You just can’t keep this equity market down – all is good in the world, no issues to worry about and economic growth and prosperity will go on and on (tongue in cheek of course. The S&P500 rose again last week closing at 4582 Friday which amounts to a gain of 46 points (1%).

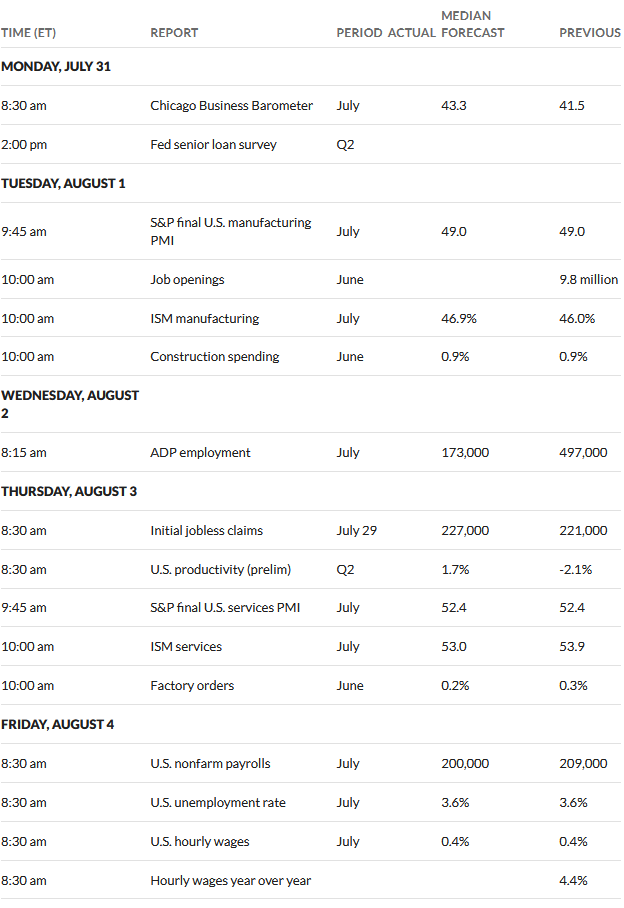

Interest rates (the 10 year treasury) spiked higher last week as economic news remained fairly strong. The 10 year hit 4.02% during the week before backing off to close at 3.97%–a 13 basis point gain from the previous Friday. This week the most important economic news will be the employment report on Friday which has a forecast of 200,000 new jobs.

The Federal Reserve balance sheet continued to move lower–falling by $31 billion last week. Certainly the Fed has not shown any inclination to back off on the balance sheet runoff–and there is no reason to think this will change until we reach the point in time where the economy starts to stumble a bit–in the mean time the Fed is building ‘dry powder’ for future economic troubles. In this case ‘dry powder’ is having the capacity to ‘print money’ in case of a black swan event or a deep recession.

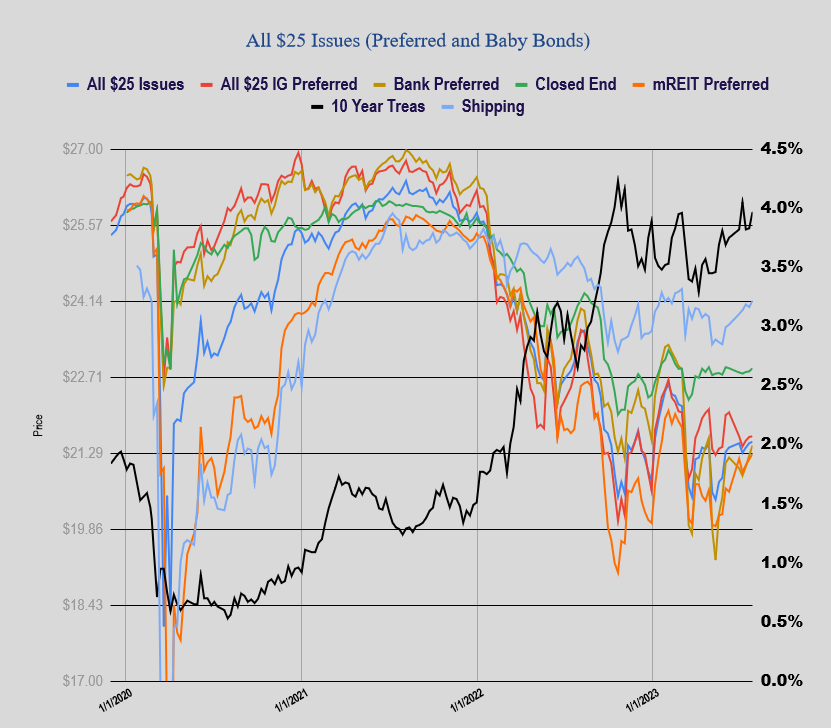

The average $25/share preferred and baby bond rose by 8 cents last week. Investment grade issues rose 1 penny, banking issues rose 19 cents, mREIT preferreds moved a dime higher while shippers moved 12 cents higher.

