Another wide range of trading in the S&P500 last week –a low of 4162 and a high of 4465 with a close on Friday around 4463 which is 6% above the close of the previous Friday.

The 10 year treasury was up about 15 basis points on the week, closing at 2.14%, although during the course of the week we saw a high yield of about 2.25%. Of course we had an increase in the Fed Funds rate by 1/4% and we will likely see another at the next meeting which is in early May. My expectations for the 10 year treasury is we will see some slight creeps up and down unless tne news of of Ukraine worsens in which case rates will fall.

The Federal Reserve balance sheet rose by $44 billion last week to the highest level ever–$8.95 trillion.

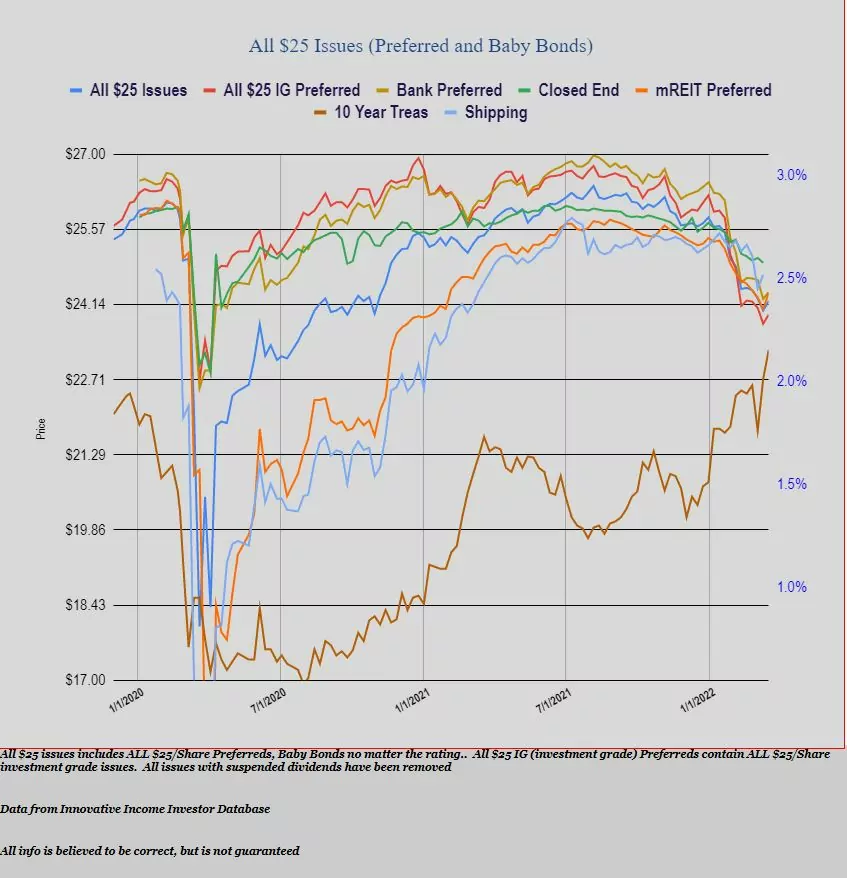

Last week the average $25/share baby bond and preferred stock closed with a gain of 18 cents as losses early in the week were erased with nice rally’s later in the week. Investment grade issues rose 17 cents, banking issues rose 13 cents and mREIT preferreds were up a strong 30 cents.

Once again last week we had no $25 preferreds or baby bonds priced. As interest rates stabilize in this area (2.15% to 2.30%) we likely will see a few company’s come to market with new issues.

Why do I get the feeling the only companies who will issue new preferred/BBs will not be highly desirable companies? It seems the “good” companies had people in place who knew this was coming and grabbed the cash before it was too late. In other people’s experience is this the case in a rising rate environment? It might take many months or even a year plus for IG new issues to appear?

The last two issues did not interest me at all.

If it takes long for new IG issues to come to market, the current deeply sold off IG issues such as WFC-D and JPM-D will finally stop going lower and potentially recover a bit as there are many holders that need to hold a certain % of IG issues.

Also, the bigger reason for current sell off may also be speculations on when the Fed will start their taper and start getting rid of the $4T in bonds it holds