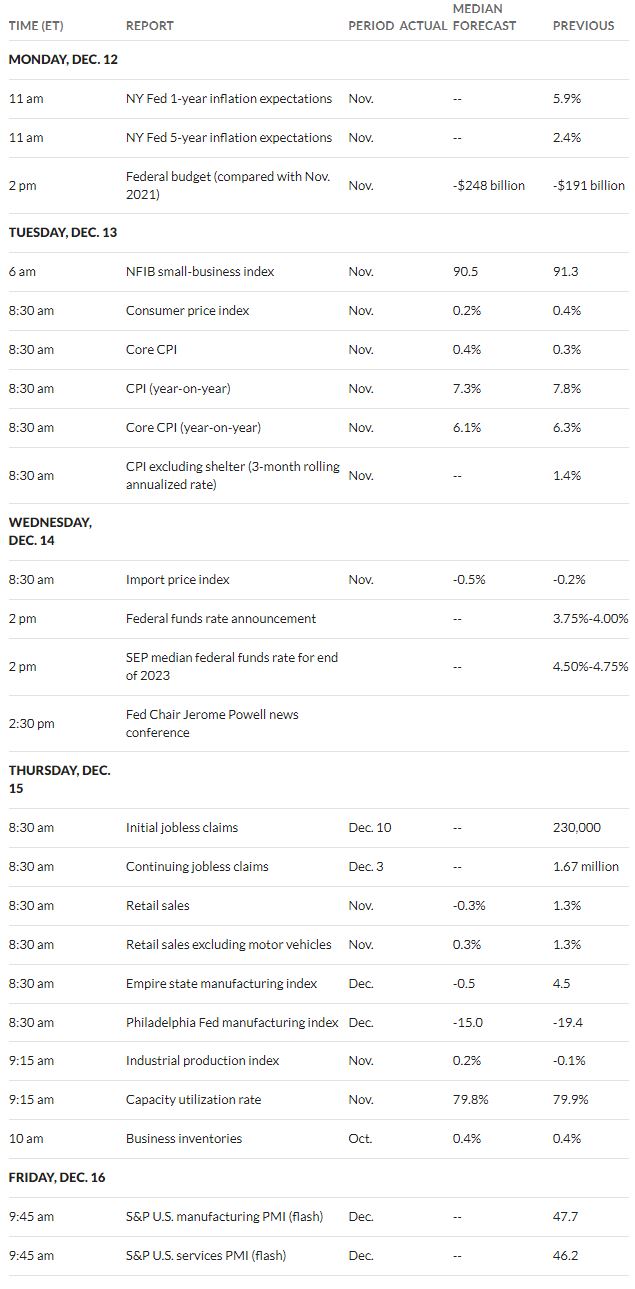

I was watching my charts as the CPI was released today and it showed exactly what I expected (up or down)–a rocket up almost 1000 Dow points and a huge drop in interest rates.

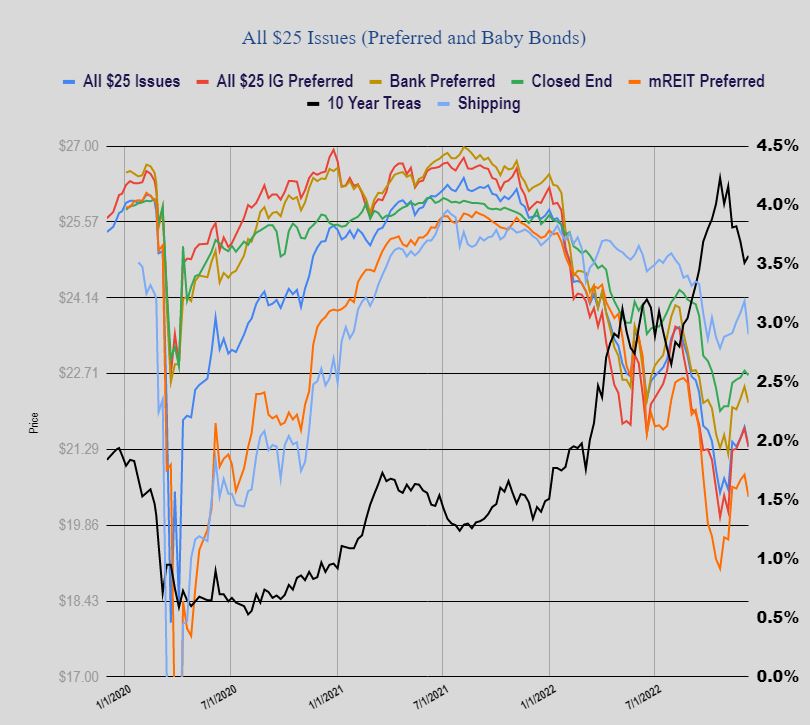

I didn’t expect that the indexes would give back everything (or almost everything)–fortunately interest rates remain low at 3.48% – down 12 basis points on the day, although the 10 year was as low as 3.43%. Income issues have skyrocketed–one of my accounts is up about 3/4% which helps to restore some losses from previous days.

As we look forward to tomorrow and the FOMC meeting (started today) we can be very certain that we will see a 50 basis point hike–todays report cemented that in–but I also expect Powell, during the news conference, to be fairly sober and warn that it would be easy for inflation to remain hot or even tick higher. But certainly there should be no surprises relative to in the fed funds interest rate hike.

Keep your seatbelts on for tomorrow–and hope you don’t need them.