Yesterday we got exactly what we expected from the FOMC–nothing–no change. What wasn’t expected was statements from the Fed chair that we may not see cuts in March–a meeting that is 47 days away–a strange comment from someone who is ‘data dependent’. No need to have markets panic–reprice equities for a few days and then move forward. The fall in equities was minor yesterday–down 1.6% on the S&P500 is meaningful, but considering the never ending rise in the last few months–not such a big deal.

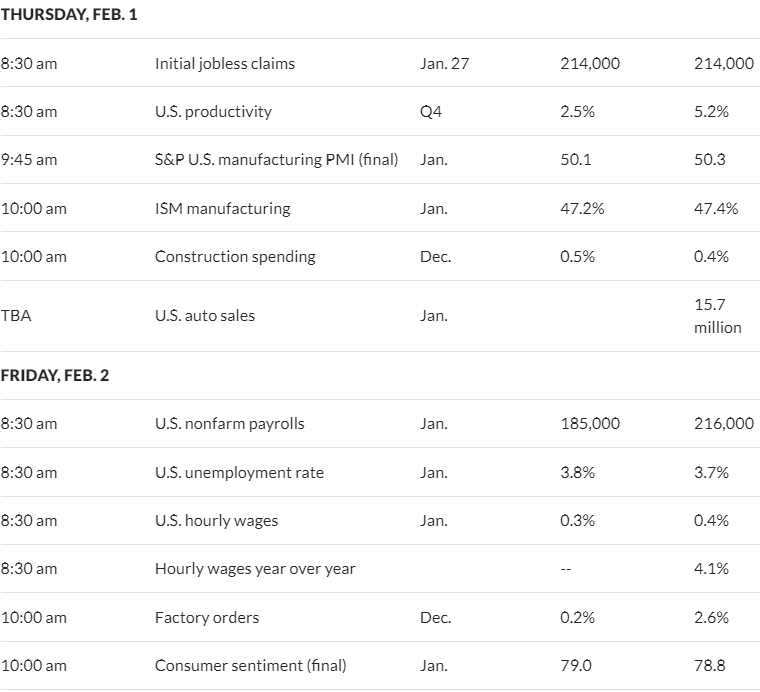

Interest rates are trading flattish to down this morning after falling yesterday by 9 basis points. The 10 year is trading at 3.94%–and was as high as 4.12% earlier in the week. With bunches of economic news out in the next 25 hours we could see substantial movement in interest rates–in particular employment news.

Preferreds and baby bonds generally held up well in the common share downdraft yesterday–of course with interest rates dropping there was a push and pull on pricing and ending flattish. Honestly, anecdotally, there has been super demand for preferreds and baby bonds–lots of folks trying to ‘get on board’ with the belief that interest rates are heading down.

Today I may do another nibble buy–we will see–if I do of course I will post it. Looking to add to a current position–I have a couple in mind, but have not determined which will be bought.

From WolfStreet:

Here’s my Powell Cocktail, Not Quite in his Own Words

https://wolfstreet.com/2024/01/31/heres-my-powell-cocktail-not-quite-in-his-own-words/

Tim

What I heard Powell say was that to lower rates, the Fed doesn’t need any more improvement in inflation or any weakening in employment or growth; the Fed just needs more of the same data as the last six months. So the Fed now has a third priority besides employment and inflation: to lower rates. (Note that the productivity numbers this morning help the inflation numbers.) Question: if raising rates doesn’t materially slow growth or increase unemployment, will lowering rates increase growth or lower unemployment?

It’s another case of….. the Fed fighting the Fed.

I kept telling others we need to have coin if rates rise. Rates drop, great. Rates go up, watch out.

Oh and for NYCB…. it’s net worth to total assets are now indicitive of a bank that could be closed at any time.

What evidence is that statement based on? Is that just a rumor or do you have some napkin math to back it up? Their loans are more diversified then before. Non performing loans improved very slightly. Am I missing something except if all their office properties fall to zero value or something?

preferreds of regional banks are dropping in reaction to the NYCB news.

Agreed with others. I personally think the elite conversation on the policy side has come to recognize that ZIRP was too low and too long. I think Powell was trying to normalize in 2018-19 before COVID-19 but hamstrung by politics and Wall Street. I think inflation has given the Fed cover to normalize so that we are not headed back to ZIRP barring a catastrophe. “Higher longer” is the rational bet, and moderate rates will prove better for capitalism over time.

Totally agree! Days of Lowflation are over.

I heard powell say that the FRB wants to see more good data (inflation) before cutting rates.

I dont think they believe that inflation will glide down to 2% and stay there. It is clear that they are committed to 2% and a sustainable 2%. That takes more good data.

Cheers! WIndy

+1. Sick of the war on savers over the last 10-15 years. Need more balance between savers and spenders.

I don’t think rate cuts are coming anywhere near as soon as popular wisdom. Like not even close. It’s highly unusual to be cutting rates when the stock market is at new highs and the economy is doing so well. They really risk inflating a bubble.

I tried to get some NYCB.PRA yesterday but didn’t get a fill. Close but no cigar.

Jay may see something in HIS data that is not as rosy. Plus, the economy has still been rather hot in spite of the current Fed Funds rate. I think he’s just telegraphing a higher-for-longer stance that the markets don’t want to believe. I’m cool with that as long as we don’t see a raging recession – we might need a mild one to suck some of the leftover COVID liquidity out of the system. 4% 10Y is fine by me.

I remember my dad helping me open my first savings account at Maryland National Bank back in the early 70s – a 5% Passbook savings account. The bank and the passbook concept are gone but, 5% savings seemed to be the norm back then. Meanwhile, I purchased a JPM 5.2% CD this morning with some of the money that matured from a Treasury overnight.

Why not yazzer? Why do borrowers always get the benefit? As you reference these arent really high historical rates at all. Why cant savers and conservative investors get a piece of the pie that has historically been given to them. Its fine by me just where its at. If you borrow money learn to sharpen the pencil and see if the math works before you do!

yup – my thoughts exactly, Grid!

Grid, I wish there was a “Really Like” button for this one. Savers been gettin’ shafted fuh too long!