Time to get back to real life after too many holidays – at least for me. In Minnesota with snowy and cold weather, being inside for these days is not to my liking. On the other other hand if you are a skier (downhill or cross country) or a snow machine rider maybe you are loving it. Obviously I live in the wrong state.

So last week, which was a 4 day market week, the S&P500 was off just 1/10th% as the trading range for the week was just about 1 1/2%–narrow considering recent history. Economic news was fairly sparse which helped in keeping the range narrow—but it is unlikely to be that way in the coming week.

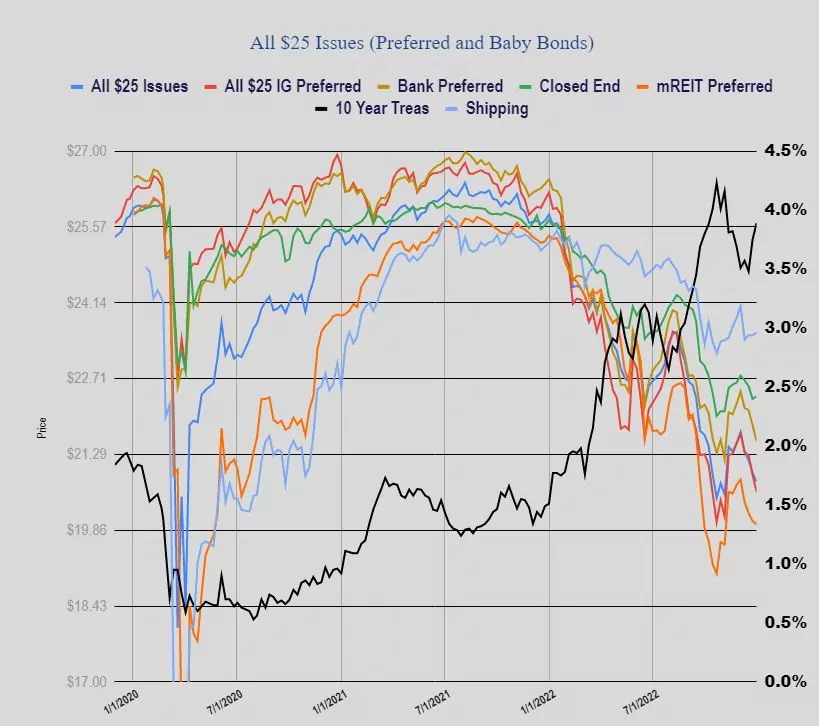

The 10 year treasury was up 13 basis points to close the week at 3.88% compared to a close at 3.75% the previous Friday. The high yield for the week was 3.91% so we closed near the top.

