Well time to start another week and see if the S&P500 continues to ‘levitate’ or if common share holders decide to bring things down to what some might believe is more reasonable price levels. My hope is that if shares move lower they will do it in an orderly fashion. We all remember the days of drops of 2,3 or 4%—not something we have seen in quite a while. While I generally hold little–if any common shares I never what to see dramatic sell-offs–I guarantee a sharp sell-off will drag preferreds and baby bonds lower and I am getting used to seeing green most days.

Last week the S&P500 moved up by just a hair over 1% from the previous Fridays close. This leaves us just a little bit below and all time high which was hit earlier in the day on Friday. Apple and Microsoft both report earnings this coming week and will set the tone for further gains or losses in the index. Last week Tesla got hammered (by over $30/share) and kept the S&P500 from moving even higher.

The 10 year treasury closed the week at 4.16% which was a measly 1 basis point higher than the close the previous Friday. Economic news was mixed on the week–but markets were laser focused on anything relative to an inflation number. Some inflation related numbers showed inflation under control–but not necessarily moving lower at this time.

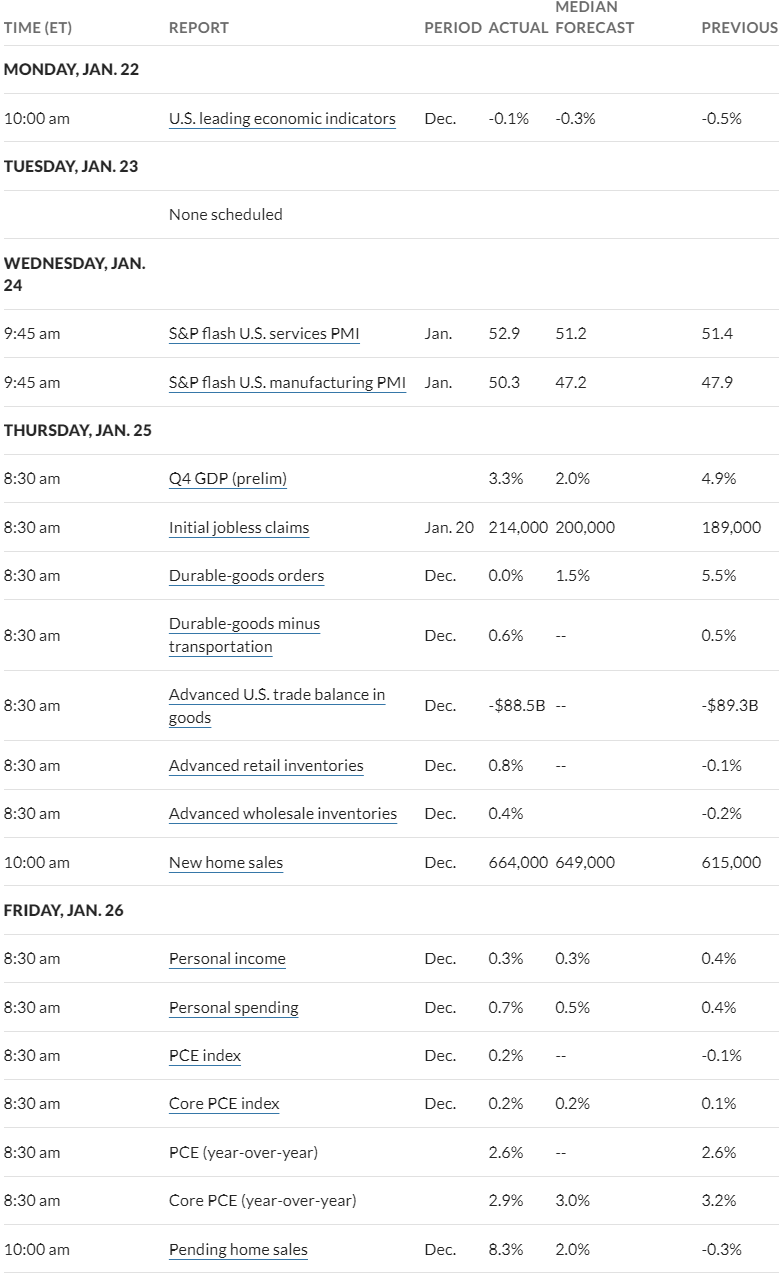

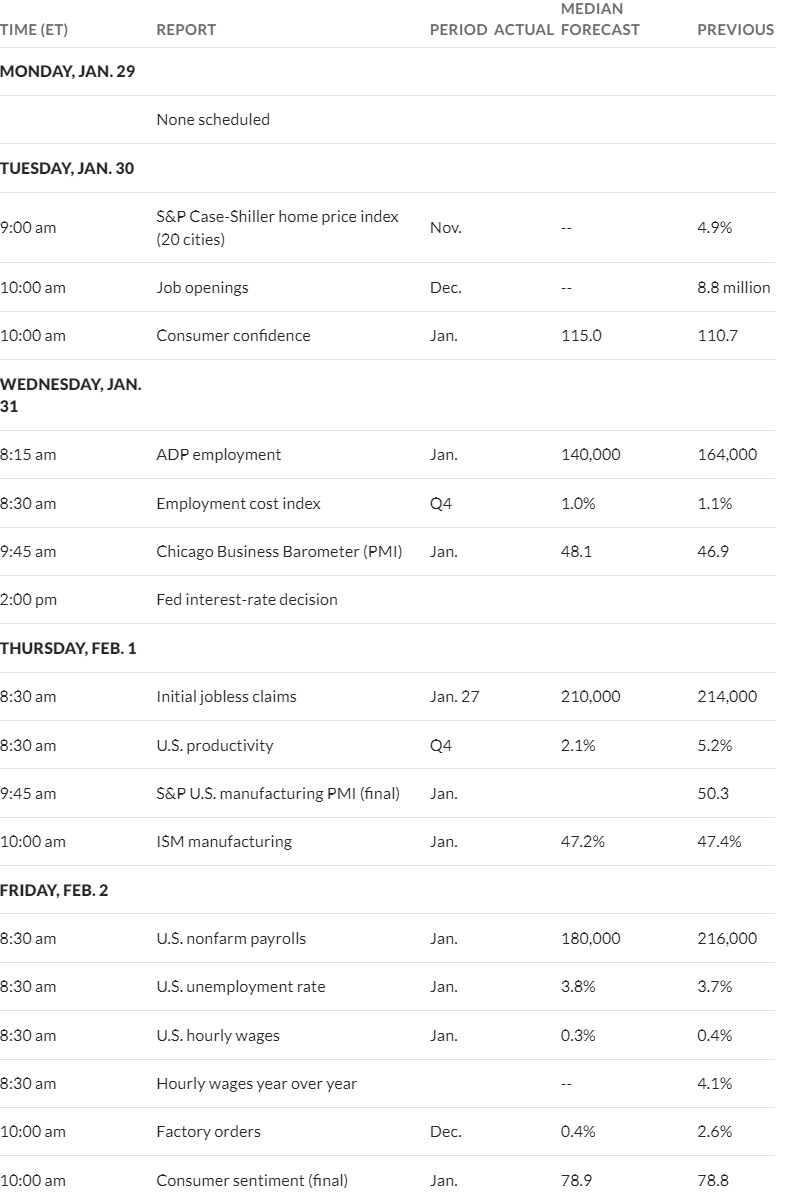

This week we have a FOMC meeting starting on Tuesday–ending Wednesday–virtually no one expects any FED action on interest rates from this meeting. The CME Fed Watch Tool is showing a 3.1% chance of a rate cut. We start off the week with no news scheduled for Monday.

The Federal Reserve balance sheet moved $4 billion higher last week. Overall the balance sheet has barely moved since 1/3/2024–down just $4 billion since that time. It is rare that we would go a whole month with no movement lower–have they changed the balance sheet run-off goal? Not that I know of–still at a total of $95 billion per month.

