Each day we hear less and less on the banking situation–is it gone? Resolved? Not a chance.

All through the financial system we are going to see band-aids being applied to deep problems–kick the can down the road some more, just like we have been doing since 20 years ago (or more). Regulators? I have little faith in the regulators of banks and insurance company’s – at least on the federal side of regulations – most insurance company’s operate under some sort of state regulators and maybe there is more nerve there to regulate–maybe.

So as we wait for another ‘shoe to drop’ it is near impossible to have huge amounts of confidence in investing–on one hand if you wring your hands and hold cash (or cash equivalents) you may miss out on some huge capital gains and very tasty current yields–on the other hand if you invest heavily and an ‘event’ happens you could get burned badly.

Yesterday I bought a position in the Jackson Financial 8% fixed rate reset preferred (JXN-A) and I added to my Lincoln Financial 9% preferred (LNC-D). These are small positions – 100’s of shares – not 1000’s of shares. I’m pretty conservative – and the odds I am going ‘all in’ on these issues (or similar issues) is exactly ZERO. I may add more in the next month or two, but I really want more data–i.e. earnings reports etc. I would rather look back and see that I missed some gains than to wake up some morning and find an ‘event’ has rocked the financial sector. It takes only 1 bad security to inflict massive portfolio pain on investors so I encourage folks to use caution and ‘leg in’ to positions.

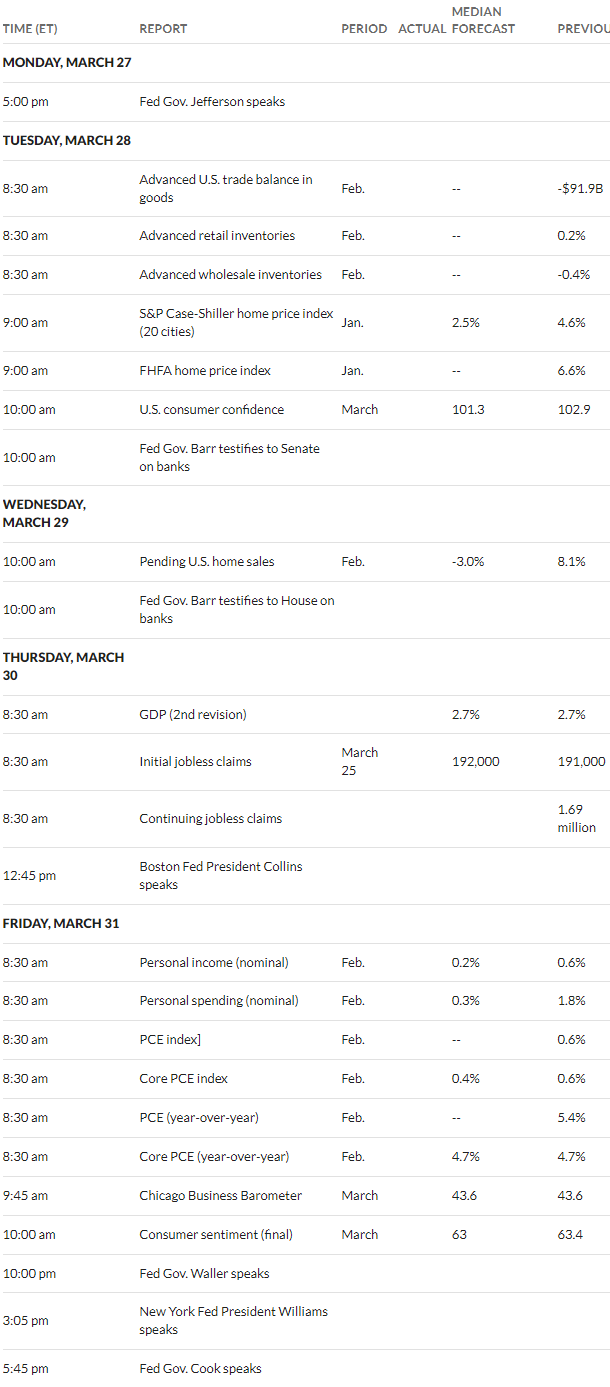

So today we have a number of economic reports hitting starting in 90 minutes with retail and wholesale inventories at 7:30 a.m. followed up by the Case Shiller home price index and the FHFA home price index at 8 a.m. (central) and consumer confidence at 9. Market movers?–not likely too much. Fed vice chair Barr testifies to the house today–supposedly on banking, but who knows where this goes.

Well markets are quiet with little movement n the S&P500–let’s get it going and see if we can keep it quiet.