Well after a long weekend (at least for some) we are ready to get to going on the investment week.

We will of course have the Biden/Harris inauguration on Wednesday of this week. I don’t think there will immediate investing consequences–more of a wait and see for a week or two.

We had a fairly rare loss in the equity markets as the S&P500 fell by about 1.5% as the index closed at 3768 which is down from the close the previous Friday of 3825. Certainly common shares have looked ‘tired’ lately as the run–up since the Covid bottom has been pretty dramatic–with all the free money sloshing around.

The 10 year treasury stabilized last week awaiting more data. The bond closed at about 1.10% after closing the week before at 1.11%. After the near 20 basis point move the previous week and the resultant relatively minor losses in some preferred shares and baby bonds those shares were able to stabilize and gain a few cents of those losses back.

Last week we had a small gain of 5 cents in the average $25/share baby bond and preferred stock. Investment grade moved 2 cents higher, mREIT preferred shares by 2 cents, shipping by 26 cents (but there are not many of them) and banks moved 2 cents. All in all let’s just call it flat on the week.

Last week we had a few new income issues priced.

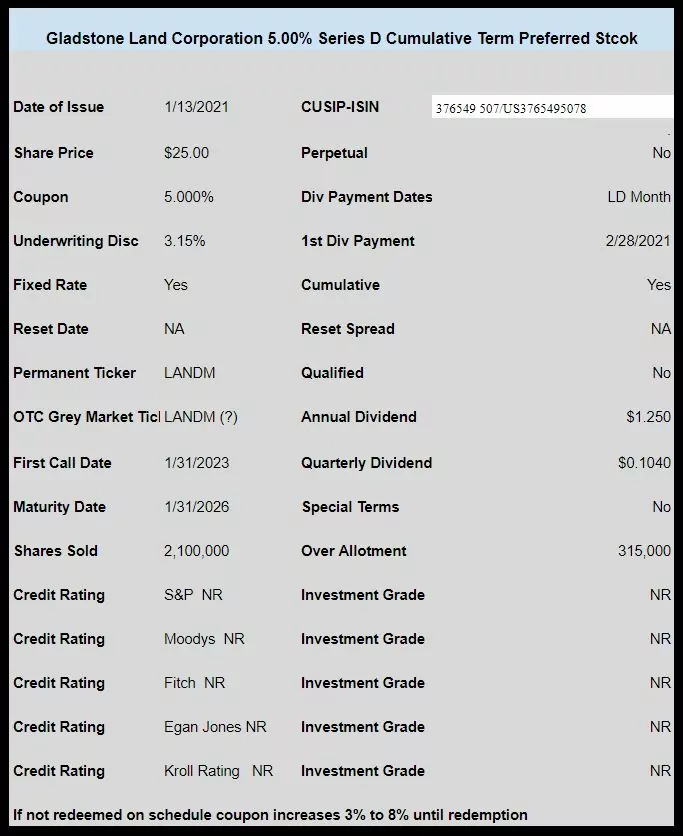

REIT Gladstone Land (Land) priced a ‘term’ preferred with a meager coupon of 5%. The issue is trading under the OTC grey market ticker of LANPP (ignore OTC ticker in chart below) and closed last week at $25.25—folks love the ‘term’ preferreds.

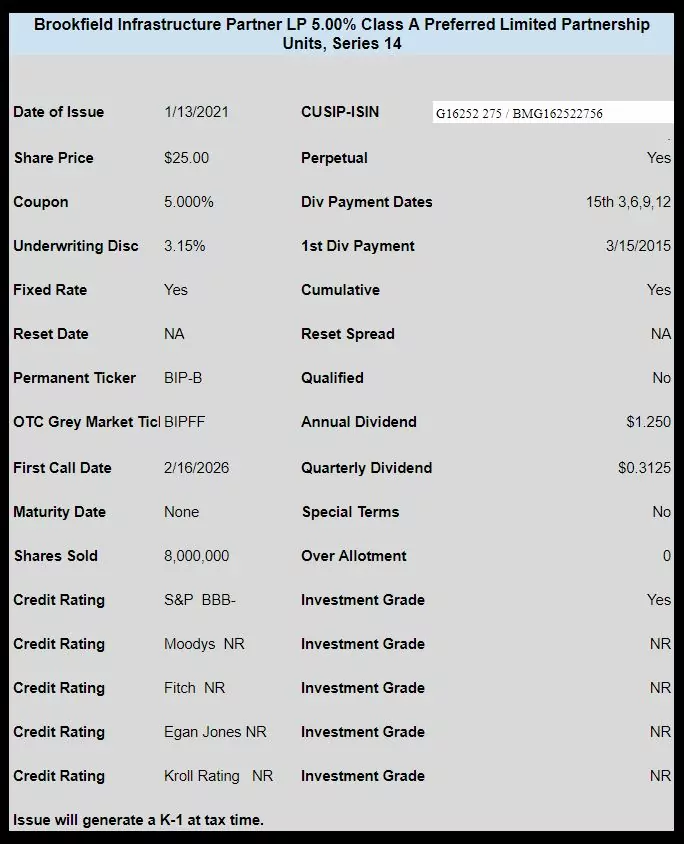

Additionally Brookfield Infrastructure Partners LP (BIP) sold a 5% investment grade perpetual preferred. This will generate a K-1 at tax time. This issue closed at $24.74 last week.