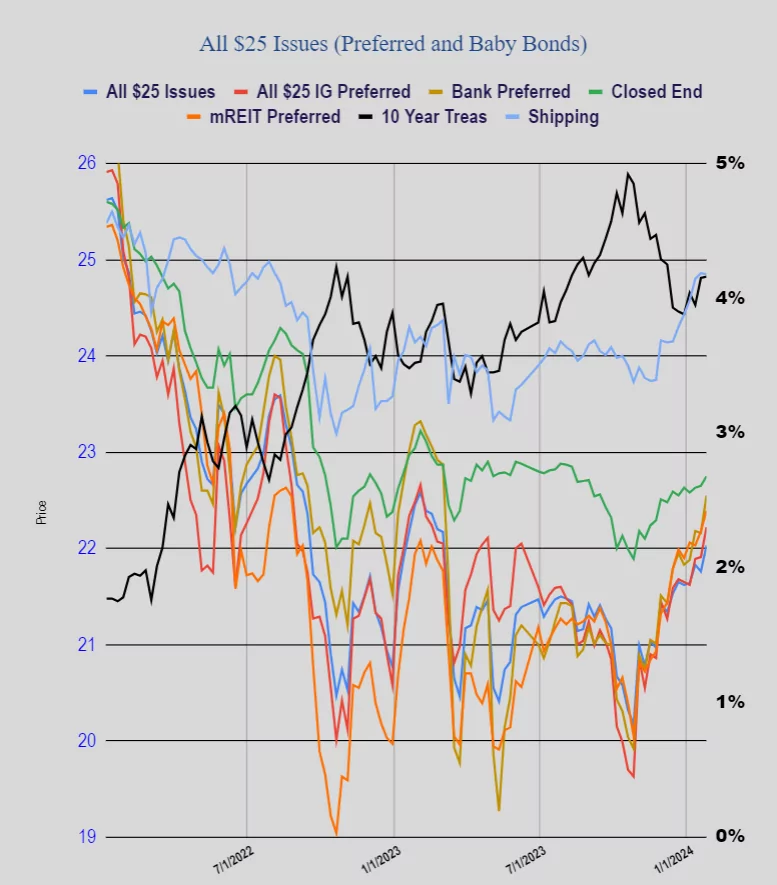

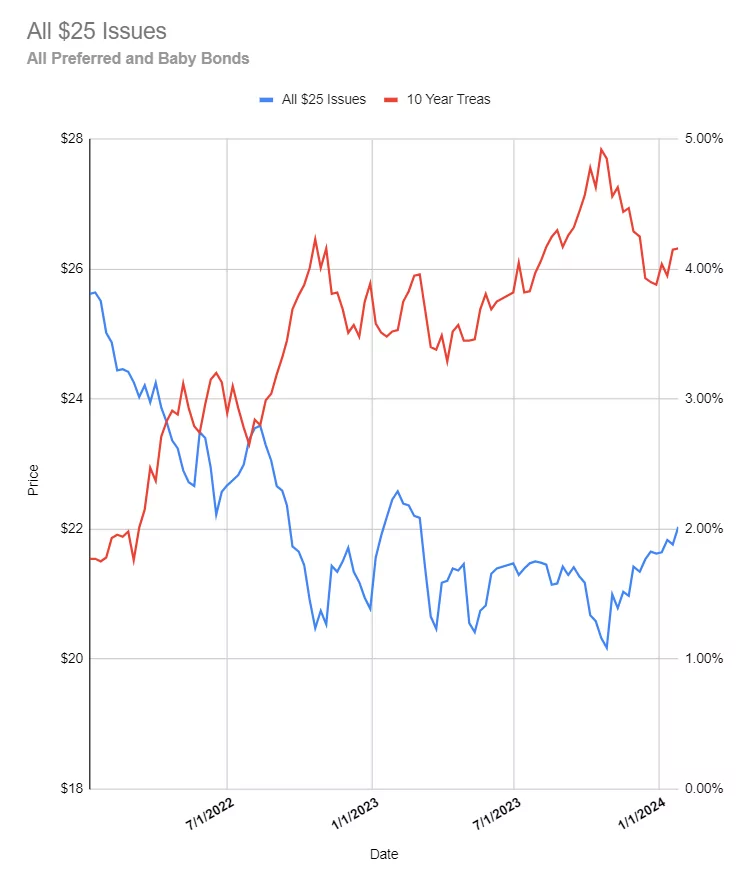

The average $25/share preferred and baby bond moved higher last week by 27 cents—all things considered a fairly stellar week. The average share hit $22.03 which is the first time we have moved above $22 since 3/3/2023. Investment grade issues moved 31 cents higher, bankers moved 39 cents higher while CEF preferred moved just 10 cents higher with mREIT preferreds moved 21 cents and shippers moved up just 1 cent.

