Last week the S&P500 moved lower by a hefty 2.6% as market participants began to realize that the Fed would be moving interest rates ‘higher for longer’.

The 10 year treasury yield moved higher by 12 basis points to 3.95%, but the yield was knocking on the door of 4% as it hit 3.98% a couple of the days last week. Most economic data is coming in ‘hotter’ than expected and inflation was shown to heat up during January as shown by the personal consumption expenditures index (PCE)

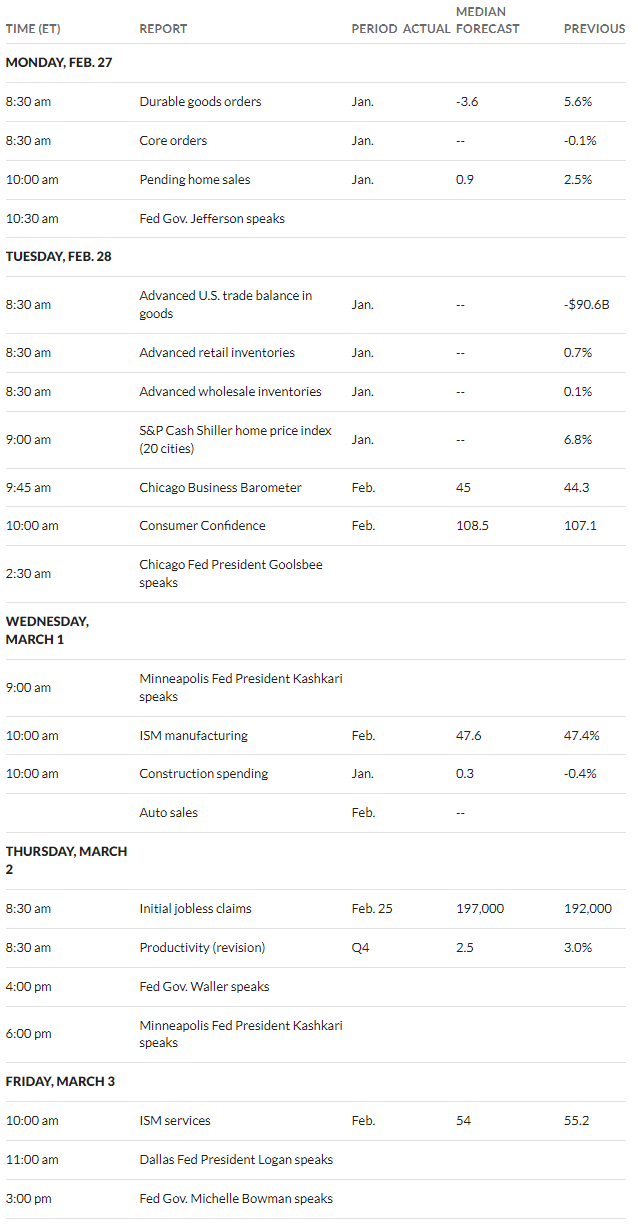

This week we have have plenty of economic data being released, but we do not have inflation and employment data being released this week which are key items that markets and the Fed focus on. As usual we have plenty of Fed yakkers sharing their ‘wisdom’.

The Federal Reserve balance sheet showed that assets fell by a measly $2.5 billion.

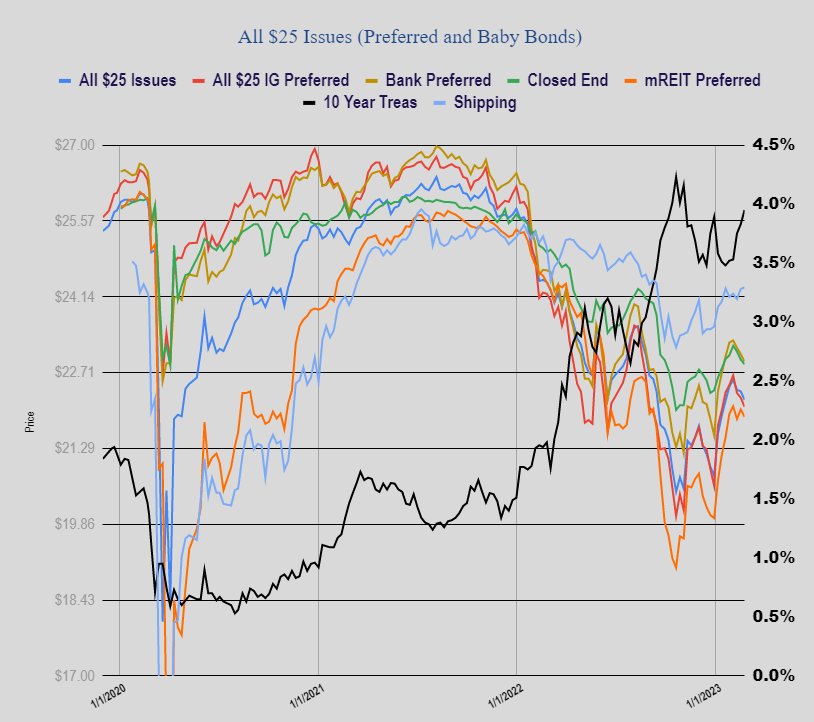

The average $25/share preferred stock or baby bond fell in price by 16 cents. Investment grade issues moved lower by 17 cents, banks lower by 14 cents, mREIT issues fell 14 cents. The only sector blipping higher was shipping which moved up 3 cents.

Last week we had no new income issues priced.