This morning we had a number of economic releases–and once again they remain a mixed bag of good and bad.

1st time unemployment claims remain muted at 222,000 versus 226,000 (revised) last week. This number must INCREASE to have some certainly that we will have a reduced 50 basis point rate hike by the Fed–employment is a key number for them. Continuing claims continue to creep slightly higher week by week.

On the other hand the Philly Fed Manufacturing index cratered badly at a -19 versus a forecast of -6 and versus last month at -8.7.

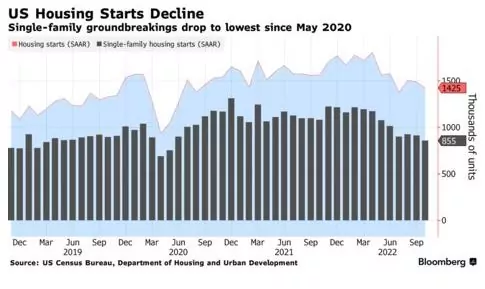

Housing starts continue to weaken–although they are not ‘plunging’–more of a slow drift lower. Single family starts are at the lowest since May, 2020.

None of the seemingly modestly soft economic news is feeding into employment as of yet–but there is a likely lag there. Or with the 10.7 million jobs openings folks are just moving elsewhere quickly (honestly I doubt this).

The Covid stock market crash back in early 2020 happened very quickly and the markets’ recoveries were also quick. This time the slump has been more gradual over an extended period of time. It’s like a slow death from a thousand cuts. My intuition, not always right of course (:-), is that the economy will take a long time to recover—maybe 2 or 3 years.

Assuming that happens, where will interest rates be during this time frame? My thinking is that I want to be about 75-80% invested in preferred stocks/baby bonds because I don’t think rates will go a lot higher from here. If they do, I will use my cash to take advantage of IG securities that I can hold forever.

I also want (with a small amount of money) to buy some of the high quality growth stocks that have moved a lot lower. I don’t know whether to wait for a final blowoff or start buying now. I’m talking about GOOGL, META, MSFT, NVDA, V, MA, etc. I guess I’m hesitant because I’m very old and don’t want to sit for a long time with great stocks that pay no dividends. Decisions, decisions, decisions……………..

Actually, I have to ask myself what do I actually need. Google? Facebook? Not so much. Hydrocarbons? Well, yes, I believe so. I don’t want to freeze to death in the dark. Winter Storm Uri is still in my frontal lobe. To be old and without power for a day or more certainly helps to focus the mind. So, yes. I know what I can live without. Hydrocarbons ain’t one of them. Everything else is dancing on the head of a pin. Folderol, to put it mildly.

JMO

Just my unintelligible, non-fact-based thoughts, but it’s hard to have high unemployment when the cost of living requires many to work two jobs. I used to take a month or two off every year on near minimum wage pay, heck, didn’t even work full-time all year. Doubt your average 20/30 yr old person could get away with that these days. Granted, I’m fairly frugal and content with the outdoors and hiking.

Speaking of fact-free thought, with all waves of dislocation in the labor market set off by the pandemic, I don’t see how the Fed can use the unemployment figures as a basis for policy decisions. It seems we have a bunch of PhD spreadsheet jockeys making assumptions about the quality of data underlying their statistics, either unaware or quietly ignoring the fact that the numbers just don’t work the way they used to. (Kind of like the rocket scientists at the agencies rating AAA mortgage securities back in 2008.) My observations align with yours, Smitty. All our employees who sign annual leases for housing are getting absolutely wiped out by the rent increases. More than a few are choosing between a taking second job and going to the food bank during the last week of the month.