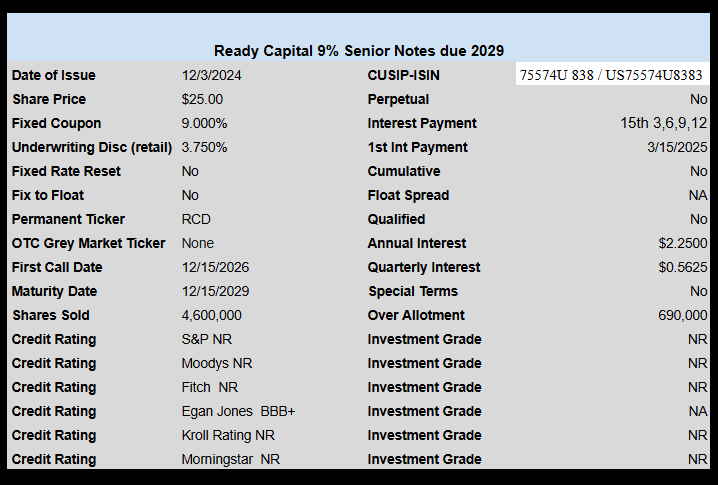

Ready Capital (RC) has priced their new issue of baby bonds with a high coupon of 9%. The early redemption period starts 12/15/2026 with maturity on 12/15/2029.

2 baby bonds that are currently outstanding from RC are trading with current yields around 5.90% and 6.38% respectively–could be messy for these 2 issues tomorrow.

The pricing term sheet can be read here.

Users who liked this:

Quantumonline has them paying 6.2%

“Interest distributions of 6.20% per annum ($1.55 per annum or $0.3875 per quarter) will be paid quarterly on 3/15, 6/15, 9/15 & 12/15 to holders of record on the record date that will be 1/15, 4/15, 7/15 & 10/15 respectively (NOTE: the ex-dividend date is one business day prior to the record date).”

11% of the equity side is being shorted, anything over 5% is a red flag…

I would absolutely worry about the risk of bankruptcy. In fact just for fun plugged it into google and the following came up, fwiw

https://valueinvesting.io/RC/probability-of-bankruptcy#:~:text=The%20Probability%20of%20Bankruptcy%20of,current%20fundamentals%20and%20market%20conditions.

I’m still in awe that companies can pay 9% to raise capital and make a profit lending it out. There are also some raising funds at these rates to pay off debt coming due to avoid bankruptcy. The trick is to separate the two and avoid the BK folks.

DJ:

“I’m still in awe that companies can pay 9% to raise capital and make a profit lending it out.”

Good point. Another commercial mortgage REIT (Arbor – ABR) did the same thing a few months ago when they raised unsecured notes at 9%.

Leverage. Boost the return but also bigger losses if it turns south.

Both baby bonds have yield-to-maturity of 8.75%. So in line with the new one.

Pays a good deal more than the perpetuals. That’s rare. Maybe because the perps are so low the potential price upside is baked in.