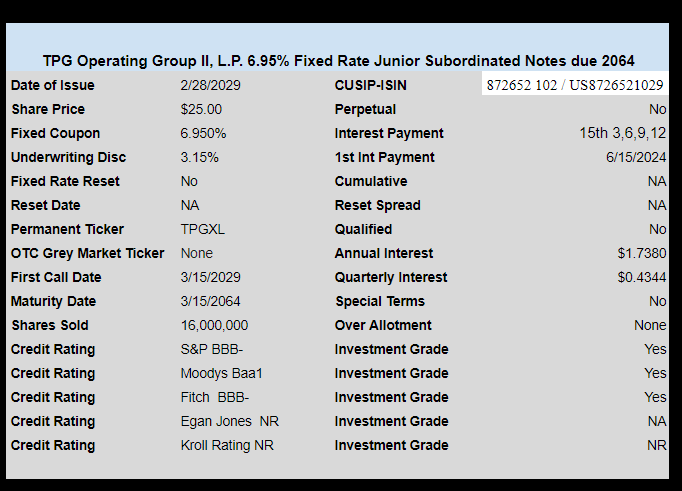

The new baby bonds from TPG Operating Group II, L.P. priced last night. They priced at a disappointingly low coupon—6.95%, although they are investment grade they have a maturity way out on 3/15/2064.

This issue contains the following provision–

The Issuer has the right, on one or more occasions, to defer the payment of interest on the notes for up to five consecutive years (each such period, an “optional deferral period”). During an optional deferral period, interest will continue to accrue on the notes, and deferred interest payments will accrue additional interest at a rate equal to the interest rate on the notes, compounded quarterly as of each interest payment date to the extent permitted by applicable law.

The pricing term sheet is here.

Underwriters discount 3.5% I would wait to see what it does when it starts trading.

My boss would say start selling at whatever you think you can get over 25.00 but don’t sell it for less than X then depending on sales he would come back and say don’t sell it for less than 24.75 finally when my boss says I want you to clear what is left of the inventory let it go for 24.30

Resist the urge to run out and spend your lunch money, wait and see how this trades

Not really a fan of the whole defer payments for 5 years. I tend to expect interest payments to be paid on time with no deferral.

With that said the above blurb mentions they are not cumulative but it does seem like they are.

I guess I will watch and wait on these. If they go under 25 by a reasonable amount I can see buying 100-300 shares.

FC

The 5 year deferral language is becoming ubiquitous. I don’t like either, but is seems to be everywhere on new issues.

I think the blurb says cumulative is “N/A”, not “No”. This is a baby bond, so cumulative/non-cumulative is not really a thing.

Junior subordinated notes very often are deferrable, and have been for a long time. It’s a cap stack slot thing for ratings. Utes PECO and Commonwealth Edison for example, have this deferrable feature in bonds issued ~25 years ago that are still outstanding and have never deferred. If viewed with their proper wink and nod purpose, that being a preferred stock but the company keeps the tax break, its nothing really to be concerned about provided you arent into dirt bag companies.

Not cumulative?

Cumulative only applies to dividends, not interest.

Long duration and a wide open 5-year provision at only 6.95% – nah. It will be interesting to see where this price when they open.

Does anyone know if/where (preferably free site/calculator) retail investors can input prices of bonds and preferred stocks and get an OAS number? Thanks!

OAS number???????????????

If you Prefer. I agree. Sentiment for credit is phenomenal.

IG OAS is 98 bps, which is close to it’s 25 year low. the Average over this period is 157 bps.

Basically, the market is not expecting meaningful defaults, unless it is CRE.

With that said, there are still plenty of opportunities in junkier or off the run names. I especially like mREIT prefs which can be misunderstood and still offer double digit YTM/C.

Or the off the run FI issues, including those mentioned on these boards many times: South Jersey or LNC floater issues.

IG https://fred.stlouisfed.org/series/BAMLC0A0CM

HY https://fred.stlouisfed.org/series/BAMLH0A0HYM2

I think that low coupon is an impressive statement of market sentiment!

Actually, as a BBB-/BBB-/Baa1 issues, 6.95% is not really out of place for the current market. It would have been great if it came in like the FGN issue last year at 7.95%.

Yepper, Proto, its right on the mark. FGN (which I own) just went exD today so it now pencils out to a 6.93% YTC on my calculator anyways.

FGN is undervalued which is why I own it. TPG is a slightly better credit and certainly bigger and more of a “brand name”, so 6.95% current yield at par is about as good as FGN 6.93% YTC at 26.

Deferable Jr subs from financials are typically rated the same as preferreds from financials but the jr subs are safer, particularly since they are cumulative.