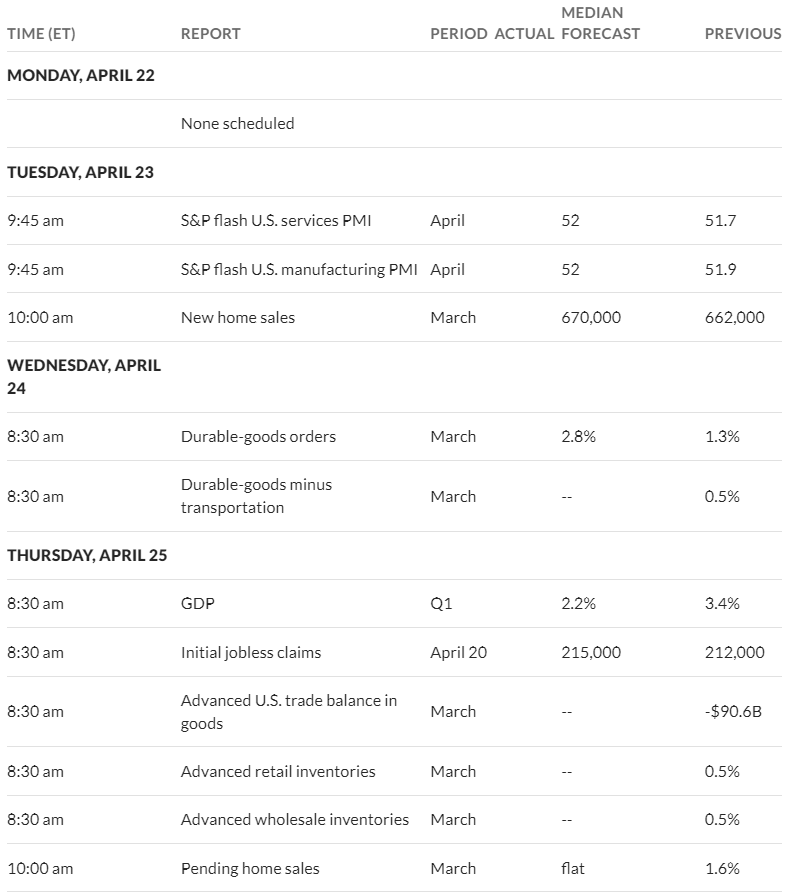

Well the big question in my mind is where will interest rates go this week? Maybe they will be quiet all week until Friday when the PCE (personal consumption expenditures) number is released–if we see a number which is off the forecast we could see an explosion higher–or a giant sized drop. A hot number will set off discussion on a rate HIKE, which I would hate to see.

Last week the S&P500 fell by 3%, closing under 5000 for the 1st time since February 13th. The index remains just 5% off an all time high so really not too much of a pullback to this point and certainly we could see a continuation of this setback–just hoping that losses are modest. Like interest rates it is not just the direction of equity movements, but the speed that they move that hurts income investors. Who know what will happen? I can’t forecast equity movements that is for sure.

Interest rates ended the week at 4.62% (the 10 year treasury) which was up 12 basis points from the close the previous Friday and the highest weekly close since the week ending November 10th, 2023. The Fed ‘yakkers’ are now almost all uniformly hawkish on rates and keep pounding home the inflation goals and even hinting that the Fed will raise the Fed Funds rates further if warranted. This week the big economic number, of course, is the personal consumption expenditures (PCE) index on Friday, but we do get a 1st look at Q1 GDP on Thursday.

The Federal Reserve balance sheet fell by $33 billion last week–resuming the normal $95/billion in monthly runoff after a 1 week pause.

