Yesterday was a simply a ‘silly’ day in the markets.

We start with the consumer price index (CPI) which was reasonably close to forecast–year over year at 5% versus forecast of 5.1% with the core rate at 5.6% which was right on forecast. Equities opened higher fell back and started a gradual climb. Then at 1 pm (central) FOMC meeting minutes–which is old news–and equities just fall off a cliff.

Then, of course, we have Triton International (TRTN) announcing they would be bought by Brookfield Infrastructure (BIP) and the preferred shares tank–Ready, Fire, Aim. It is likely that the dividend is safe and will continue to be paid as long as Triton is performing well financially–historically the various Brookfield companies expect the company being bought to ‘pay their own way’–what I mean by this is that Brookfield isn’t there to provide deep pockets and if Triton doesn’t earn the dividend it will not be paid. Previously Brookfield Business Partners (BBU) bought Altera Infrastructure and when Altera hit financial hardships the preferred dividends were suspended and subsequently Altera was taken into Chapter 11 and preferred holders were wiped out. Many know of the DTLA properties that Brookfield Properties bought – financially troubled from the get-go dividends were suspended for many years before a bankruptcy filing occurred in recent history.

Then we have the SiriusPoint preferred (SPNT-B) shares getting hammered down $2/share because they have received interest in a possible acquisition–talk about nervous nellies.

I have no Triton shares and only a very modest position in the SiriusPoint preferreds.

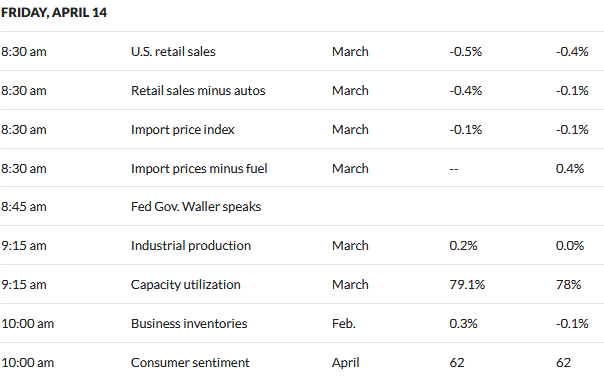

So this morning we will have the producer price index (PPI) released at 7:30 a.m. (central) – don’t know if we will get much market reaction, but we also have initial jobless claims which is an important number.

I didn’t do a thing yesterday – in fact I didn’t even look at my accounts until after market close–but with a gaggle of CDs and treasuries my portfolio don’t reflect craziness.

Well let’s see how markets trade today.