The S&P500 was generally quiet last week closing at 4138–which was a .8% gain–better than a poke in the eye with a sharp stick. The range for the week was 4072-4163–around a 2% range.

We have seen the earnings from regional bank M&T Bank (MTB) and the revenue and earnings both beat forecast–State Street Bank is yet to report today and most of the regional/community bankers will be reporting this week or next–I will be watching closely.

The 10 year treasury was a bit more active than equities moving in a 3.34% to 3.54% range and closing at 3.52% on Friday–this is 23 basis points higher than the previous Friday close.

This week the economic news is of the more minor variety although we have some Fed yakkers and they can cause trouble–although they have been uniformly hawkish lately so I think investors are getting used to their rhetoric.

Last week the Fed Balance Sheet fell by $17 billion as the stress comes off of the banking system. The balance sheet is $225 billion (more or less) higher than it was just prior to the banking crisis back in early March.

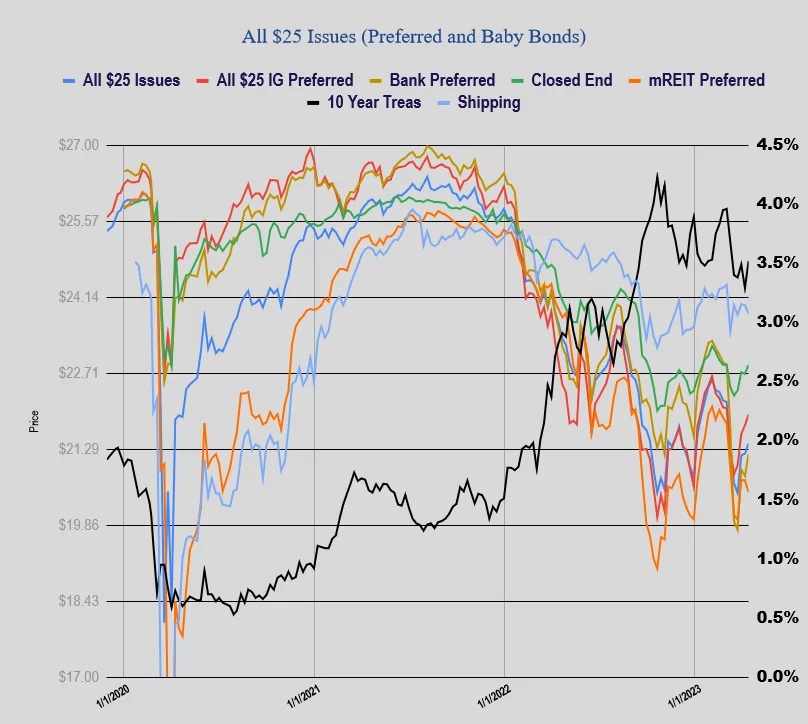

Last week the average $25/share preferred stock and baby bond moved higher by 23 cents with investment grade moving 21 cents higher. Banks moved 40 cents higher, CEF preferreds were up 17 cents. mREITs were off 22 cents and shippers down 16 cents.

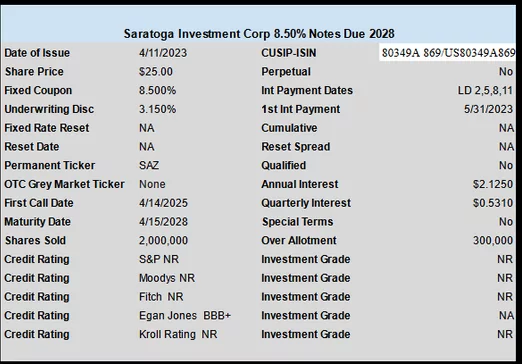

.We had 1 new income issue priced last week with BDC Saratoga Investment (SAR) pricing a new baby bond with a fixed rate coupon of 8.50%. The new issue will trade under ticker SAZ–I don’t see it trading yet.

Well we had the big banks reporting earnings this morning and JPMorgan (JPM) and Wells Fargo (WFC) both beat forecast as was expected. I am more curious how the smaller banks are doing–the regional banks etc. I want to see how the commercial loans are holding up–some of the community and regional banks specialize in multi-family lending–how is that holding up?

Yesterday ended up being a very solid day in the markets–stable prices in equities with interest rates mostly flat. My portfolios move only minor amounts on days like yesterday- little up or little down–that’s fine since I am not really expecting upward moves in the portfolio, just hope to dodge any major losses.

I am sure most of you that have bought CDs and treasuries (like I have) in the last 6-9 months are very pleased with your interest payments when you look at your brokerage statement. Seeing a monthly 4 digit interest total is very sweet after seeing zip the last many years. Balance these receipts with some solid 6-8% preferreds and baby bonds makes for a great risk/reward balance. I actually bought a few 5 year CDs in the 5% area – not many, but who knows what the future holds so get a little when you can. IF we see inflation in the 2% area in a year or two 5% CDs will probably go away, but we shall see.

Well let’s get this day rolling–with futures and interest rates fairly flat we will likely see a quiet day without fireworks–fine with me.

Well today started off right with the producer price index showing a month over month reduction in prices of 1/2%–of course it is just 1 months worth of data so to some degree not ultra meaningful, but just the same it feeds into the interest rate decision in 3 weeks. 1st time jobless claims were up from last week and above forecast a bit which is also an important ‘sign’ for the Fed.

Tomorrow we have what is normally a batch of less important economic news – but in recent history everything can be important.

Interest rates are pretty much holding flat at 3.42%–doing nothing at all.

Preferreds and baby bonds are mostly holding their own – with a green tilt up. I keep checking my good-til-canceled buy orders and nothing happening there which is fine–I have plenty of dry powder, but as long as it is collecting 4-5% I am happy being very patient.

I see the Triton (TRTN) preferreds are mostly up 2-3% today–I suspect they will climb back over the course of the next week or two, but folks are pretty risk adverse so I doubt we see all the losses from yesterday recouped–but who really knows. I pretty much don’t play in these situations anymore – just not motivated to take the risk.

Well let’s see if equities hold their gains without puking today–unlike yesterday.