Markets are not just about inflation–an equal influence on the economy is jobs and there have been few (if any) signals that we are seeing any job softness. Once again we got a jobs number yesterday that did NOT indicate softness when ADP reported their March number for new jobs created when they reported 184,000 new jobs created against a forecast of 155,000. Additionally the company reported a higher revised February number. New jobless claims for the last week will be reported in 90 minutes and the forecast of 213,000 is likely to be higher than reality–the forecast has been too high most weeks this year–we’ll see.

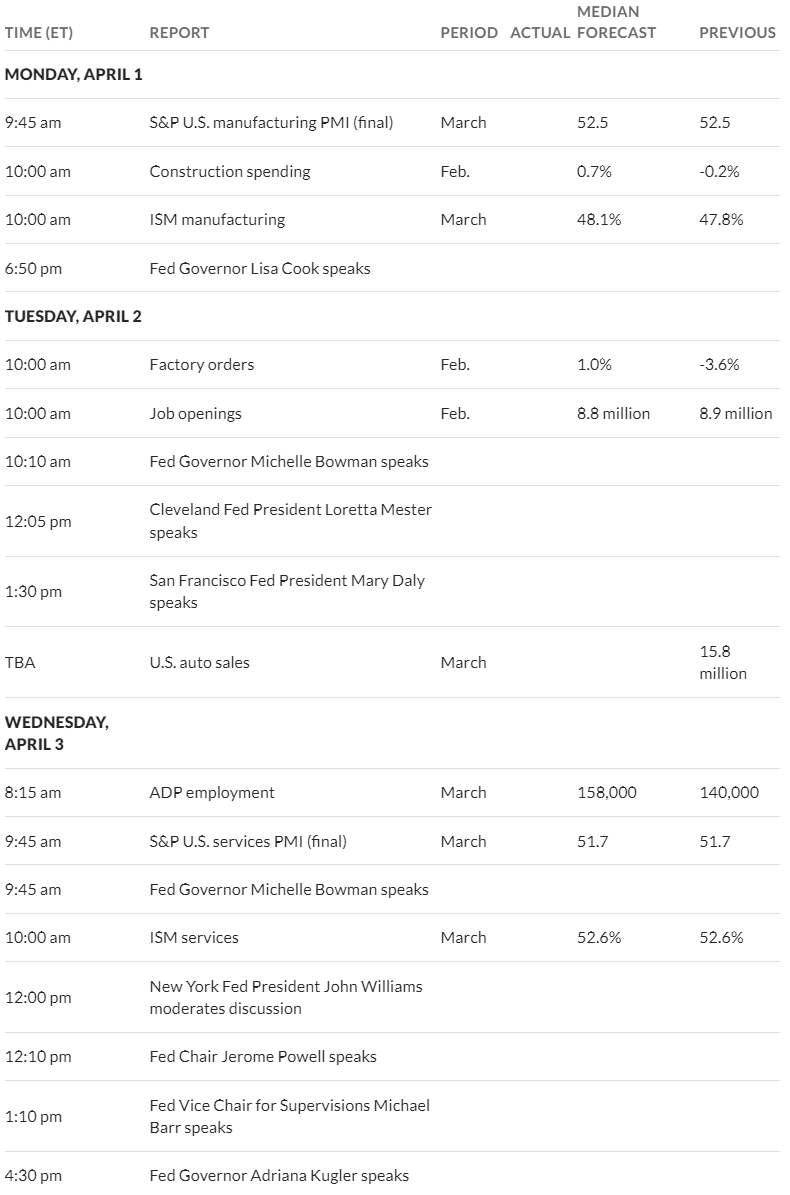

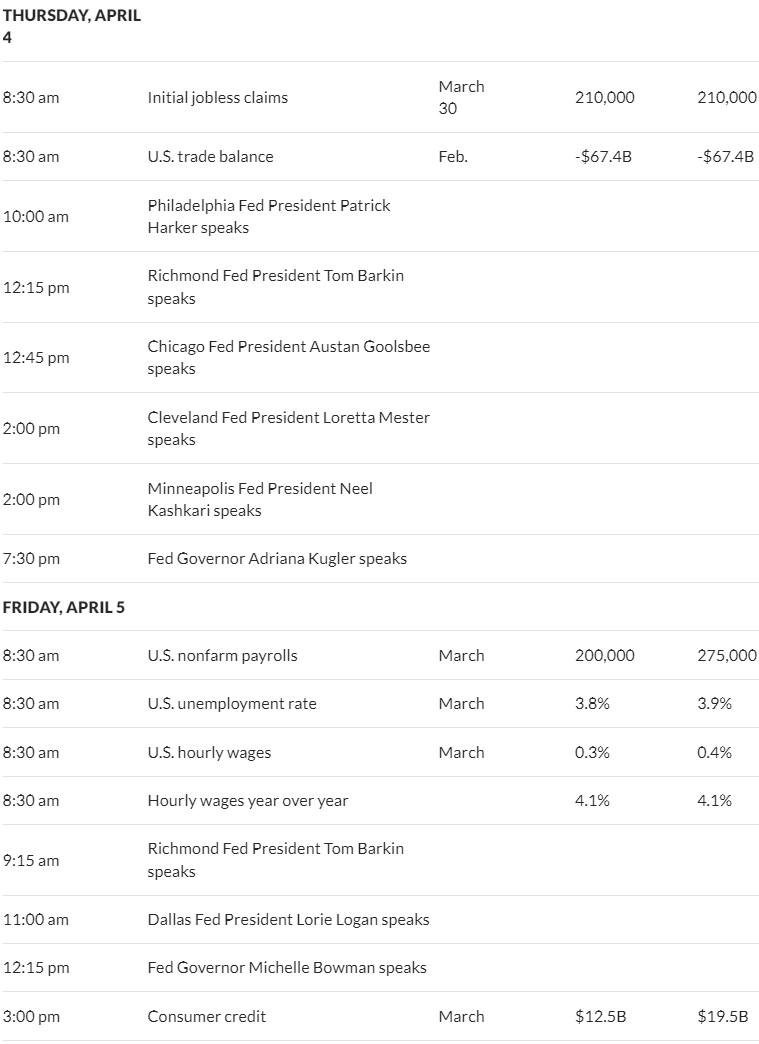

Tomorrow we have the ‘official’ government report for March–forecast is for 200,000 new jobs which is not a blockbuster number, but it certainly doesn’t indicate a failing economy.

I have been watching oil prices–how can one help it as we have to buy fuel for our vehicles. West Texas intermediate has been trading in the mid $80’s for the last few weeks–this is 15% higher over the course of the last year an up 18% YTD. These prices bleed into the economy-over time and you can be certain that the negative affect on overall inflation is going hurt at a time when folks are pretty sick of paying higher prices, although not sick enough to quit buying inflated products apparently.

