Below are press releases from companys with preferred stock and/or baby bonds outstanding–or just news of general interest. Earnings season is pretty much over so we will have slow news days for a month or two.

I own 2 different issues of BrightHouse Financial (BHF)—I own the BHFAP 6.60% issue and the BHFAN 5.375% issue. As I surveyed holdings this weekend I said to myself ‘what the heck were you doing buying that issue’? This was in reference to purchased the 5.375% issue on October 1, 2024. I already was highly suspicious of owning perpetuals at that time and I paid a price for this ill advised trade taking a loss that could well have been avoided.

I have no problem with Brighthouse fundmentally, I simply want to own fewer perpetuals with inferior coupons (inferior at this time). Moves lower in interest rates in the next month or two are maybe not likely (of course we have to see the data)–with a new administration everything is hazy in this regards.

I noticed today that CD rates continue to drift very slowly downward–most at 4.30% – 4.40% on the 3 month at Fidelity and eTrade. Still a reasonable rate to hide out in until other opportunities arise–hopefully in short duration issues.

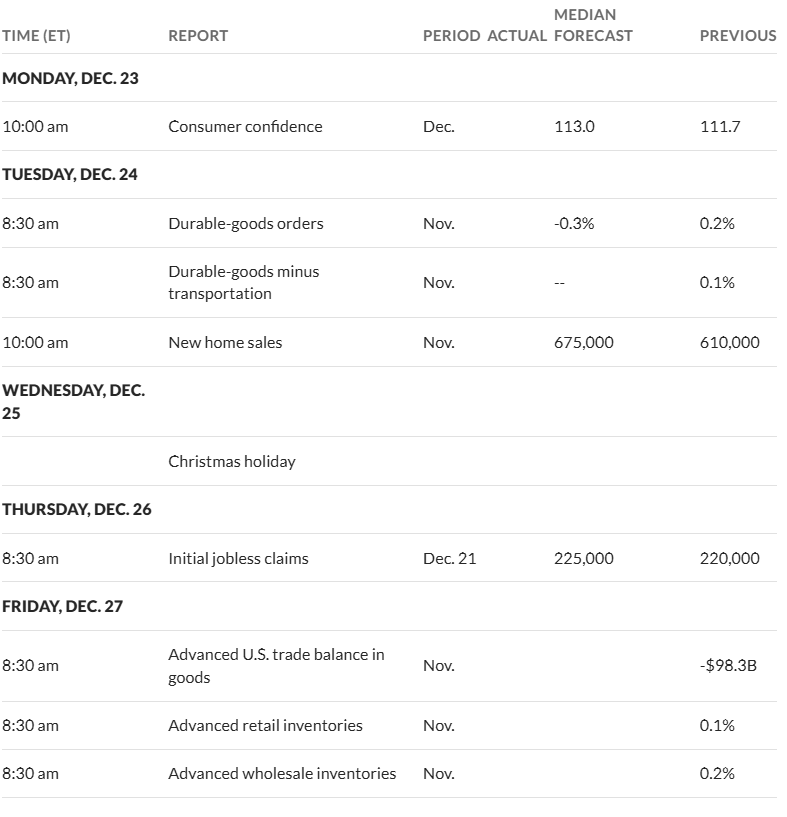

It was kind of a ‘wild’ week last week–so are we going to have more of the same this week? Actually this week could be a bit quiet with the Christmas holiday dead in the middle of the week on Wednesday–actually equity markets will close early on Tuesday at 1 p.m. (eastern time). Just remember that when volumes are thin movements could be exacerbated–but I am not expecting giant moves.

Last week we saw the S&P500 lose right at 2% on the week–but at the low the index was off by 3.75%. Of course we saw the big plunge on Wednesday as stocks fell all afternoon as Jay Powell gave what was perceived as a hawkish press conference. I personally didn’t see it as hawkish, but I didn’t have my rose colored glasses on–obviously I was in a minority. The index remains just 2.8% off of the all time high–it will be interesting to see if this index can set new highs–we may well see some folks locking down some profits in early January as we get closer to the new administration coming to power and bringing with it all sorts of uncertainty.

While equities were taking a tumble the 10 year Treasury yield was jumping–as high as 4.59% before settling down and closing the week at 4.52% which was 12 basis points higher than the close the previous Friday. Of course interest rates reacted to Jay Powell–investors had their expectations ‘reset’. The personal consumption expenditures (PCE) were released on Friday and were fairly tame which kept the situation from growing worse.

This week most of the economic data to be released,while important, is not likely to move markets much–if any. More likely is that the lack of faith in our Congress could set off selling–the CR passed late Friday doesn’t inspire great faith in the ability of politicians to begin to cut spending.

The Federal Reserve balance sheet fell by $8 billion last week at $6.89 trillion.

