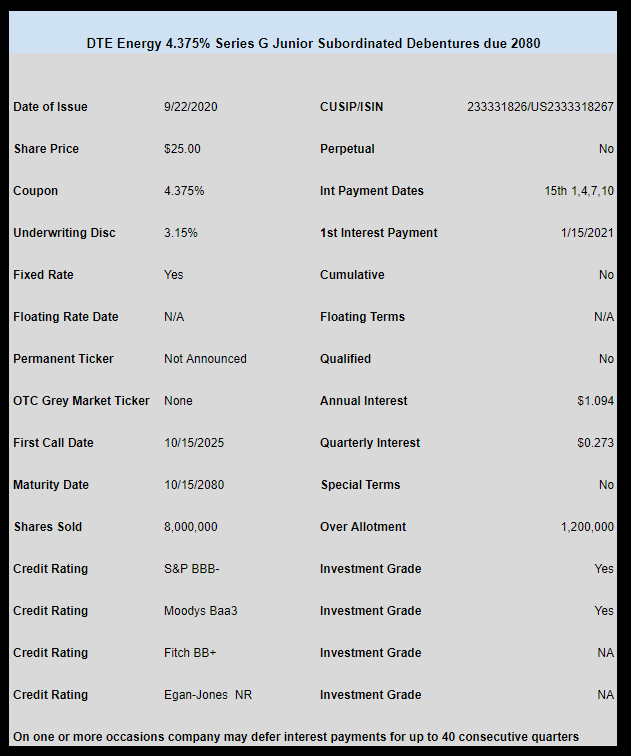

DTE Energy (DTE) has priced the previously announced baby bonds.

The Junior Subordinated Debentures are priced at 4.375%–right where razorbackea said they would price.

The company can defer interest payments up to 40 consecutive quarters (10 years) without being in default.

No ticker has been announced. It is likely this issue will start trading next week.

The pricing term sheet can be read here.

Does anyone know the ticker symbol for this one?

Dick,

I have not found a ticker symbol for this one yet. Per SEC filings listed on the DTE website, their registration statement for listing has been approved per a letter dated 10-2-20, but I cant’t see it’s trading yet.

Maybe later today or early next week?

symbol is DTB it will list on oct 7

Thank you mcg

Thank you mcg! I really appreciate your posts!

mcg,

You were absolutely correct.

DTB is trading today (10-7-20) on NYSE.

I got some shares in this issue @ IPO, but wanted more. I saw activity in the bond market via the gray market last week, so I ventured into that arena yesterday. Was able to build what for me is a good position. The settlement date on the IPO is tomorrow. Don’t know if it will make it to the NYSE b4 the end of this week. Hope it gets there at least sometime next week. At this juncture I’ve only seen new preferred type issues from utilities by Southern and DTE. Others are exiting that type of security – see NextEra. So the choices are getting slimmer in utilities at this time. Did see that DTE is floating a new institutional senior note today. Have no idea what the coupon will be.

Correction – settlement date for DTE 4.375 IPO is Wednesday, 10-1-20.

My bad

My bad #2

Make that Thursday 10-1-20

Thanks rb

You are welcome Tim.

I just noticed that the new institutional senior note that DTE is issuing has a .55% coupon and is priced at a slight discount to par to provide a YTM of .575%. It’s based on .45% over the treasury note maturing in Sept 2022. The DTE note matures in 2 years also.

What not to like here? Low yield, barely Investment Grade, Subordinated Debt with a 2080 Maturity Date (probably won’t be around to see that). However, I am guessing this issue will quickly trade over $25 within a few days of being available. Sad.

Yes, I dont even know why a smaller investor would look at this even if wanting utility yield. One can get that yield in QDI ute preferreds with as good or better credit rating than this.

Guys to put it in prospective, this is the perfect example of the basic death of QDI preferreds at the holding company level anyways. See with the low yield and deferrable subordinate note status, this is for all intents a preferred…Except the company via the tax deduction receives the “QDI” and the buyer gets squat. The only real way you will see a new QDI Ute preferred is if regulators want at subsidiary level more equity ownership in the company to beef up the ratios. And if hold co doesnt want to inject it, they could issue some subsidiary preferreds to accomplish it. Otherwise this is a prime example of they are dead. This issue is equivalent to them sending out in many states a 3.19% perpetual preferred. And the market isnt ready for that, yet.

