Talking about common stocks it sure looks and feels like we are moving into a Goldilocks phase–with a downward tilt. No one can foresee the future and we don’t have many more ‘bailout’ programs left at this time to ‘juice’ the market.

Seems to me that folks are slowly accepting that the economy will be in rough shape for many quarters–fortunately folks are not panicking just slowly rotating their holdings.

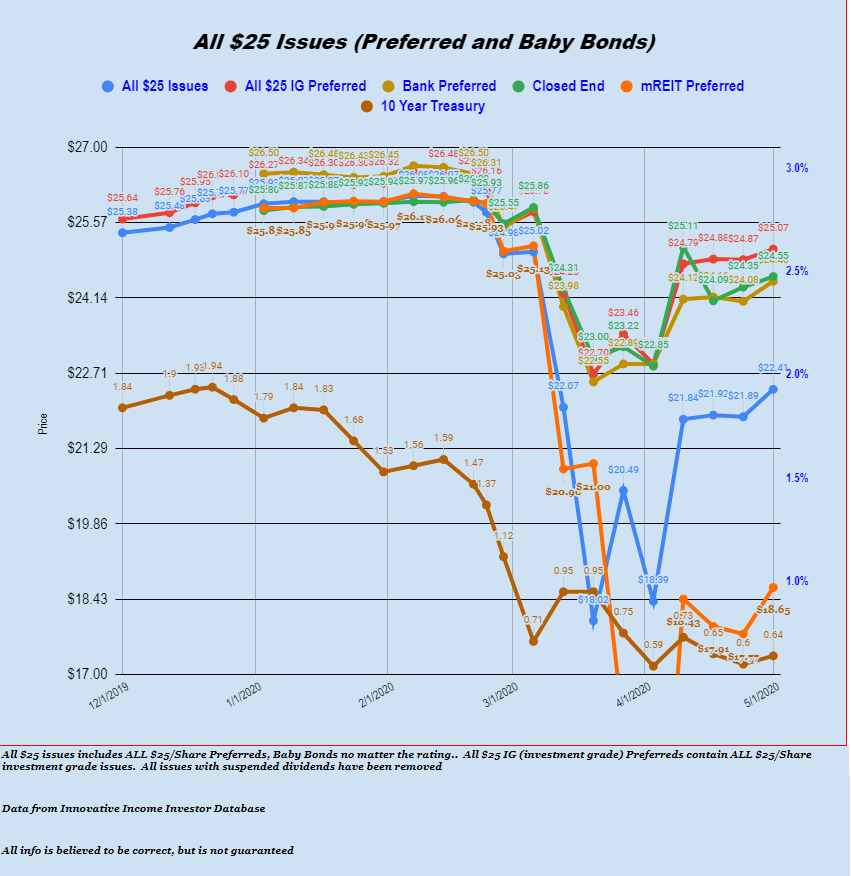

In the arena most of us play in – preferreds and baby bonds, the deals are likely gone for now–the panic selling done. From this point I think most deals will come in reaction to individual companies having issues–many in the REIT arena and in particular mREITS, lodging REITs and I suspect in some of the triple net lease issues. These will all play out over the next 12 months.

We are now getting the reports of the damage in the collateralized loan obligation area. Oxford Lane Capital (OXLC) has released their NAV (net asset value). The company burned up almost 50% of their NAV since 12/31/2019—ouch. The company will continue to pay a couple monthly dividends already declared but then likely will suspend the common dividend there after.

It is very interesting to watch the term preferreds from Oxford Lane–they have 3 issues outstanding. They are trading with current yields of around 8.5%–not bad for junky issues. This is a test of the asset coverage rules–they have to cover preferreds by 200% and debt by 300%–my suspicion is they have broken coverage.

I have written before that Oxford Lane, Eagle Point Credit and Priority Income (all CLO holders) would have challenges in a recession. Because of their structure–no matter how poorly the common shares do, I think they will eventually be just fine–no guarantees however.

Just like the above issues we will wait to see howly poorly the financials are in the business development sector (BDC). Undoubtedly there will be significant damage—if you are making loans at 15% you have to know that there will be defaults a plenty. These announcements in the future may create some deals for us in the BDC baby bonds–only time will tell.

Today the only activity I have done is that earlier today I let go of 1/2 my SDS short hedge–still hold a little, but with panic maybe waning I think I don’t want to be too short.