Watching equity indexes earlier today made me think ‘am I crazy’? I’m looking at not just the current economic conditions, but at what I think is likely a year out. I am super conservative, but I am trying to take the optimistic view of the global economy.

I see 15-20% unemployment (current) and at least 5-8% unemployment a year out–how does that translate into equity prices that are only 15% off all time highs?

I see earnings releases from some of the drug companies that are pretty good–I see 3m being pretty good–no surprises here. But who is buying cars–a lot less folks than a month or two ago. After an initial pop as folks rushed to set up home schooling sales of electronics, appliances etc have dropped off a cliff–Best Buy said after this initial pop sales were going to off 30% in April–a year from now are they going to gain all of the sales back?–I don’t think so. A company like Best Buy runs on very skinny margins sales off 5 or 10% means long term layoffs.

Talk about a disaster–unemployment. Folks still haven’t gotten payments in many (most?) states. I know people in Minnesota that applied in March and a month later they have no clue whether they will see some money. Folks are running out of money–the $1,200 helicopter money lasted about 1 day–and now since folks have been trained to get a personal bailout everyone wants more.

Some businesses have reopened, but folks did not flock back to them–maybe those businesses got some PPP (payroll protection) money–but the rent, taxes, utilities and other overhead continues and if sales end up down 50% for the next few months those small businesses are toast–some that are getting PPP money are already toast–but everyone wants money, whether they survive or not is a different story.

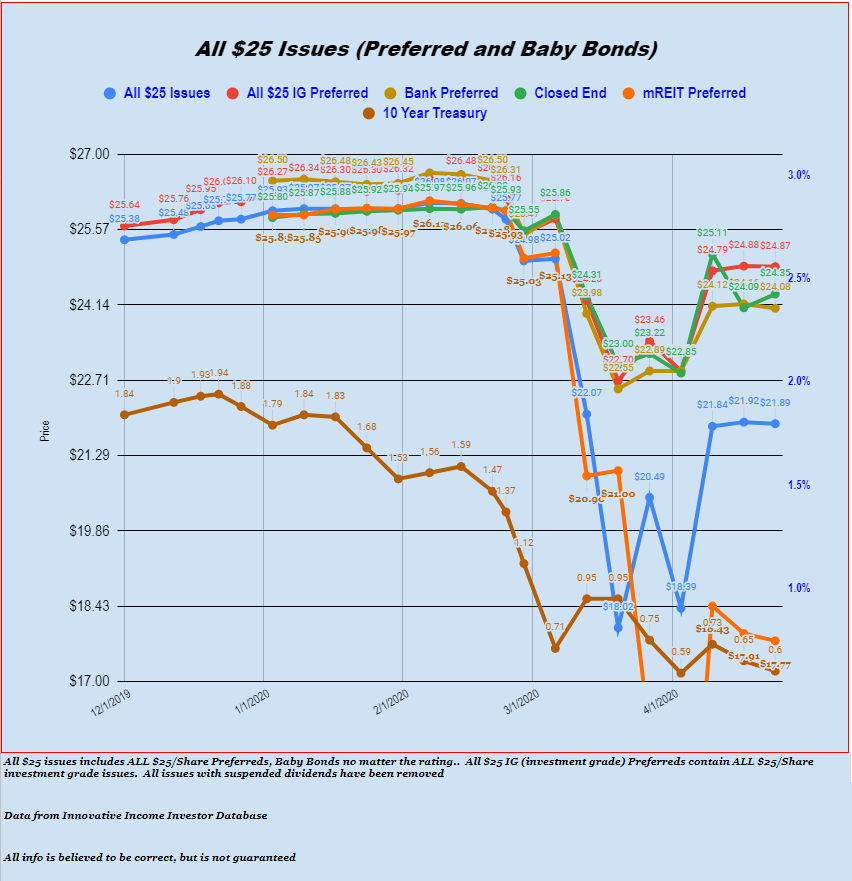

In spite of the ominous outlook I have done some nibbling this week. I bought the Annaly Capital NLY-G, another taste of Hersha Hospitality HT-E, some Two Harbors TWO-D, and some WR Berkley WRB-B. Not much of any of these issues and some were additions to current positions. Some are already redeemable–but as long as they are under $25/share it is not a problem.

I remain in the 65-67% invested range–and honestly I would be surprised if I go above 70% in the next few weeks. I need realism in the marketplace and until we start getting a 2-3% loss in equities week after week I don’t think there is realism–we remain in the ‘don’t fight the fed’ market—-these are ‘fake markets’.