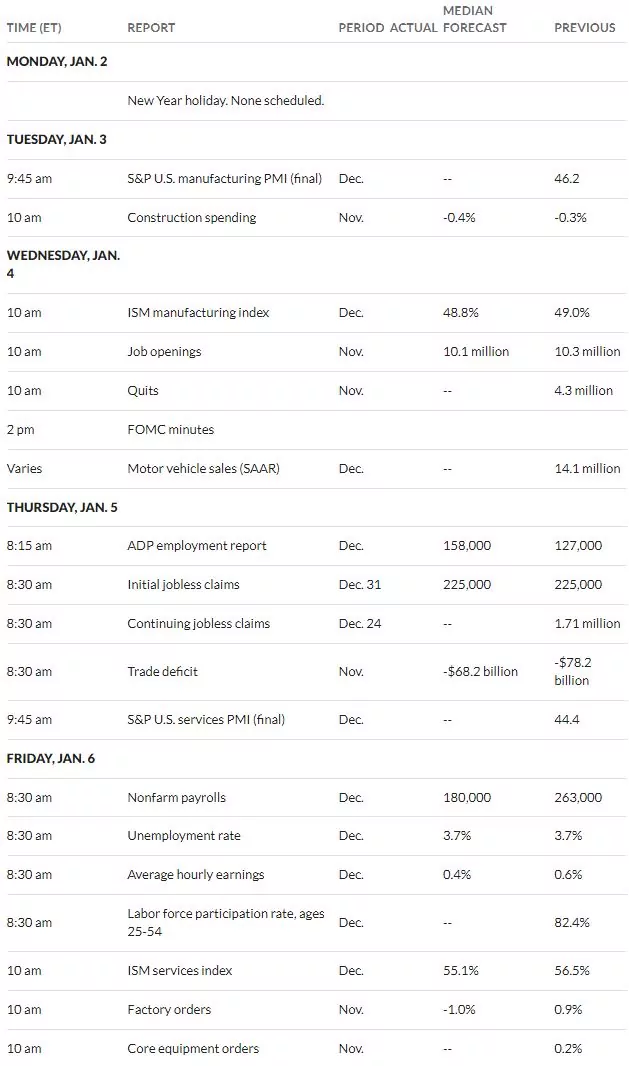

For the coming week we have a number of economic reports which will be market moving. We have the FOMC meeting minutes released on Wednesday for the last meeting and while it is ‘old news’ it will move markets. We have employment reports on Wednesday and Friday (ADP and then the government report on Friday)—this will move markets as the FED will assign a high weighting to the report for the FOMC meeting which happens on 1/31 and 2/1. They really want some softening in the jobs market.

The Federal Reserve balance sheet was down $13 billion last week–likely creating a little ‘tension’ for future numbers as the Fed looks at their monthly caps (maximum) of reductions of $95 billion, which they have been way below the last month. The Fed reserves the right to adjust their monthly cap dependent on financial conditions–a section of their statement on reducing the balance sheet is below –

Last week we again saw losses in most $25/share preferred stocks and baby bonds – this time to the tune of 17 cents per average share. Investment grade issues were hammered lower by 32 cents, while banks were off the same 32 cents. mREIT preferreds were down just 6 cents and shipping issues were up a nickel.

Last week we had no new income issues prices.

A note, as mentioned by a couple folks over the weekend is that the Hoegh LNG Partners 8.75% perpetual (HMLP-A) issue is now delisted – effective today.

2023 KICKOFF ON TUESDAY worked on this over the weekend, today was the first day to take advantaged, so I pulled the string, took part of my “23 RMD today. moved 500 shares of GDV-H from my Ira to my taxable account@23.06 that’s a yield of 5.82% and a qualified dividend. so much for the first trading day of the year. Think I’ll quite while I’m ahead.

Mike – How I hate to expose my ignorance, but it’s real easy for me to do (again) on tax issues… I don’t get it – what does this accomplish for you? It doesn’t seem braggable to me but as I’ve previously confessed, I’ve always only settled RMD in the past by moving cash….

2WR, let’s say you own XYZ $25 face preferred which is currently trading @ $12.5. But you think it might eventually recover to $25. When you transfer it to a ROTH, the IRS values it @ $12.5, so you think you ~ doubled the additional income stream as opposed to transferring it when it was $25.

We recommended this to everyone back in March 2020 to do this if they could. Particularly if they had to satisfy a MRD.

it is a good and legal strategy to increase you untaxed ROTH income, so that comes out tax free. (At least for now, but long term it is debatable.)

Tex – But that’s not what Mike described….. He’s satisfying his MRD or part of it by taking out a 2 point discounted from “par” security and transferring it into a taxable account, isn’t he?….. Unless the thing to be thankful for is moving this in hopes of an eventual long term capital gain in a taxable account instead of ordinary income, I’m missing the exciting part of the reasoning…. It could be there and I’m not trying to knock Mike, I’m just not seeing the sizzle…

Tex-

You can’t do a move/conversion from a TIRA to a ROTH to satisfy all or part of your RMD. You can move money or stocks to your taxable to meet the full RMD, but it must all be done before a penny can go to the ROTH.

Gary, you are 100% right. I mistated it. We did move a lot of beaten down issues from regular IRA’s to ROTH’s, but they were NOT part of MRDS. They were all done for people under 70 1/2, which are not required to do MRD’s, My apologies.

BTW, the new Secure Act 2.0 which was signed into law last week raised the age for starting MRD’s to 73.

2WR AND TEX , not to get overly specific but qualified dividend’ s an long term gains are essentially tax free in my tax bracket. gdv-h drips with both, and quality, Tax planning is a whole lot easier than staking nickels, not bragging guys just “pointing” out another way to skin the cat. all kinds of resources on this topic available

Thanks, Mike – please don’t misunderstand my use of “bragging.” It wasn’t meant to be derogatory – just a way of saying I didn’t understand what made you want to post….. given your circumstance, there is more of a Roth like impact to the strategy…

no offense 2WR, you got the idea now, as far as my roth ira, I got my maxed out mlp’s and quality reits, an some ordinary taxable income issues.

Our area of NV had 16″ of snow- 9F at night, but managed to have highways clear in a day or so. More to come in the next 3- 5 days… erk!

Gary, I think I saw Grid packing up his snow skis. He will probably show up @ Tahoe/Mammoth tomorrow. . .