A big down week again last week for the S&P500 as the index fell by 4.8% to close at 3873. The market just has been too optimistic on inflation.

Interest rates again jumped and closed up by 13 basis points for the second week in a row and now is at 3.45%. Rates are again higher this morning by about 5 basis point to 3.50%. Of course we are starring at a 75 basis point Fed Funds increase of Wednesday which comes with a press conference by the Fed chair after the rate hike announcement which I expect to set a hawkish tone as the Fed chair needs to send a message that they are data dependent and the data thus far remains hot (inflation and employment in particular).

The Federal Reserve balance sheet rose by $10 billion last week as full blown quantitative tightening gets underway at the rate of $95 billion/month.

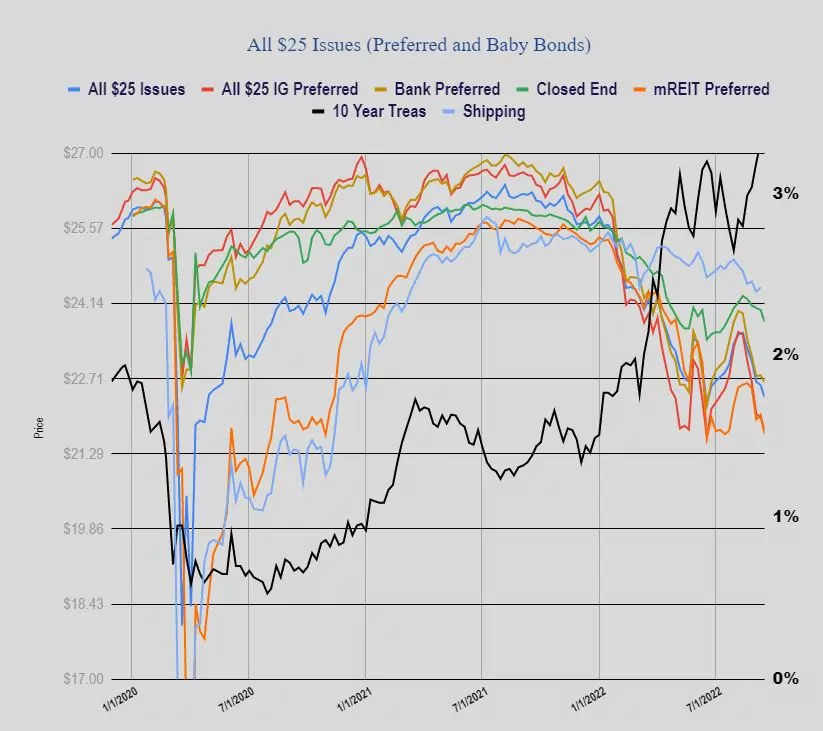

Once again the average $25/share preferred stock and baby bonds fell in price ending the week down 23 cents to $22.36–the lowest close since $22.22 on 6/17/2022. Investment grade issues fell 22 cents, banks by 13 cents and mREIT preferreds fell by 37 cents. BDC baby bonds fell by 16 cents.

Last week we had no new income issues priced–seldom do new issues get sold during times of market turbulence.

Tim, Is the Fed increase already baked into the CD rates we see, or will CD yields go higher?

Newman–likely the current 75 basis point move is substantially priced in, but we will likely see rates higher over the course of the next 6 months. Just depends on the Fed–they will move higher with the Fed, but banks will drag their feet as long as possible–they charge you more quickly but drag their feet when paying out. Some folks are predicting as high as 4.5 or 5 in the next year.

Tim, we had RGA priced new notes

Greetings

Hi Eugene–just saw that. Thanks