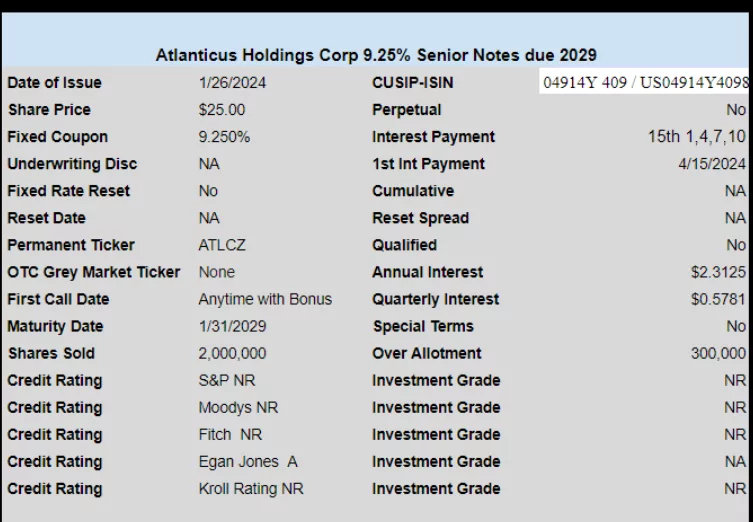

Last week we had 1 new income issue price as Atlanticus Holdings (ATLC) priced a new baby bond with a coupon of 9.25%. It will probably be a week before this one trades. Make sure to do your due diligence before chasing this yield–their write offs are generally pretty hefty.

And WHAT A KICK OFF!!!

JXN A went to 27 on massive volume. Over 500K in a few minutes. Over 850K for the day. And speaking of rally….ZIONO which has been setting up well, traded over 27.67 …Some other issues really strong too. All I can figure is that an ETF or a money manager decided they needed coupon.

The message seems to be, if the float is happening this year there’s a chance they too might spike. 8% move in 2 weeks? Sell Mortimer!!

EZ$

If you Prefer, now see what you have done. I said I wasn’t going to sell in my accounts I bought just for the income and I was blissfully unaware of the action on JXN A Now you have me questioning that strategy considering my buy in was 25.10 but the question is what are you going to buy that gives you the same 8% and relative safety?

Hi Charles, well that’s often asked. Most bond sales are 2 step trades. I get out of one to get into another. However when the move is over 8%, versus waiting another 45 days to collect 2%…..i ask which would you prefer, 8 now or 2% later? You’ll most likely going get a chance to re acquire if you really like the name.

Take the canoli.

I’m buying for a hold. With the CEF leverage rule and strong covenants on these preferreds to allow (force) them to maintain the coverage ratio, I have no concerns with holding term preferred of a CEF, particularly with credit easing supposedly on the way. The common, on the other hand, is risky and probably not something most here would be comfortable holding.

Does anyone have an idea why ZIONO is pushed to arguably ridiculous values? It has been setting 52 week highs for the past week or so and is presently at 10%+ over par, despite being callable since March last year. Is it the juicy 10%+ coupon / 9%+ market yield? Today’s volume was almost double its average….

Their Q4 ’23 numbers were not bad though not stellar, so that can’t be it.

I placed a GTC sell order for $27.95 (avg purchase $24.18), hoping and expecting to buy them back shortly for a more reasonable price.

So which is the better underlying bank, ZION or CUBI? I’ve never really taken any time to make that direct comparison, but as a stock, CUBI has done far better than ZION in recent history. With that in mind, it’s tough not to compare ZIONO to CUBI-F because the terms are quite similar with ZIONO being SOFR + .26 + 4.24 and CUBI-F being SOFR + .26 + 4.76 and both are currently callable, only CUBI-F even has slightly better call protection than ZIONO since it’s only callable on a dividend payment date while ZIONO is callable at any time subject to 30 day notice (CUBI-F has 30 day notice also)… So if CUBI-F makes it to 2/15 without being called, it’s good to go until 6/15.