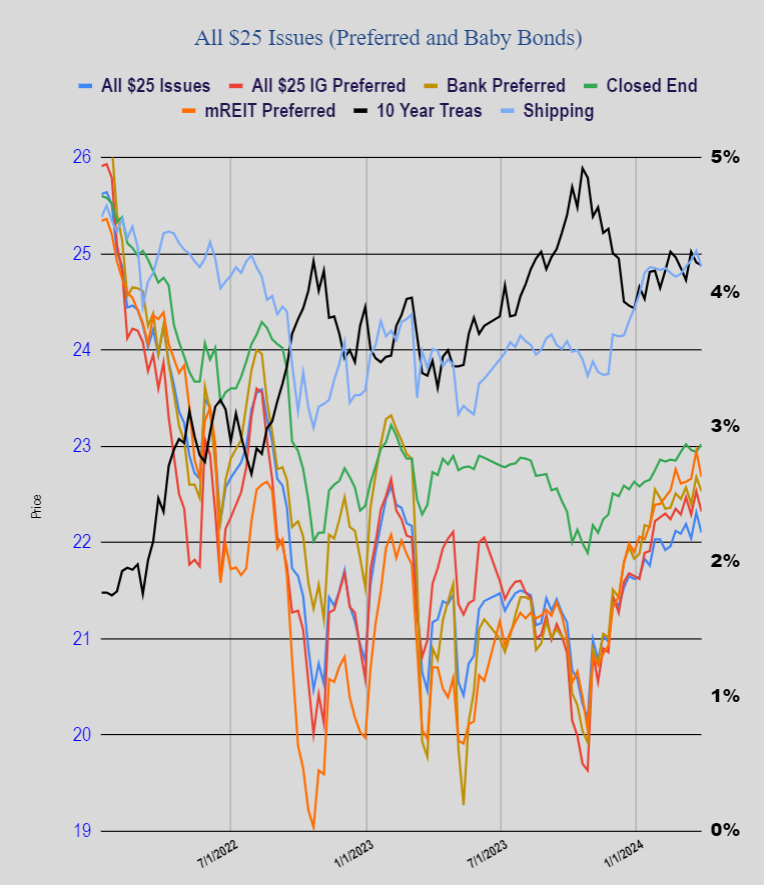

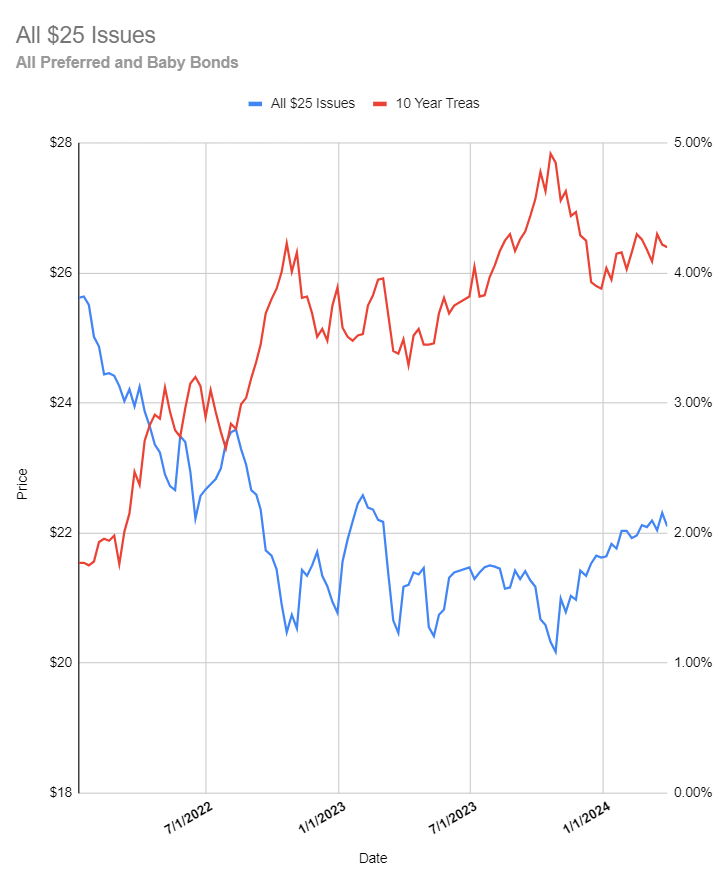

Everything points to higher rates for longer–what is longer? Who knows for certain, but if inflation remains elevated (above 2%) and employment remains fairly strong why the heck would the Fed lower rates? Honestly interest rates are NOT high–on a historical basis. Folks want free stuff–including free money–but as an investor I want to be paid for others to use my money. For years they wanted my money and didn’t want to pay me for the use–now I am getting paid a fair rate and it makes me very happy.

The 10 year treasury is at 4.37% after popping to 4.40% yesterday on strong employment–tomorrow we will see if rates are shoved higher or lower with the March employment numbers–it is a very important number.