UPDATE–I added a chart to the bottom of the screen.

The 10 year treasury has toyed with the 1% level today, before bouncing a little (a basis point or so).

The ‘talking heads’ breathlessly say ‘while waiting for the Fed policy decision from there current meeting’–I mean really?? If there is someone who believes the Fed will announce a slow down in QE at this juncture would you please raise your hand. Powell (and now with treasury secretary Yellen) is so dovish they he is growing feathers.

Equity markets continue to trade softly, even with stellar earnings releases from many bell weathers such as Microsoft. Market manipulation (legal or otherwise) has been obvious all week long–the Gamestop (GME) game has reached the new height of silliness–a 52 week range of $2.57 to almost $400–at this moment up $218/share to $366. Tanger (SKT) has benefited greatly from a short squeeze as well. Then there is movie theater operator AMC. Oh well–this to shall end.

Lately I have been studying the low coupon issues that have been being issued lately–to refresh my memory where they could trade if interest rates move higher. I looked at a bunch of issues–but I always come back to my personal favorite super high quality Tricontinental 5% perpetual (TY-P or TY-) issued in 1963.

This monthly chart shows that these shares have traded in a range of $18 to $59 since 1973 (as far back as my chart goes)–almost all of this interest rate driven. While many of us think we can forecast interest rates–we can’t. We can make guesses. This is just to remind folks that unless you are an ‘immediate income’ investor (most interested in current income flow without so much attention to share price) you can be bludgeoned into oblivion with these low coupon issues. Disclosure–I have recently sold all of this issue I owned.

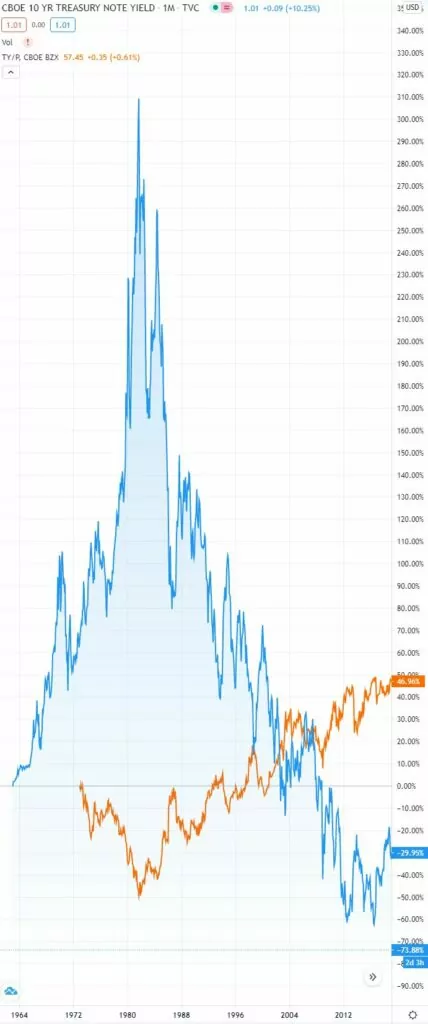

This giant sized chart shows the 10 year treasury yield compared to the TriContinental 5% prepetual. The blue is the 10 year treasury while the orange is the TY-P issue. Interest rates peaked in the early 1980’s and have been in a downward trend since that time.

Fed’s Kaplan Expects “Enthusiastic” Debate On Taper Timing — see Bloomberg story.

Now it’s like heads I lose, tails you win. Strong economy equals taper and higher rates and a potential bubble pop — leading to a weaker economy and concomitant potential credit risk drawdowns.

I really can’t whine and complain that I can’t generate any income in my retirement without taking risk, because I would never have had this amount of assets without the zero interest rate asset bubble. I know I can’t have it both ways — high asset prices and high rates.

You know the investing gods have succeeded when they have us talking about rates rising AND falling both in the last month. . .

I gonna have to go over to Reddit to figure out what is actually going to happen. (Sarcasm in case you thought that was a serious comment.)

Tex – and after you go to reddit, just to be sure you’ve got it right, head to SA. Load up on them LTS bonds!

I bought some additional shares of BKFAF (BAM.PR.B) today from BAM. It’s a floating rate preferred that is tied to the Canadian prime rate. I like this as a hedge to the impact of rising rates on the fixed rate preferreds that I hold.

The yield I’m getting is around 4.2% on today’s purchases. It’s trading signifantly under par around $8. It has traded around $14 within the past few years on expectations on rising rates.

You can buy this in an IRA with Schwab and they do not withhold Canadian taxes.

If I’m wrong and rates stay low, I’ll collect 4.2%. If I’m right, BKFAF shares can potentially appreciate by 75%.

Dick, I have edged into a few floats and resets which number about 16 positions now. I care NOT about the short term fluctuations in trader land. I feel the trend in five years will be up on real rates and I will need to buy goods and services at a higher price.

I just did a review of ENB and recently bot some common to collect div and sell close-in, OTM calls on since I am bullish on their operation and management. It is my largest position with common and two prefs. The Keystone rejection should even help them in my mind, but the replacement (read: super-redundant, upgrade to aging, existing infrastructure at NO govt expense) of the Mac Straits pipeline is a very short sighted and inflationary bottleneck that will not be recognized until it is been killed too? It will not harm ENB if they shut it off tom. They have other things to place their funds on, like building out super-grid capabilities elsewhere…just another pipeline!

All that to say that ENB.PR.V (make sure it is the PR or PF) in USD is also a screaming buy and I recall there is an OTC symbol for it as well. I moved it over to IBKR. Resets in four years or so. If I had to hold one security and cash, this would prob be the one.