On top of these new issues Franchise Group (FRG) ‘reopened’ their 7.50% perpetual preferred (FRGAP) by selling around 3 million shares at $25.20. This reopening knocked the shares much lower–from near $26/share prior to the offering to close the week at $24.68.

2WR, History has shown I do a lot better dating than marrying. GF of past 14 years running just moved in a few months ago. Baby steps, ha…. Oh we were talking about stocks…Its that way too. I was stunned by the links shown here by a few posters what the annual return for a preferred stock held for a year was last year, basically nothing. Holding instead of trading would have almost been as expensive for me as a divorce would be…Almost, lol.

My mystery lyric of choice, having consulted with GF first, had to be one of two – either the one posted or this one… LOL :

“Don’t kiss me, don’t claw me

Don’t pet me, don’t paw me

I won’t leave my freedom behind”

So I say, “You know what?”

She says, “What?”, I say, “What?

Oh, I’m not the marrying kind”

The key is to get a few timely divorces. If an investor was able to avoid the enormous drawdowns (like 2007-2009 and March 2020), returns increase significantly. I’m too sensitive and typically separate far too early, but I do find new mates during market breaks.

As we are closing in on Tom Demark’s 3907 target on the S&P 500 and interest rates have begun to rise, it’s probably time for me to consider some judicial separation and dissolution.

“I don’t think there will immediate investing consequences”

I wonder if we won’t get a relief-jump if there’s absolutely no violence.

There has been a gentle rollover of some of the ‘better’ shopping center pfds UBP/ BFS w yields rising- I guess to be expected given the jump in the 10yr. I put the pfds of both back on my radar. Bea

wow–you’re right Bea. I had been in and out of the BFS issues a month or so ago–but left them as overvalued–looks like it is time to add back to the watch list.

thanx to your pfd gainer loser spreadsheet again, Tim!!!! Bea

Thanks Tim. I’m bullish for ‘21 and see SPX above 4000 this year. At the moment, sentiment is to bullish and margin debt is at ATH. I’m short above 3800 but will stop out above 3830. I think we get a short term correction and will load up if we get it. ATB.

Hi Tim…. PBI-B giving 6.7% return ,every company, is shipping something, and needs their equipment .. never missed a payment ……. still hold off ???

$18.93/sh worked for me.

Georges–I just checked and updated the credit ratings for PBI—they had starting investment grade years ago–but now Moodys has them at B1 and S&P at BB–not good. I personally don’t like the company, but with teh current yield of 7.17% maybe it works for someone with a higher risk tolerance.

PBI is not just a postage meter company any longer. For the last 8 years they have invested heavily in e-commerce, and that investment has been paying off (the company did $140 million in EBITDA during the third quarter and $400 million the first 9 months of 2020).

E-commerce revenues were up 47% during the 3Q. The stock advanced 60% in 2020. PBI owns 15 domestic parcel sortation centers and 4 fulfillment centers.

There also have a very big business in e-commerce returns, as they bought a private company called Newgistics a few years back that proved extremely timely. I consider the company a mini-FedEx or baby UPS.

Own both the baby bonds and common and it has worked out very well so far.

I believe those baby bonds are “money good”. My biggest fear is that the company will redeem them and I lose the monster yield they have been providing. The bonds have been callable since March 2018.

Rob, I wont marry this lady, but I date her frequently. Just got out on another buck a share bang out last week. Have done that several times in past few months. Just riding it up and holding would have been just as good if not better. But I just am personally “not there” yet. But…I do keep her phone number handy, lol.

I gave you my heart, babe

But you wanted my mind, oh yeah

Your love scared me to death, boy

‘Cuz it’s the chokin’ kind

Rob–am well aware of the changes over the years, but I seldom by issues rated this low. Fine for some just not necessarily for all.

Rob:

You are exactly right that this company is not an old stodgy postage meter company. PBI stock price has gone from a low of $1.75 to over $6.50 in the last 52 weeks. The PBI bonds for me have gone from $17 to $23.00 and have paid the interest on time without hesitation. There was a Wall Street Journal article favorable to Pitney Bowes last August that I mentioned on this site. Thank you Rob for laying out the case for PBI investment. I thought I was alone in my commitment to Pitney Bowes. Glad to see Gridbird is even stepping his toes into PBI waters and Tim has some favorable comments.