After a rough start to last week with the S&P500 down near 2% the index ended the week off by just 1/10%. A stellar performance as talks of capital gains tax hikes put a very temporary fear into the market. Of course all downside moves are bought as investors have endless amounts of investable cash–or so it seems.

The 10 year treasury yield continued to slowly drift lower in spite of what seems like endless anecdotal stories of inflation flaring totally out of control. The yield started the week at 1.60% and slowly drifted to 1.57% over the course of the week. I suspect rates will continue in the 1.50% to 1.60% ‘goldilocks’ area until investors come to a conclusion that the inflation is something other than ‘transitory’.

The Fed balance sheet grew by $27 billion last week. That makes for an expansion of $130 billion or so in the month of April.

The average $25 preferred stock and baby bond rose by 3 cents/share last week. Investment grade issues were flat, banks rose by 2 cents, CEF preferreds by 4 cents. Overall a very quiet week.

There were 2 new income issues priced last week.

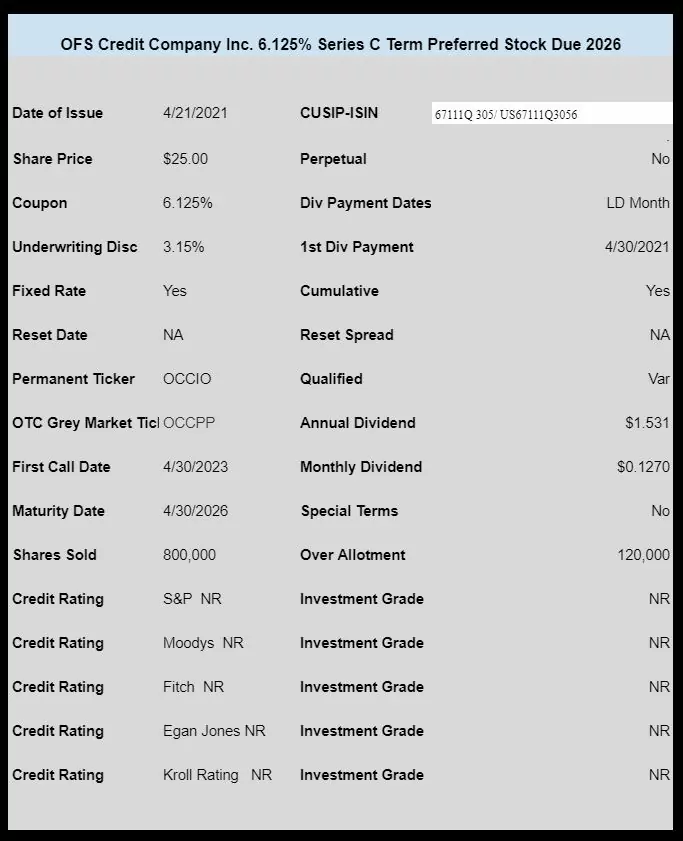

Little finance company OFS Credit Company (OCCI) priced a new ‘term preferred’ with a coupon of 6.125%. The quality of the issuer, in general, is not deserving of this modest coupon, BUT the mandatory redemption date in 2026 helped keep the coupon low. There is always a relationship between firm redemption dates and the coupon an issue prices at. In this case if the company would have gone with a 2028 – 2030 mandatory redemption they would have priced at maybe 6.625% to 6.75%.

This issue is currently trading under temporary ticker symbol OCCPP and closed last Friday at $25.