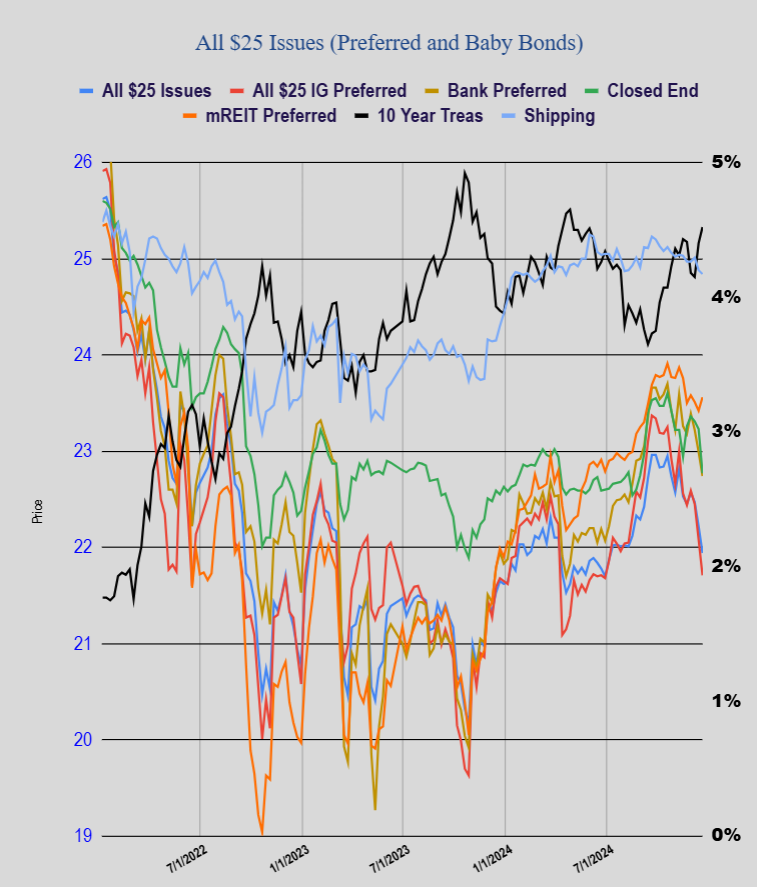

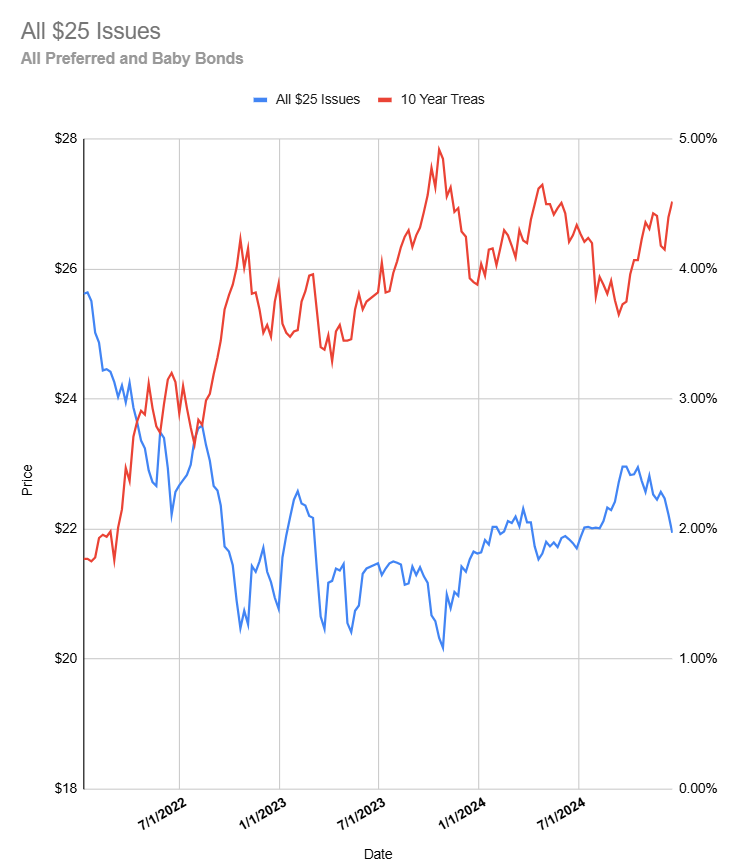

Last week, as one might expect, the average $25/share preferred and baby bond fell in price–by 28 cents. Investment grade issues fell by 37 cents, banks by 24, CEF preferreds by 46 cents, mREIT issues rose by 14 cents and shippers fell by 4 cents.

In a couple hours we have the personal consumption expenditures (PCE) number being released and the forecast is for the number (year over year) to come in a little hot. At this point in time any number cooler or hotter than forecast can move markets quite a lot and certainly set the tone for the day. The 10 year treasury yield is down 2 basis points at 4.52%–would be nice to get a PCE number that starts to send the yield back lower.

The S&P500 futures are off about 3/4% at this moment. I believe that this is caused by what is a continual inability of Congress to get their act together and the rejection of the latest CR (continual resolution) last night. As I mentioned yesterday any sign that Congress is serious about cutting spending will be met positively by markets–while business as usual will be punished.

I was noting yesterday that real estate investment trusts (REITs) have been getting slammed–really slammed. The most followed REIT ETF the Vanguard Real Estate Index (VNQ) closed below the year ago level after being up 10-12% just a few weeks ago. As most of you know Brad Thomas created his own REIT ETF in the spring–the net asset value (NAV) yesterday closed 1% below the original issuance price–it goes to show that in investing there are no ‘magic’ formulas and prices move on more factors than fundamentals–if it was that easy we would all be billionaires.

I have been pondering the future–not the next 10 years, but the next 6 months to a year and will have my thoughts on interest rates to publish soon. Recall that I thought the 10 year Treasury yield would fall this year into the fall and then we would see them rise as Congress continued to spend like crazy. In a blind squirrel moment I was correct–probably I won’t have this level of lucky guessing again, but I really need a level of comfort in my own thoughts in order to move forward with my own allocations. Right now I am guessing my 7% target is at risk–I might have to realistically reset to 6%–we’ll see.