With hot inflation and the fear of ever higher interest rates the investment grade low coupon banking issues have been really pummeled–those with coupons in the 4.0% to 4.50% area. There is a fair chance that being ‘perpetual’ these issues may truly be outstanding forever.

Now personally I love these issues–just not at present prices. It seems reasonable to believe that even at what are now heavily discounted price levels they may have much further to fall.

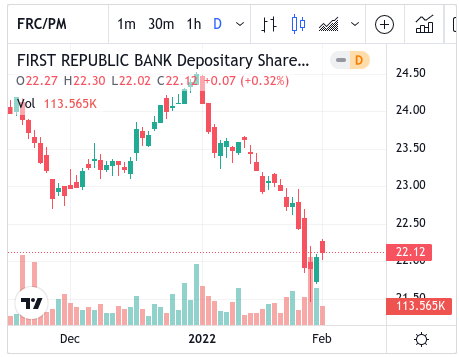

Let’s look at one of the issues that has taken one of the largest drubbings–the First Republic Bank 4.00% non cumulative preferred – FRC-M. This issue was sold in July, 2021 and while it traded around $25 for a short time in August it has not traded at that level since and has sunk to as low as $21.46/share lately–recently bouncing to $22.20.

Now we can clearly see what has been known for a long time–when rates are moving higher–or there is an anticipation of rates moving higher the lower coupon issues (which of course are almost always high quality issues) will bear the brunt of the share price erosion.

The ‘immediate income‘ investor may not care one whit if the share price erodes as long as him/her can feel safe in the receipt of a modest coupon payment. If this is the case this same investor should consider adding to their position –what was a good investment at $25 is quite the bargain at $22 or $21.

On the other hand one should deploy cash very carefully–what is $21 or $22 today may well be $18 before the year is out–in fact if interest rate forecasts hold true these issues will almost certainly be much lower a year from now. Only time will tell

Bought some of the JPM/K at 24.15 May end up holding it forever but I’m good with that.

I’m on hold and making a shopping list.

The JPM, USB and ENO type of issues will be at the top of my list.

As of now 4.5% does look to be the handle of the preferred issues.

IMO, by the fall we should have a better sense of what is going on and a good view of options. Lots of sock drawer issues to build an annuity type of portfolio.

Who knows, ALP-Q may be our new IPLDP. That would be nice.

Just to give you an idea of the happenings still going on in the “Bond World” Valero Energy a very old company that is in a very out of favor industry just this morning came out with a BBB 30 Year bond with a Coupon of 4.45%. My point being with inflation now raging in all kinds of things well over the 7% that the Talking Heads on CNBC are spewing who in their right mind would buy this??? And to Tims comments above I said pretty much the same thing about 6 months ago that I want nothing to do with low coupon preferreds in this “environment” unless you like getting your head handed to you as it goes south.

keep adding

I still get the feeling we will not have many high quality businesses rushing out to issue new BBs/preferred at 5.5% anytime soon if rates keep going up. If FRC-M trades at 18 that is essentially 5.5% so there will have to be some pretty exciting things to purchase at 25 for that to happen. That recent BAC preferred at 4.75% probably represents as good as it will get for the time being for something comparable.

I guess the only other option is to sit on cash and miss out on 4-6% over the next 12 months with no risk of capital loss. Praying? that a BBB- company comes along and wants to borrow money at 5.5% when it had a chance to borrow significantly cheaper for a while now. Why would they at this early stage? Early being 1-12 months since the Fed decided to fight inflation by being more hawkish.

I think there’s a better option than sitting in cash for a year waiting for the preferred market to settle. I’ve been stashing cash earmarked for fixed income investment in a floating rate fund ( FFRHX in my case but I’m sure there are others) to be deployed later this year or next into better priced fixed income bargains. At slightly over 3% and some capital upside it seems to me better than waiting in cash. Thoughts?

JV,

FFRHX can also drop significantly, see e.g. what happened on March 2020: it went down to almost $7.50 and took many months to come back somewhat. And the drop was very sudden. Even after the scare, it stayed well below $9 for a while. So the money there may not be as readily available if you need it after it drops 10 or 20%.

Having stated this, I also think this can be at some point an option for (some) of my cash, especially if it begins to yield higher, but probably not quite now.

Curious about others’ thoughts

dd,

March of 2020 was a black swan and meant that interest rates, if changed at all, would be coming down to prop up the economy during the emerging pandemic. That wasn’t a time to be going into floating rates so FFRHX’s bad performance was understandable. But I think things are different now with a growing economy and inflation the fed says it will battle. In other words: that was then, this is now. One drawback is Fidelity gets upset if one uses FFRHX as a ready cash fund. They want a 30 day holding period. Other thoughts invited.

Vinny, agree with every thing you said. Just takes a lot more than 3.23% yield of any duration with a Credit Rating of “B” to get me interested if, at all.

The whole point of floating rate notes is to minimize interest rate risk (i.e., bond price is relatively stable regardless of rate changes), so the idea that FFHRX dropped in March 2020 due to declining interest rates is inaccurate. And that’s obvious because the price recovered even though interest rates remained low. FFHRX has credit risk and it gets hammered when credit spreads rise – has happened every time in the past and will happen every time in the future.

It’s not just about rates. BBB spreads are up 25 bps since October with most of that increase coming since Jan 1. 25 bps spread increase plus 25 bps 10 year UST increase should mean a BBB bank preferred needs to yield 50 bps more than a couple months ago. So 4% preferreds need to be priced to yield 4.5%.

good analysis Landlord and FC, I pulled the trigger last Thursday on ‘jpm-k” for a yield of 4.73% , and I’ll double down with Jamie Diamond if this goes down latter this year to $18.00 like “Tim” suggested.

I too decided to ride the Dimon train with a small position in JPM-PL @ 23.90

If you guys are comfortable with higher quality lower yielders, you may want to consider CBKPP, which is a stronger credit bank than even JPM. The fast approaching floating mechanism in October (if not redeemed) converts it to 3 month Libor plus a strong 4.556% adjustment. If short term rates rise this will pay more all while being one of the safest banks in the world. Many brokerages wont allow purchase though it appears. I bought through TD at $102.65.

Thanks for the earlier heads up Grid. I did pick up some CBKPP. It has a decent yield to call at that price and I could only buy it in my TD account.

Kapil, Im beginning to think most of the retail brokerages wont allow a purchase of it. I would strongly suspect this will go to float status. You seen how they dragged out the 6.125% fixed CRLKP that was just recently redeemed…three years past call. They presently have 5 preferreds with only the very overpriced CKNQP publicly tradeable besides this one.

Thanks Grid was able to buy 200@102.66 with Chase self-directed. Tried Merrill first no go.

qxjm, are you able to put orders in on any expert market issues with Chase by chance?

Just for giggles I entered SLMNP at 800 and KTBA at 20 and both worked except for there is a warning. Review all warnings

Please be aware this OTC security purchase may require additional approval to sell if traded below $5 per share. Please contact us if you have any questions. (R01946A)

I also was able to buy OCESP ocean spray whaen it was trading at 14 on Sept 21st 2021

Nice, Im jealous!