So does that mean that CUBI-F (and E) are the next to make it to the $27+ price range or has something like an auto-run preferred fund’s non-price sensitive need to own the ZION name taken ZIONO to an unsustainable price? Gosh I hope it’s the former but I suspect it’s the latter.. Poor old CUBI-F is at 25.28 last vs ZIONO’s 27.59 and CUBI-F even pays a little more than ZIONO.

Hey Tim,

I was just looking at some high-yield regionals that recently reported earnings and I noticed that the highest curret yielding prefs above 8% are – BANC-F (8.4%), FGBIP(8.4%), VLYPO (9.5% floater), ZIONL (9.18% floater), MBNKP (8.44% float ), FRMEP (8.41 yield), MBINM (8.07% floater), TFINP (8.05%). CUBI-F (10.415% – FLOATER), CUBI-E (10.659% – FLOATER).

I am looking at TFINP which is a small preferred of a regional Texas bank that besides its usual deposit/lending business is also invovled in factoring and payment. They are apparently buying discounted invoices from small trucking companies and also are doing somekind of an app that is trying to connect shippers, carriers and insurance brokers. Their dividend seems well covered (10x 12 months trailing) and also they seem to see real prospects with the payment and factoring segment. Why is their preferred yielding 8%? Is this a screaming buy or am I missing something?

+1 for “Screaming Buy”

As a pref/credit holder, I care most about their balance sheet. Their credit holdings are much much safer compared to most banks. The CEO went out of his way to highlight 13 bps of charge offs for Q4. Yes, only 13 bps.

And from a funding perspective, their deposits are relatively stable.

The common trades like a tech/ SAAS stock. lots of upside potential as they gain market share. This is a positive as it creates the ability to issue (high priced) stock if needed to support the pref.

Lastly, management is in the very credible category. Just less possibility for shenanigans, always a factor for prefs.

This TriumphPay is something that most analysts are inquiring about at every earnings call. They are apparently trying to be a middle man between shippers, carriers and brokers. Not your typical bank.

Just bought ECCF at $24.70

I was able to buy at Tastytrade and got in at 24.65 but neither Fidelity nor Schwab seems to have it trading yet. Got to grab these early while the underwriters are dumping shares.

Are you guys buying for a flip or a medium/long term hold? I do not have much confidence buying a lot of these recent preferred/BBs. I put a toe in on the IG rated ones but have been ignoring the rest for the most part.

ECC is a closed-end investment company.

ECCF is a term pref with 5 years duration.

It’s very safe in my opinion.

peppino – Although ECCF does have the standard 1940 Act protection language, “Under the 1940 Act, we may not (1) declare any dividend with respect to any preferred stock if, at the time of such declaration (and after giving effect thereto), our asset coverage with respect to any of our borrowings that are senior securities representing indebtedness (as determined in accordance with Section 18(h) under the 1940 Act), would be less than 200% or (2) declare any other distribution on the preferred stock or purchase or redeem preferred stock if at the time of the declaration or redemption (and after giving effect thereto), asset coverage with respect to such borrowings that are senior securities representing indebtedness would be less than 300%. …,” the Devil’s Advocate argument regarding its safeness should also take into consideration it’s Company Strategy: “The Company seeks to achieve our investment objectives by investing primarily in equity and junior debt tranches of collateralized loan obligations (CLOs). The CLO securities invested in are unrated or rated below investment grade and are considered speculative with respect to timely payment of interest and repayment of principal. Below investment grade securities are also sometimes referred to as junk securities.” Put these both together and IMHO, only in Rida’s world should ECCF be defined as “very safe.” It is, afterall, a preferred, not a note, of a CLO investor, which, IMHO, takes a big chunk out of a safeness definition right off the top…. But I guess that’s what makes markets.

I’m pretty sure ECC will still be here and alive in 5 years.

That’s why it’s “very safe” for me.

I usually buy much more risky prefs and BB.