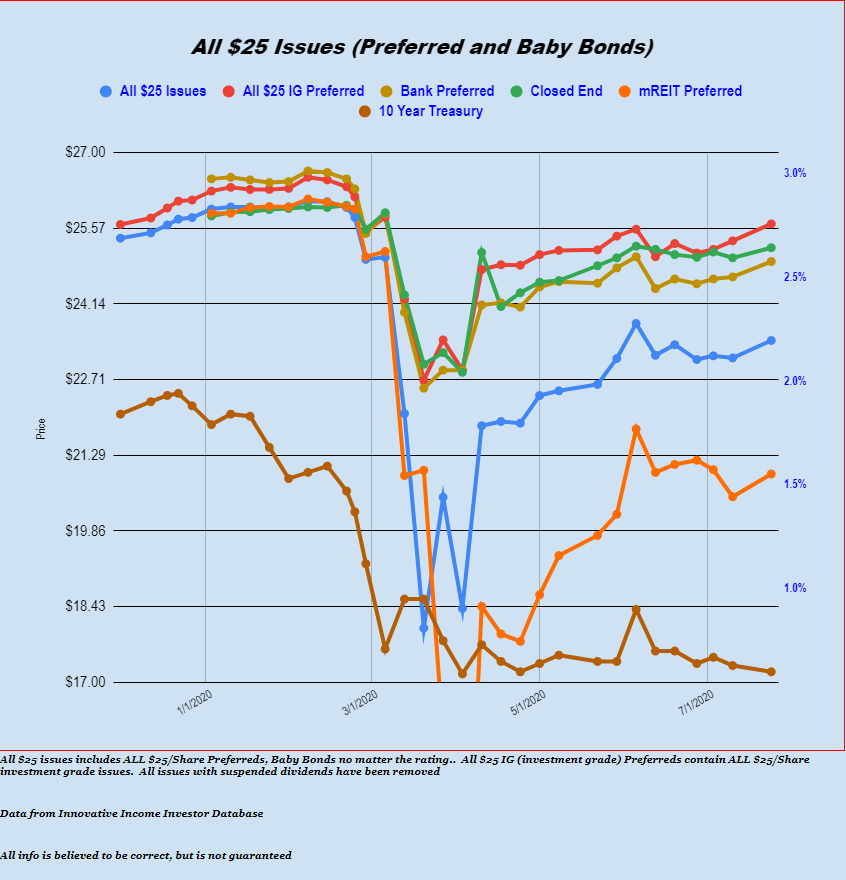

Below you can find instructions for the sortable $25 master list (baby bonds and preferreds stocks)–finally after months of being too busy to get this updated I have all but a few issues now included–I hope to get the last few added within a week.

If you already ‘know the ropes’ on this spreadsheet you can go right to the spreadsheet here.

Version 1—12/16/2019

Version 2 —2/15/2020

Version 3—3/4/2020

Version 4–7/29/2020

NOTE THAT NEW VERSIONS HAVE CALLED ISSUES REMOVED AND NEW ISSUES ADDED

UNTIL THE NEXT VERSION IS RELEASED (60-90 DAYS) NEW ISSUES ARE NOT ADDED UNLESS YOU DO IT ON THE COPY YOU MAKE

Please NOTE that this will not work with EXCEL only Google Sheets.

- You need a Google Account to use this sheet correctly. Go here to set up an account if you do not have one. While an account gives you gmail and other apps it importantly gives you an account for accessing and using Google Sheets.

- After creating an account with Google make sure you are signed in.

- Go the the sortable spreadsheet which you can find here.

- Once you open the spreadsheet as long as you are logged into your Google account the spreadsheet will automatically be in your spreadsheet list.

- You will see that when you open the spreadsheet it will say ‘view only’.

- Make a copy of the sheet for yourself–go to File, Make a Copy then give it the name you want.

- You will now be able to use own copy to sort etc.

Note that there are 3 sheets to the spreadsheet–I have hidden 2 which are not needed by you unless you wish to make changes. The tab you need is labeled “Filter”.

Unless you are very well versed in Google Sheets I would suggest not modifying the other 2 pages–BUT if you are like me and just can’t help yourself you can always come back here if you ‘break’ the sheet.