We continue to await the new 7.75% term preferred issue from Eagle Point Income (EIC). I see that eTrade and Fido both have the issue set up, but no trading has taken place as far as I can tell–maybe today.

EICA (5% term preferred maturing Oct’26) ~23.45 for a 5.33% current yield

EICB (7.75% term preferred maturing Jul’28) ~24.95 for a 7.77% current yield

Risk is basically the same. Longer term, much higher rate. I swapped out this morning. (not sure if I am missing something)

RTL

730 Cap–Right you are! Thanks for the help–you are better than Schwab reps who obviously don’t know much about what they trade….

I just successfully purchased EICPB at ETrade for 24.90

Adrian and others reporting trades at Schwab: not sure how you can do that, as I have a Schwab account, tried to place an order with both EICB and EICPB.

Neither symbol works to get a quote. 3 different Schwab reps told me Schwab allows only closing orders in grey market securities……

As Private explained recently, there are at least 3 different ways to place a trade at Schwab. Using the quote box at the bottom of the page is working for “EICPB” (even though ticker is supposed to be EICB lol)

I was able to do it with the snap ticket at Schwab. No OTC fee either. It surprised me but it did work, got it for $24.95

I am thinking we all getting excited about a new issue. Yet looking at Yahoo, I don’t see any large volume. Not sure if it’s real time. I suspect if volume doesn’t pick up the price will drop. Love to see it with a 8% yield but that’s wishful thinking. See if my low-ball bid hits

Is EICA going to continue to trade at a yield of less than 5.5% while EICB trades at 8%? I know it has an earlier maturity, but that seems like a huge disparity.

Which do you prefer:

EICB or OBDC?

Schwab let me place an order, and no OTC $6.95 fee !! Not filled so far.

bought 200 EICPB thru Schwab at 24.95

Well I take it back, they allowed me to enter a bid then when I looked they dropped it.

For Fido try EIC/PB

Trading @ TDA as EICPB at 25

Can someone clarify why buy EICPB @ $25 (7.75% div.) rather than ECCPD @ $20.65 (8.15% div.)

Maybe because ECC earnings come from the iffier equity tranches, vs EIC’s debt- higher up.

etsfl – ECC invests in primarily equity tranches of CLOs which are generally a higher risk than the debt tranche of CLOs which is what EIC primarily invests in.

This from prospectus of series D preferred stock (ECCPD)

“The shares of Series D Preferred Stock will rank equally in right with all other preferred stock (including the Series B Term Preferred Stock and the Series C Term Preferred Stock) that we have issued or may issue from time to time in accordance with the 1940 Act, if any, as to payment of dividends and the distribution of our assets upon dissolution, liquidation or winding up of our affairs. The shares of Series D Preferred Stock, together with the Series B Term Preferred Stock, the Series C Term Preferred Stock and all other preferred stock that we may issue from time to time in accordance with the 1940 Act, if any, will rank senior to our common stock as to payment of dividends and the distribution of our assets upon dissolution, liquidation or winding up of our affairs and subordinate to the rights of holders of our existing and future senior indebtedness (including the 2027 Notes, 2028 Notes and 2031 Notes).”

It’s a matter of safety, noted above- – EIC wins.

Yup, matter of safety. You can get a deck chair closer to the stern, or closer to the bow…

If they default on one, I think the whole thing will collapse – but that is just my curmudgeonly view.

Perpetual Preferred(ECCPD) vs Term Preferred (EICPB)

etsfl – you’re also comparing a term preferred with a 5 year “maturity” to a perpetual preferred with no stated maturity which for many people for whom duration risk is something to consider makes your comparison apples to oranges… So not only riskier investment strategy but duration risk as well.

EIC/PB does not work at Fidelity. The temporary symbol is EICPB. Unfortunately, it can’t be traded at Fido. I was blocked online because it’s grey market, and a Fido trader just confirmed on a call that he, too, is unable to place any trades for that reason.

If anyone has luck with some other broker(s), please let us know. Thx.

just successfully bought at TDA, $24.95

Hi Wilson – you are correct – couldn’t buy at Fido. Just placed an order on eTrade though.

Eagle Point is trading. My one broker has it as EICPB

Fidelity is now recognizing EICPB, but Big Brother will not allow an opening purchase in the grey market. Haven’t tried calling. That’s probably what it will take.

Order for EICPB @ Schwab just confirmed @ $24.95. Trading as high as 24.98, but bid / ask not currently listed. FWIW.

Thanks Charles – I see it now and have an order in at eTrade