Grid,

QDI in taxation was developed in the GWB administration. So it’s been with us for between 15 and 20 years. I can’t put my finger on the invention of $25 par value preferreds, but I’ll guess it was early to mid 1990s. So I’m going to say that b4 those events the only tax advantaged preferreds were those held by corporate investors (C corporation) who enjoyed the DRD. The DRD years ago was either 70 percent or 90 percent (can’t remember which) and the corporate tax rate was 46 percent. So a C corp owning preferreds paying a 2 or 3 or 4 percent coupon had a heckuva deal. I figure a lot of preferreds b4 the 1990s were owned by such C corp investors. There was no tax advantage for individuals to own preferreds (QDI) b4 the Bush Jr. administration.

Agree that from a regulatory and ratings perspective subordinated debt is now the equivalent of what a preferred once was considered. But as far as individuals are concerned in the utility sector there never have been a lot of QDI $25 par preferreds as I see it. Case in point this new DTE issue is a sub issue replacing DTQ which is another sub issue.

If you want QDI preferreds, the utility industry isn’t and hasn’t been where to find them.

That is correct. The history of QDI preferreds were best utilized tax wise by CCorps due to the onerous tax rates they used to pay way back in yesteryear. But no, they have been available to retail consumers for a long time though, via the $100 and $50 preferreds. Just as you stated fewer offerings though, and this did coincide with the advent of the holding company structure which has consolidated the utility industry over the past 20.-40 years. As the hold co redeemed the utility preferreds or bought most of the floats in tenders to keep voting control. Many of these, however,are still available mostly in roached out previously tendered offerings. Many utilities in the 1990s took advantage of high relative interest rates and offered well below par tenders which owners gladly accepted. The Indianapolis Power and NEWEN and NRGSP preferreds off the top of my immediate head are some as their still is a visual trading trail of these today.

If you go back and look at 1950s and 1960s preferred through Standard and Poors or regulatory lists, there were a entire literal slew of utility preferreds available. But also there were IBM, Texaco, and Exxon preferreds available. Water utilities even used them back in 1970s. Its a largely disappearing cap structure outside of Financials, Reits, and highly indebted companies.

But the few that offer have even less…Even if you look at Quantum you can see older issues all redeemed in past 10-20 years. Also in general many subsidiary preferreds have been redeemed in last 10 years. Even 3.5% to 4.5% perpetuals. Plus the few that did are largely retreating. Look at SCE…They just redeemed a slew of older issues trading well below par and lowered their cap structure to 5% preferreds from closer to 10%. Entergys in past 2-5 years has redeemed Mississippi Power (which did have a $25 issue), Entergy Arkansas, Entergy Gulf, EntergyLouisiana, Entergy Mississippi and replaced them all with debt offerings either at Baby bond, or Bond desk notes… Southern has redeemed all their Gulf Power, Georgia Power, Mississippi Power, some Alabama Power QDI preferreds in this past decade and replaced with baby bonds or just redeemed. These were a literal playground for me…Exelon redeeming the sweet 3 Baltimore Gas $100 par issues (Issued in 1990s) I loved to trade in. AES redeeming Daypo preferreds a few years back.. Trust me the list is long and and they were out there as I owned most of them at one time or another. 🙂 I would guess redemption reissue ratio is 20-1 call and no reissue of QDI, or a baby bond replaced instead.

But yes, in terms of percentage banks/financials have clearly been the heavy hitters they are roughly 75% of the preferred market.

Grid

I yearn for more real preferreds which would now be QDI from the utility industry. But for various reasons – regulatory and ratings as well as fund sources we just may not see that many, The sources of funds today from all kinds of retirement plans is unbelievable compared to what existed pre 1970s say.

I never had a company pension plan but utilized IRAs from 1974 (I think) when they were first invented (made part of the tax code). And I’ve done everything I could with ROTHS when I could qualify for one – well two counting my wife. You never know what the future holds you have to work with what’s available at any given time but I wish all of my IRAs were ROTHs.

But I’m rambling about retirement plans because the explosion of them makes moot to an extent whether a security is sub or a real preferred.

I’m sure Wall Street talks about fund sources with CFOs as well as perhaps

regulatory and ratings people and all of that may have contributed to getting us where we are.

In any event, I still like utilities a lot. After REITs they are my largest industry concentration. But I guess I’ll have to take what I can get even if that means exchange traded debt.

