As I have mentioned too many times I have been carefully reviewing our holdings and trying to find the best balance of safety and yield–so many options all dependent on each individual investor. It has NOT been helpful that politics has become such a large part of investing decisions. While politics has always been part of investing it is now on steroids.

Regardless of anything that occurs in politics we as investors have to simply ‘deal with it’.

There are a plethora of both term preferred and baby bonds available from company’s that are collateralized loan obligation (CLO) owning companies–Carlyle Credit Income (CCIF), Eagle Point Credit (ECC), Eagle Point Income (EIC), Eagle Point Institutional (EII), OFS Credit (OCCI), Oxford Lane Capital (OXLC), Oxford Square Capital (OSXQ), Pearl Diver Credit (PDCC), Priority Income Fund (PRIF–unlisted) and Sound Point Meridian (SPMC). Every one of these companies have either term preferreds and/or baby bonds currently outstanding.

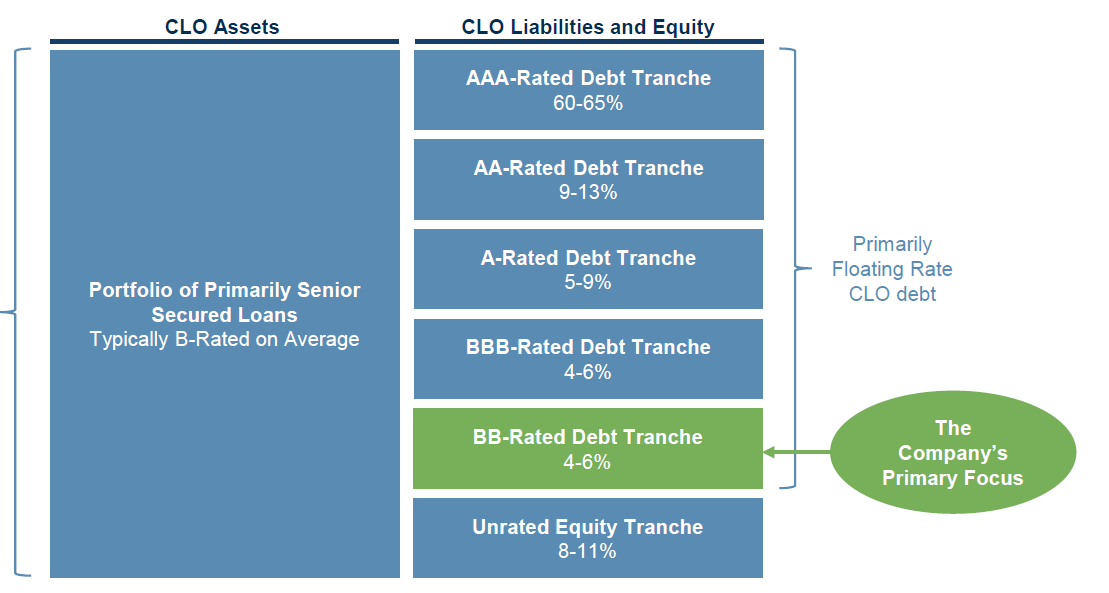

The common theme of all these companies is that they invest most all of their funds in the equity tranches of the CLO—EXCEPT Eagle Point Income (EIC) which invests exactly 75% of their funds in CLO debt. Instantly they climbed above the equity tranche in quality. Their investments are almost all in the BB tranche which is just 1 step above the equity tranche–but it has been a significant difference in the last year as equity issues have fallen substantially in net asset value while debt tranches have fallen much less. It should be noted that EIC took their equity tranche higher a few years ago–at the fund IPO they were 88% in debt tranches.

For instance Eagle Point Income (EIC) has a net asset value of about $13.80 (April 30th) as compared to $15.20 a year ago. Eagle Point Credit Company (ECC) a company holding all equity tranches of CLOs has a net asset value of $6.75 (April 30th) as compared to $9.00/share a year ago. So the EIC net asset value has dropped by 9% over the course of the last year while ECC has dropped a eye popping 25%.

I don’t look at investing in the BB tranche as providing a massive level of safety above the equity tranche–BUT it is safer and EIC has out performed the equity holding companies by a long ways. You can see the difference in quality below–safer, but not the safest certainly.

Now as we look at the term preferreds offered (although many baby bonds are outstanding) by some of these companies we can see that the safest issues (EIC) are yielding the highest current yields (at least in 2 of the 3 issues)–in my mind EICB and EICC are the best current buys. I am looking at it as the best current yield with the best quality investments–NOT by yield to maturity. If one was to look at the yield to maturity of each of these issues you would see that many times the EIC issues have the lowest yield to maturity–BUT just by a tiny bit.

So it comes down to do you want the best current yield with the highest level of safety (in CLO company’s) or are you willing to take on a bit more risk for a tiny bit of reward?

As I review my current holdings I am way (I mean way) overweight in the CLO equity section—but my risk tolerance is really much lower than the way I am positioned.

Since I want maximum safety with minimal volatility – but at the same time I want high yield I will be doing some portfolio rearranging this coming week in our CEF CLO sector–not a total wholesale change, but certainly a rebalancing so my investments reflect my risk tolerance.

Above I am not implying that holdings in any of the CLO companys are bad investments–or that any company is in trouble. Simply I am looking at them in the light of what best reflects my personal risk/reward situation. As long as the asset coverage ratio remains strong and the company has the ability to sell common shares continually preferreds and baby bonds remain safe.