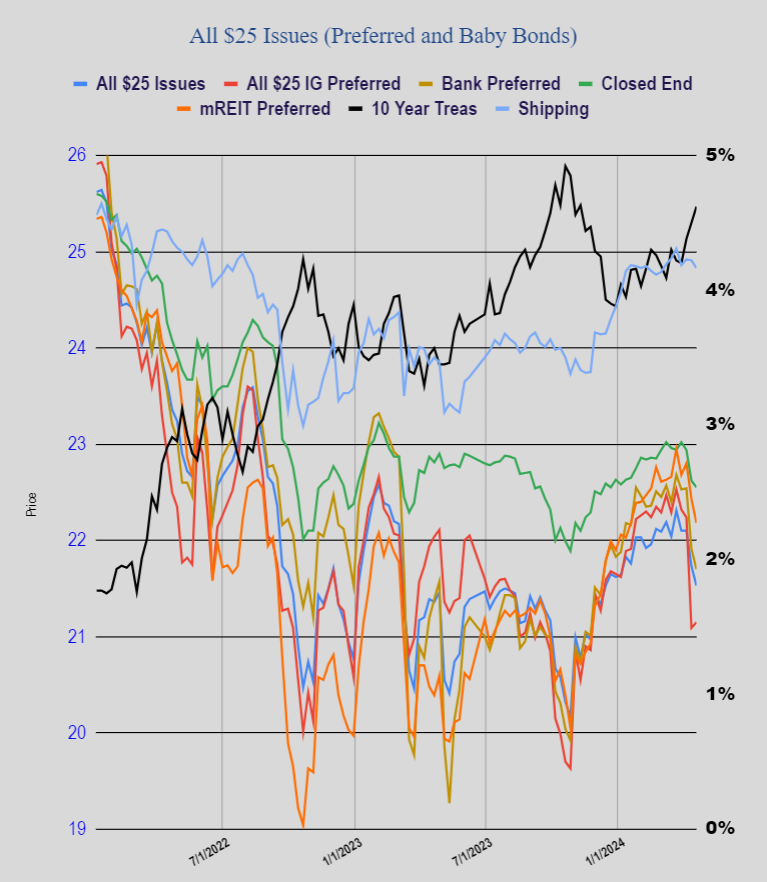

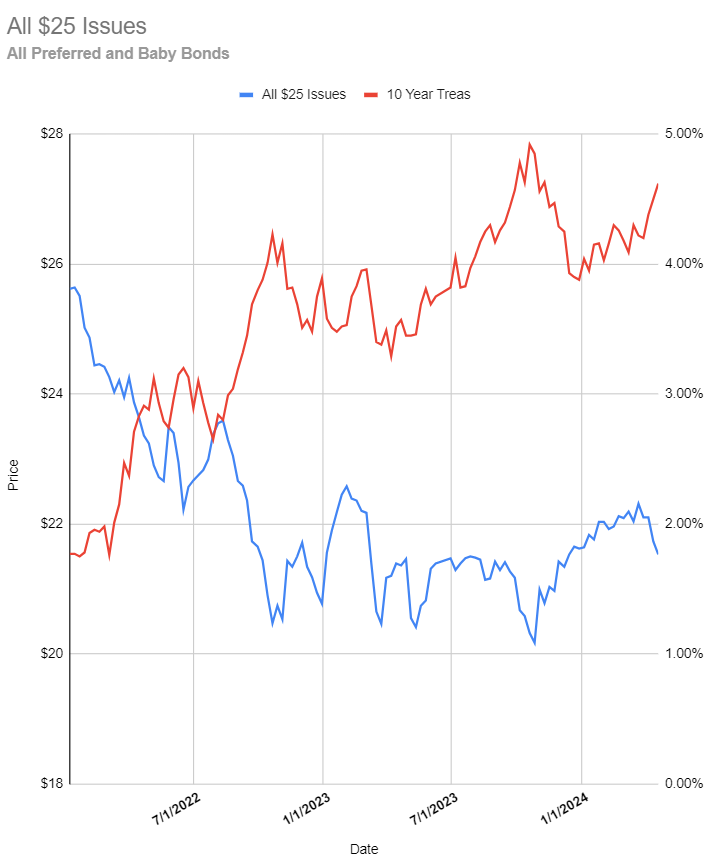

The average $25/share preferred stock an/or baby bond fell in price by 20 cents with investment grade issues rising 6 cents, banking issues fell 21 cents, CEF preferreds fell 12 cents, mREITs off 25 cents and shipping issues fell 8 cents. Very much a mixed bag for the week, but certainly in a downward trend.