Razor, last I checked I was a little over half utes, I think SJIJ is only ute baby bond I own rest being QDI. Reits is second not because I own so many as much as that I own so much LXP-C, ha. Other whatevers are my third, and banks are my smallest. They are probably fine, but we all tend to gravitate towards what we trust. As that matters most when market panic hits. I have to have confidence in what I hold so I dont do something stupid, at the wrong time. 🙂

As far as retirement goes its certainly more stressful now than the good old days of 1/3 each of Ma Bell, Local ute, and CDs. Im very thankful for my pension. As long as it outlasts me it will more than cover up any or all investing mistakes I would make.. So I am much more interested in the returns of my pension manager than I am of my own stuff, ha!

QRTEP issued through a special dividend from QRTEA looks like a good investment at these prices – QRTEA paid 1.5 $ in cash and 3 shares of QRTEP for every 100 QRTEA held last week.

SG, I have been waiting for “the dump” and bought this morning a modest 200 shares at $93.70 this morning as a higher risk bucket issue. These Liberty issues are something else in their spinoffs and special divis, etc…GLIBP which I own (an uncallable preferred that matures 2039, that recently merged again yet with another entity and will have the preferred renamed under same terms) was originally joined with this QVC centered outfit.

These types of issuances have a stigma of being “dumped” on people. And then they jettison them for the cash. A plus 8% BB- type issue isnt the worst in the world. And the terms are nice…Mandatory 2031 maturity, 5 year call protection and a premium to be paid if called in years 6 and 7. Not a fan of what and how the company peddles its products but that is why I have this in the old high risk bucket.

I have no clue on when the sell pressure will end.

Man! One really has to get down in the dirt just to figure out GLIBP has a “Scheduled Redemption Date” of 2039! It’s sure not spelled out up front, is it.

2WR, When you deal with anything John Malone has his hands on its all gonna get goofy. Probably ways to maintain control and extract income at same time. Yes, it is a 21 year dated term preferred (does 21 years even count as a term preferred anyways?)…And now his latest thing is this very common 11 year mandatory maturity issuance… But clearly they arent too interested in redeeming it or they wouldnt have put a 6 and 7 year redemption premium on top…And not even needed since the shares were not IPOs, just like GLIBP which was not either.

I was a bit too itchy buying my 200 as the dump continues. Under $92 on over 400k shares. Its just always hard to know where the bottom is on these types of dump issues.

Grid – I didn’t realize you dabbled in C-corp preferreds like QRTEP with 8%+ yields. Next thing you know you might venture into some of the hotel REIT preferreds like those issued by RLJ, SHO, and PEB that are still paying and offer 7-9% yields! Just kidding.

Thanks for the idea on GLIBP. Very interesting, as GLIBA seems to be a rock solid company in a somewhat hot sector right now.

GLIBP is truly uncallable until 2039? Wow.

Rob, I designate a portion for higher risk. It isnt hospitality or mall, but close enough, ha.

What is now QRTEA and GLIBA actually used to be under one roof a few years ago..In fact if memory serves the genesis of GLIBP came from separating. If one likes credit ratings QRTEP is stronger than GLIBP. But several hundred basis points better yield. In fact GLIBP had the exact same sell off dump when it was issued a couple years ago also. Part of my thesis. And I just bought 100 more below $91. I swear 300 is it…Maybe, lol…

And I certainly view this snippet below as a positive for the high yield issue..

Fitch has also assigned a ‘BB-/RR6’ rating and 0% equity credit to Qurate’s proposed offering of approximately $1.3 billion aggregate liquidation preference of 8% fixed rate cumulative redeemable preferred shares. The 0% equity credit is driven primarily by restrictive interest deferral terms. The preferred share issuance is part of a special dividend the company will distribute, which will include $633 million in cash.

Trust me when I say that QVC has its share of core customers.

I have a relative that has trouble sleeping and often stays up until 4AM ordering junk from that company while watching their cable channel.

I’m fairly certain he is not alone. QVC is a shopaholic and insomniacs’ dream come true.

QVC just redeemed some 5.125% notes so is this the same company that Grid is talking about? It would be odd to redeem the 5.125% early and issue 8% ones. Must be some sort of holding company arrangement.

Scott, this explains it a bit…The 8% preferred was part of a “special dividend”.

This was a billion plus issuance and many are just dumping it for the immediate cash. Over a million shares today and half million yesterday. Probably more needs to be dumped and sopped up before it can stabilize.

https://seekingalpha.com/pr/17980146-qurate-retail-announces-declaration-of-special-dividend-of-cash-and-preferred-stock-to-common

https://www.fitchratings.com/research/corporate-finance/fitch-rates-qvc-issuance-bbb-rr1-qurate-preferred-shares-bb-rr6-affirms-idrs-at-bb-12-08-2020

FWIW, John Malone who helped create this is keeping his bloated supply indicated his intention of keeping the preferred that he received from this process.