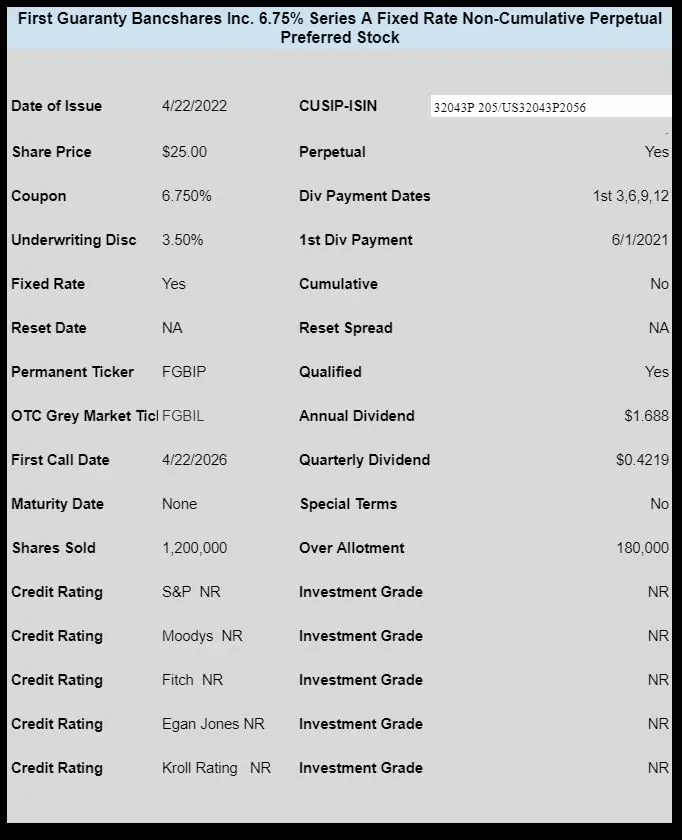

Tiny Louisiana banker First Guaranty Bancshares (FGBI) priced a new issue of perpetual preferred stock with a coupon of 6.75%. In what has become fairly commonplace in the last year the new issues of these small bankers have found solid demand in the markets. This new issue closed the week at $26.32 after trading as high as $26.65

New deal coming today

I read thru their entire 150 page annual report over the weekend. I know everybody seems to love it but I’m still not jumping in on it. Their net income over the last 3 years is $20 million, $14 million, & $14 million. Everyone looks at things differently and I noticed some of the snarky comments from the same old tired folks again. Hard to get excited about posting here anymore.

Im holding back myself trading at 26.30 nope. Its not for me I will wait myself.

Chuck, I have enjoyed your posts this past year. I know a while back you took some time off and I at least missed some of your input. You might of been early on your interest, but your call on hotel properties was good.

As Tim’s site gets more popular and we see new posts maybe from people who have drifted over from SA, I hope they keep it civil.

First Guaranty preferred issue is a reminder on how profitable the banking industry is if they pay nothing for their deposits, originate loans but don’t hold the loans in their loan portfolio, minimize labor costs through technology, increase bank fees, and invest their money wisely. The large banks are making substantial fees from investment banking. God Bless Jerome Powell for enabling banks to pay nothing on deposits by flooding the marketplace with huge sums of cash. I just hope for us investors the banks will bring more preferred issues to the market and pay us at least six percent like Merchant Bank, First Guaranty, Ocean First, Heartland Financial, etc in the last 12 months. Hopefully, some banks need some capital from preferred stocks to buy other small banks deposit base and start paying those savers zero ,increase their bank charges, and consolidate their workforce by saving labor costs, after a merger. Paying investors six percent or more for capital to expand by merger is a good solid investment in a economy where Main Street is in serious trouble.

Don’t forget the PPP program. That has been a money maker for the banks. We get paid to hand out free money

Don’t mention that program or I will have to go ballistic (just kidding). If you go to pro publica you can see every person/company etc that received money. When I look around my little community it drives me crazy to see folks that got money.

https://projects.propublica.org/coronavirus/bailouts/

Thanks for the link, Tim. Amazing.

What is your problem, Tim? You get up early each day, work had, apply yourself, thinking it’s for the benefit of you and your family? No, it was for someone else and someone else’s family. You just need to change your thinking to conform to the new policy reality. Helicopter money is here!

One bank is buying-

https://seekingalpha.com/news/3685549-new-york-community-bancorp-shares-jump-after-q1-beat-flagstar-deal?mail_subject=nycb-new-york-community-bancorp-shares-jump-after-q1-beat-flagstar-deal&utm_campaign=rta-stock-news&utm_content=link-3&utm_medium=email&utm_source=seeking_alpha

Nycb A has behaved well. Many investors have sold out of their preferred… I think I’ve moved everybody.

The Q is bank common shares in General. Many have rolled out of pfds into bank common and have been richly rewarded. But what about from here? I’ve heard both sides. One manager was dissing the idea. They felt bank common had little left to run. And would you seriously roll from growth side names to value side…where was the growth anyway. In a Zoom like name or a mid cap bank at a multi year high??