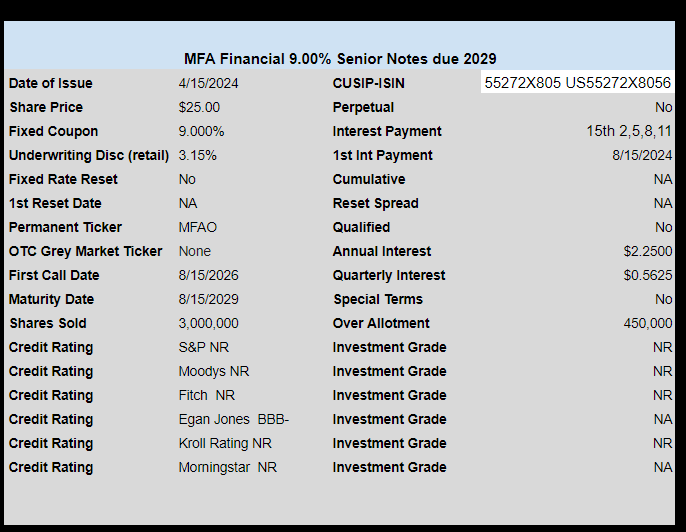

Last week we had 1 new income issue priced as MFA Financial (MFA) priced a new baby bond with a 9% coupon. It has been a while since we had an issue price at 9%–and with rates trending higher it was only a matter of time. It will be interesting to see if we see other new issues pricing this high.

Well Israel launched a very limited strike on Iran overnight. When it was first announced equity futures plunged over 50 S&P500 points (1% more or less)–but by this morning that had been reduced to 25 points as of 5:30 a.m. (central). It looks like the limited nature of the strike is welcomed–maybe it will remain limited.

Interest rates which had popped back up to 4.63% yesterday are now at 4.57% as the strike caused a modest ‘rush to safety’. Oil had spiked, but it too has calmed and is actually a bit lower this morning from yesterdays close. Who knows what will happen in the near future–no one of course.

Yesterday we had mixed economic news–unemployment claims a bit lower than expected, existing home sales lower than anticipated, but Philly Fed manufacturing much stronger than expected. Leading economic indicators (LEI) were softer than expected–again–it has fallen consistently for 2 years except for a positive number in February.

As I mentioned yesterday I planned to add a bit of a BDC baby bond to the portfolio–to add to a current position. I added to my Saratoga Investment (SAR) 8.50% baby bond (SAZ) position which has a current yield of around 8.4%. This high yield purchase balances the purchase of the RiverNorth Opportunities Fund 6% (RIV-A) A1 rated perpetual preferred. This is a very tiny move in my heavy portfolio CD weighting—no rush on this shift—maybe it takes place over the course of years (not months). With money market, treasuries and CDs available over 5% what is the rush?

No portfolio moves contemplated today for me. Next week I have bunches of CDs maturing and will be rolling most of the proceeds with a tiny bit of the proceeds shifted over to preferred stocks and/or baby bonds.

Yesterday we got a bit of a fall back just a bit—closing the day at 4.57% and now trading at 4.58%. This is a nice bit of relief for income investors as our accounts got a bit of a bounce yesterday in response. Does this mean for the weeks ahead? We have no earthy idea–we have to see data and that will start in earnest next week with the release of GDP on Thursday the 25th and the personal consumption expenditure (PCE) on Friday the 26th. With this 1-2 punch we could see interest rates move to the next higher level–OR we could see them begin to work their way back down. NO ONE knows—I think the talking heads, Fed officials and economists have all proven they don’t have a clue–nor do we.

I see crude oil has backed off 5% from the high earlier in the week–now trading around $81. I would not expect a further sell off–unless there is instant peace in the middle east and that isn’t going to happen, but we all know that further tensions are likely to arise and it could send oil way up–let’s hope this doesn’t happen. Lower prices aren’t hugely helpful to the inflation picture, BUT it certainly doesn’t hurt to pay less at the pump.

As mentioned by some folks in comments Trinity Capital (TRIN) has made a partial call (on May 17) of their 7% baby bonds (TRINL). We own this issue so will have a prorated amount called away. Everyone knew this was coming so no loss of capital will be sustained by owners–the company had stated in an earlier prospectus that they might call some of this issue. The companies partial call announcement is here.

Today I will likely take a nibble on a BDC baby bond–I’m looking for a 8% current yield (or thereabouts). I will add to a current position. Since I one bonds with 4 BDCs I see no reason to add a new company. Current holdings are on the laundry list page. Given the uncertainty in interest rates BDC baby bonds, with there shorter maturities, should provide some price stability.