John Malone and Greg Maffei, each a member of Qurate Retail’s board of directors, have indicated their intention to be long-term holders of the preferred, which will collectively represent approximately 8% of the Preferred Shares expected to be outstanding on the distribution date.

https://www.businesswire.com/news/home/20200821005410/en/Qurate-Retail-Announces-Declaration-of-Special-Dividend-of-Cash-and-Preferred-Stock-to-Common-Stock-Holders

Down to 89.8, that’s almost a 9% yield. How much more do I buy! 🙂

I haven’t researched much at all but is QVC a dying industry?

EOZ, I dont jump off the cliff with all my money, ha… I pretty much laid my bed at 300, now Im gonna lay in it, let it play out and not chase.

I know John Malone and partner own 8% of the over billion float, so that is a pretty penny, I know through Fitch it has no equity assigned to it from its restrictive covenants (Hmm, why would a preferred have restrictive covenents to protect owners…maybe because Malone owns a slug?), I know GLIBP has lower credit rating and considerably lower yield and it dropped just like this when it was dumped on market from owners…. And if the company doesnt go bankrupt in 11 years I should get my money back at $100…I hope. 🙂

Dick, they had a great quarter…The Corona stay in thing..The oldies keep buying I guess…

https://seekingalpha.com/news/3603681-qurate-retail-eps-beats-0_05-beats-on-revenue

Scott, yes you are correct QRTEA is the holding company.

I guess as long as they don’t stop making old ladies, or cure insomnia QVC will make money ;o) Seriously though, it is very rare that people can sleep through the night when they are older. It is normal that your sleep gets broken up into segments then.

I bought a bit under $91.

I think the QVC issue was trading 15% above par the last I checked so if this recovers to anywhere near that level, after all of the people who were shocked to find an alien issue that they don’t understand in their account dump it, then we will do well.

Scott, granted I wish this was an unwanted Ameren preferred being dumped, but that aint happening. But I would guess that vast majority of investors dont like or even want preferreds. Especially when they can just dump and take the cash instead. Selling creates selling and the issue isnt being promoted by an underwriter. So a billion dollar issue will have sell pressure until these shares are sopped up by people willing to hold it.

This process happens all the time. I just got a bit to trigger happy should have painted a little longer and I would have got them cheaper, ha!

Speaking of Ameren preferreds being dumped, did you pick up any AILLM today?

Dick to be honest I didnt notice until I read your post now…Been distracted most of the day doing touch up painting to all my living room, hallway, and stair walls from the damage the wood floor installers did. Scratches were everywhere. More repair needed on the wall trim too, ugh…

Anyhow, I already have AILLN, been rebuying AILLL recently in 28.75 range, and have UEPEM.. So I probably have my limits here for now anyways. I need to focus more on my high yield bucket and rejigger that a bit more somehow.

I bought some QRTEP this morning just above $90…it may have bottomed, but in this volatile market its hard to tell.

Me too, just a toehold, find myself (mostly) resisting temptation and guarding the dry powder.

Demand on this new issue of DTE was definitely weaker than some other recent issues other than DTE. Don’t know why. Did notice this issue had IG ratings from Moodys and S&P, but non IG rating from Fitch. Don’t know if that had anything to do with it or not. Personally I think DTE is a good company.

I got shares today but if the price drops some I will buy more if funds are available. I remember buying DTQ @ its IPO. As time progressed, the price declined so I bought more. Same sequence of events happened with the 2 PSA issues being called next week. At the time I was buying these 3 issues @ IPO with 5 plus % coupons, I thought they might end up being perpetual holds which I was fine with, But boy was I wrong.

Tim,

Just to be clear I have no crystal ball. When I have funds available and the one

broker I use for IPOs is a book runner for a new issue, I’m able to get preliminary price talk. I then usually give an indication of interest for shares.

When ticketing begins, some issues are sold out in a minute. Literally. Others languish. Sometimes b4 ticketing begins, demand is so strong that the book runners start talking about changes in price talk. That usually means lower yield. I get a call to confirm if I am still interested @ the lower yield. After ticketing begins, if my order is accepted I will get a call confirming the expected yield. I usually pass that on to this board. At the close of business, I can usually confirm for sure the yield. I also pass that along here.

On a day on which I have no funds available, I will not be spending time pursuing a new issue and consequently will not have any information to pass along.

razor–don’t admit you have no crystal ball–haha.