As we have watched interest rates go down, down, down over the last few years it was only a matter of time before fixed-to-floating rate preferreds began to be impacted.

Up until this point we have had just a few issues that were in their respective ‘floating rate periods’ where the coupon would reset every quarter–normally to 3 month Libor plus a fixed spread.

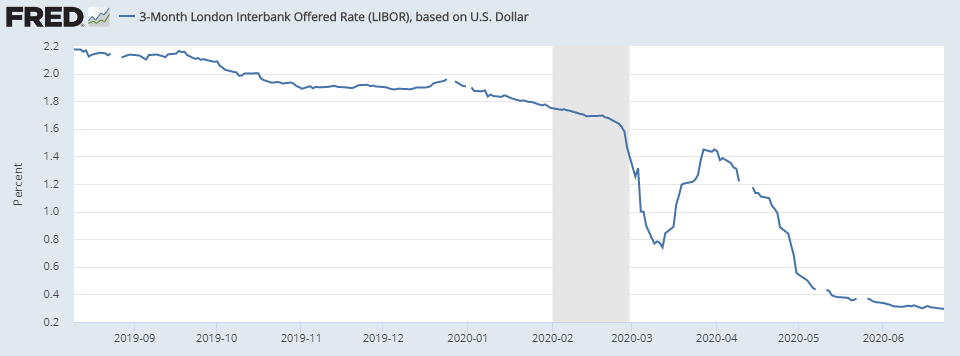

As most of you know 3 month libor has been on a downward trend for years and now is in the .3% area. This means that almost all fixed-to-floating rate issues which were issued years ago will see falling coupons when they enter the floating rate period.

We have a list of all the issues with their ‘potential’ coupons here.

Even worse these issues have no floor to the 3 month Libor reset level–if 3 month Libor goes negative coupons will keep right on falling.

So let’s look at the most recent example and that is the Customers Bancorp 7% Fixed to Floating non cumulative preferred (CUBI-C).

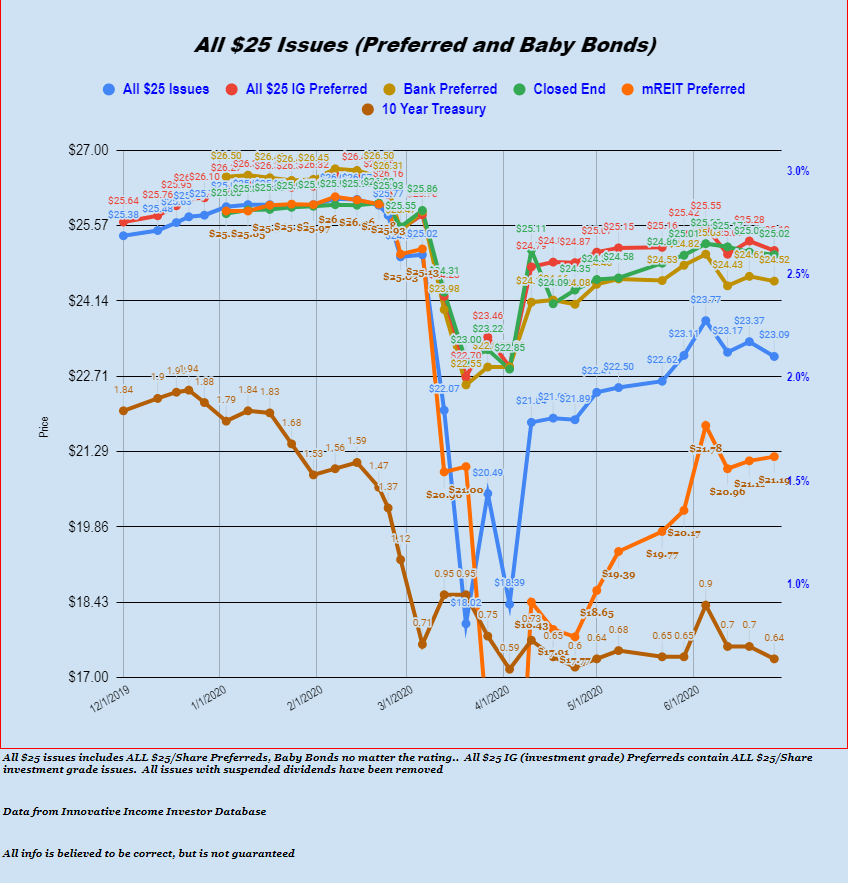

This issue was tooling along with pricing in the $26 area all the way until March 1, 2020–of course shortly thereafter we had the COVID 19 disruption and the share price fell to $14—but now recovered to $21.24

The terms of the issue would become 3 month Libor plus 5.30% on 6/15/20 — the first dividend payment date would not be until 9/15/2020 under the floating rate structure. If 3 month Libor remains at .3% the new coupon will be 5.60% for the next payment in September.

Knowing what we know today about interest rates the conundrum is whether the CUBI-C issue is a good buy at $21.24? With a coupon of 5.60% the current yield would be 6.60%.

3 month Libor has never traded at negative levels (going back to 1986), but these are not normal times we live in and one should never say never when making a forward looking forecast.

If 3 month Libor falls the coupon will fall for this issue and share pricing would likely follow.

But let’s make this a little more complex. What if interest rates generally and the 3 month Libor in particular jump by 1%? With bond like securities you would normally expect price to move in the opposite direction to rates–but not here. If 3 month Libor moved higher it is likely the share price would move higher, although it probably is more complex–meaning the level of the 10 year treasury would affect pricing as well.

In the case of CUBI-C if 3 month Libor moved sharply higher while the 10 year treasury moved only modestly higher it is possible that Customers Bancorp (CUBI) could potentially redeem the issue in which case a huge capital gain could be realized by the investor. It is hard to fathom this scenario occurring–but as I wrote above never say never.

Currently this is the only fixed-to-floating rate issue that Customer Bancorp has that is in the floating rate period, but they have another 3 issues that will go into the floating rate period in the next 18 months–all currently priced in the $19 to $22 range–all of which are already factoring in reduced coupons.

So it is quite the puzzle—and your action really depends on your personal outlook for interest rates.

Currently only a handful of fixed-to-floating rate issues are trading in the floating rate period–but in the number of years we will see bunches of issues go floating.

As noted by many we are starting to see large spreads coming with the new issues. Additionally as DoubleV pointed out we have the Fixed-Rate Reset issues coming with large spreads–for instance the newer Wintrust 6.875% non cumulative preferred comes with a spread of 6.507%.

What we are still missing is a ZERO floor in the variable portion of the coupon–if 3 month Libor–or alternatively SOFR or the 5 year treasury goes negative–the rate is zero—I won’t hold my breath for this in preferred stocks.