This is one which I had a full position in, but because of the safety of this issue going a bit overweight is fairly comfortable for me. The issue is rated A1 by Moodys. I paid $23/share for it which gives me a current yield of over 6.50%.

Please note that safety doesn’t equal a strong share price as most of us know–but in this case I am willing to take this risk for a reasonable reward.

Of course I will add this to my ‘laundry list’ of holdings.

In a speech yesterday Fed chair Powell has tossed cold water on any realistic hope that investors have for Fed Funds rate cuts in the next couple months. Honestly finally he has come around to where he should have been all along – that you shouldn’t be implying rate cuts just ahead when the data has not been tallied. I for one am not counting on rate cuts for any investing boost–I am more inclined to worry about rate increases. I really am starting to think the only way the economy slows to any great magnitude is that we have an event (what?) that causes widespread job cuts and sends us into a recession. We’ll see–we need the data.

Yesterday markets started to stabilize a bit – interest rates held near flat – up a couple basis points at 4.65%–this morning rates are at 4.65%–steady. Today the only economic news is at 1 p.m. (central) and that is the release of the ‘beige book’–so maybe markets will be steady to up a bit today.

I see that little ($5 billion in assets) bank CNB Financial (CCNE) released earnings for the quarter ending 3/31/2024 yesterday. CCNE has a 7.125% perpetual preferred outstanding (CCNEP) outstanding–now trading at $22.82 for a current yield of 7.81%. I skimmed over the earnings release and while I didn’t see anything startling I am able to come up with a long list of ‘what ifs’ on the negative side. I watch these small banks because they have potential to have preferreds at bargain prices–but I want a higher current yield to cover the risk. For instance these small banks still have high levels of non-interest earning deposits–for CCNE it is over $700 million. These assets are those that can move in a microsecond in a bank run. Commercial loan write downs are relatively small (so far), but with ‘higher for longer’ the risks continue to escalate on the commercial side. Anyway there is no way to predict the future, so for now I am holding on the repurchase of small bank preferreds.

Yesterday I took a tiny nibble on the RiverNorth Opportunities Fund 6% perpetual (RIV-A) at $23.00/share. The current yield of 6.52% is lucrative for a A1 Moodys rated CEF preferred. I was overweight this security and obviously am now more overweight and will not buy more of this one. I continue to look!!

So we have had almost 2 months where interest rates have been trending higher—the last time we had the 10 year treasury under 4% was back on 2/2/2024—from there it has been a constant push higher. During that time frame economic news has not been friendly to rates as jobs have held up well, retail sales have grown at a rate above expectations and inflation numbers have held at or even above expectations.

The Fed continues to hint at rate cuts—which in my opinion was a major mistake. It makes no sense to promise (or near promise) rate cuts without seeing the ‘data’—last I knew they claimed to be ‘data dependent’ which obviously they can’t be if they are promising rate cuts somewhere in the months ahead.

As always we, as investors, have to use our thinking–what am I seeing and what logical conclusion does my thinking lead me to relative to investing?

So now, I see no reason for the Fed to cut rates–the data taken as a whole does not warrant a cut. This morning we got a housing starts number that came in soft–down 14% month over month which translates into a shortfall of over 200,000 units. While this is a soft number it moves a lot from month to month and 1 month doesn’t make a trend.

We have seen quality, low coupon, perpetual preferreds, and very long-dated maturity (out 30 or 40 years) baby bonds move sharply lower as rates have shot higher. Does one buy? It seems logical to me that with competitive rates in the money markets, CDs, and short maturity treasuries at 5% or higher that it makes little sense to be a buyer–but on the other hand if one is an investor looking for solid income (less concerned with capital levels) maybe it is a good time to buy–at least some nibbling. So everyone is different–every single one of us.

I am looking only at positions I currently hold for any possible small nibbles—as shown on my laundry list of holdings. I am looking for safety today–so will possibly take a nibble or two on a CEF preferred. I would consider a term preferred at the right price–although I am loaded pretty heavily with term preferred already. We’ll see what the day holds (or maybe a week)–not desperate to do anything–but would take a nibble on a perceived bargain.