Joel – just to clarify: ENB.PR.V = EBBGF and ENB.PF.V = EBGEF. EBBGF [ENB.PR.V} resets 6/1/23 and EBGEF [ENB.PR.V] resets 3/1/24. I’m long EPGEF….

2wr, Glad you clarified the research. I was being lazy in my reporting. I did remember the tricky PF and PR so I get a macaroon with my tea today.

I have sold all OTCs at TD and migrated all CNs over to IBKR, hence pitched all that old encryption codes to TSX/OTC.

Glad to notice that my brain is still kind of operating while listening to my arteries harden during this Lockdown.

I may not have waded through the migration (just realized the Freudian pun) to Canada if good roadsigns and dead reckoning had not been posted on this site.

Sorry, no commission sharing advisory agreements are in place in my records.

Further comments re Canada Issues: I have avoided the one-sided contracts and uber-love by the Canadians of their beloved bank issues with above par prices, NVCC, mezzanine tranche stacking, low rates, call risk and near a top in systemic risk with bloated real estate, dependency on govt payments to their clients and house of cards debt. We have NOT seen a real, cleansing washout in a very long time. This is true with US Banks too. I do not want to go through their workout as a business partner someday when the contract gives me no-thing.

Not saying when…I’ll have to look at the tea leaves when I’m done.

Here’s to the House! JA

2WH

I think you have two many V’s in your Enbridge map above.

I have the OTC matching as:

ENB.PR.U as EBBNF

ENB.PR.V as EBGEF

I’m long both (as well as the common)

Greg – You’ve got the right symbols for both of the shares you mention however, EBBGF, which you did not mention, does equal ENB.PF.V .

Cross reference https://www.enbridge.com/~/media/Enb/Documents/Investor%20Relations/DividendandShare/ENB_Securities_Prefs_Summary.pdf?la=en with QOL OR there’ve been at least two III’ers who’ve offered their in depth spreadsheets if you can find them…

No one should forget that it was Janet Yellen as Fed Chairman who last raised interest rates, and as recently as Sept 2020 stood by her decision to do so. The notion that she has changed her position that interest rates can be raised without derailing economic expansion is misguided. If the pandemic eases and growth ramps up, I’d expect Yellen to be supportive of the Fed raising rates.

CW, that is not correct. Jay Powell was the Fed chair who raised rates until the stock market cried “Uncle!” in the 4th quarter of 2018.

Yes, Yellen has always been a fan of zero interest rates.

Ok…then it was Yellen who began the interest rate increases in 2015 with Powell continuing the policy after he took over from her in 2018. -btw I disagree with the characterization that Wall St. cried uncle in Q4 2018…it was more like they crashed the markets until the Fed cried uncle on providing easy money.

Agree, 1/4pt in ’15, 1/4pt in’16 and 3 ^ in ’17, after 6 years of near zero

rates. The ’18 Powell increases led to short-lived online bank rates of 2%.

To quote Ralph Nader(to Yellen: “It does not seem fair to put the burden of your Federal Reserve’s monetary policies on the backs of those Americans who are the least positioned to demand fair play” That is, the millions of

Savers who had counted on bank interest to supplement their Social

Security.

Heron, Thanks to that uptick a few years ago, I was able to get my step mom into a bunch of longer duration 4% CDs. I have already warned her in a few years if things dont change she wont be getting that yield next time around.

Gridbird, Good move. The best I could find at that time was 3 yr Wells Fargo

CD’s at 3%.

Does anyone think the Fed has the stones to eventually take rates negative after having printed 25% of the dollars in circulation last year?

Dovish ?

Yes, but with the demand destruction from the pandemic, we may be in a destructive policy loop. Stick with it, screwed, change it, and still screwed.

I am looking at lower coupon higher quality issues USB-Q and OPP-A

and maybe some higher risk issues like ECCX to juice income with a partial position. I wish i knew what was going on with AFC. IG past call at $26.

Pickel–I own OPP-A–but am watching it closely–it is the only sub 5 that I own. I have OXLC and ECC issues to try to juice income like you.

Tim,

I’ve heard so much from you on the OPP-A I picked up 100 today at $24.82.

It’s got the A1 and the 400+% coverage so that’s comforting.

Looks like they buy a mish-mash of fixed and other income instruments, chew on them, and spit out a distribution.

Ah, the art of sophisticated investing.

I believe ARCC has indicated it has no interest in calling AFC (quoting BDC Buzz, who is the subject matter expert).

If you might be interested in the egghead version of what Tim’s saying, here’s where you can read a definition of “duration.” https://www.investopedia.com/terms/d/duration.asp. It essentially explains in an academic way why these 4% versions of new issues will tend to go down much faster when interest rates rise than the already outstanding higher coupon versions of the same issuer.

Thanks 2wr

Thanks, Tim Good info.

Tim, when you say low coupon are you talking sub 5%?

libero–yes I am mainly talking sub 5. The TY issue is a good example because I have 50 year chart through many interest rate cycles.

Tim, the key to understanding the chart is one must know the general long end yield trend at that snap shot in time and the exact 10 yr yield and general economic situation. Most oldies here know, but for newbees, in reference to say 1982 price action above, the 10 year bond was around 13%.

Yes Grid–agree. If I was a smart person I would have laid rates into the chart. Will try to do that maybe tonight.

Tim, I roughly know them in my head all the way to the 1940s, as that exercise helps me undertand the historical push/pull rate environments have had historically on issue yields and pricing action….But putting it on a chart to see? Well I would need a pencil, ruler, and graph paper, lol.

Grid–I did get a chart – just posted to the article. But I know what you are talking about—I could draw it with a pencil in 5 minutes–more time to do it with my computer.