Well we had a week with some important economic news last week–but Jay Powell and the FOMC news was good news–at least equity markets took it as good news.

The S&P500 moved up on the week by a solid 2.3% from the close the previous Friday. Investors took the news from the FOMC to imply 3 rate cuts yet to come this year—as always we’ll see–no one, including Fed folks, can know what with any certainty what will occur yet this year.

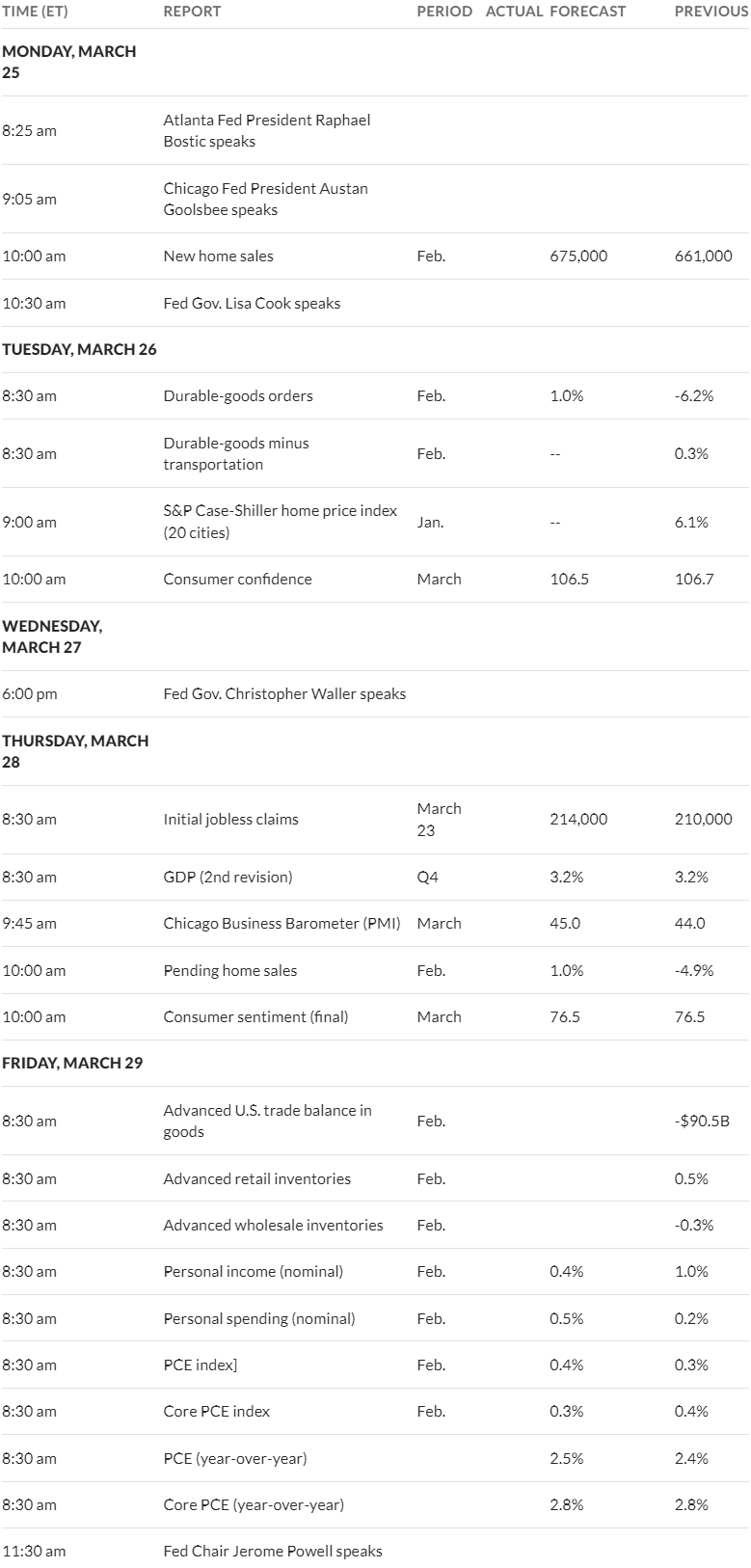

The 10 year treasury closed the week at 4.22% which was down 8 basis points from the Friday before. The yield moved in a 12 basis point range on the week–4.20% to 4.32% which all things considered is a pretty tight range. This week as always there is plenty of economic news, but the biggie for the week will be the personal consumption expenditures (PCE) which will be released on Friday. Also now that the FOMC meeting has been held we will have Fed yakkers during the week so one of them could ‘throw a bomb’ of some sort.

The Federal Reserve balance sheet assets fell by $27 billion–which is a continuation of the $95 billion monthly runoff.

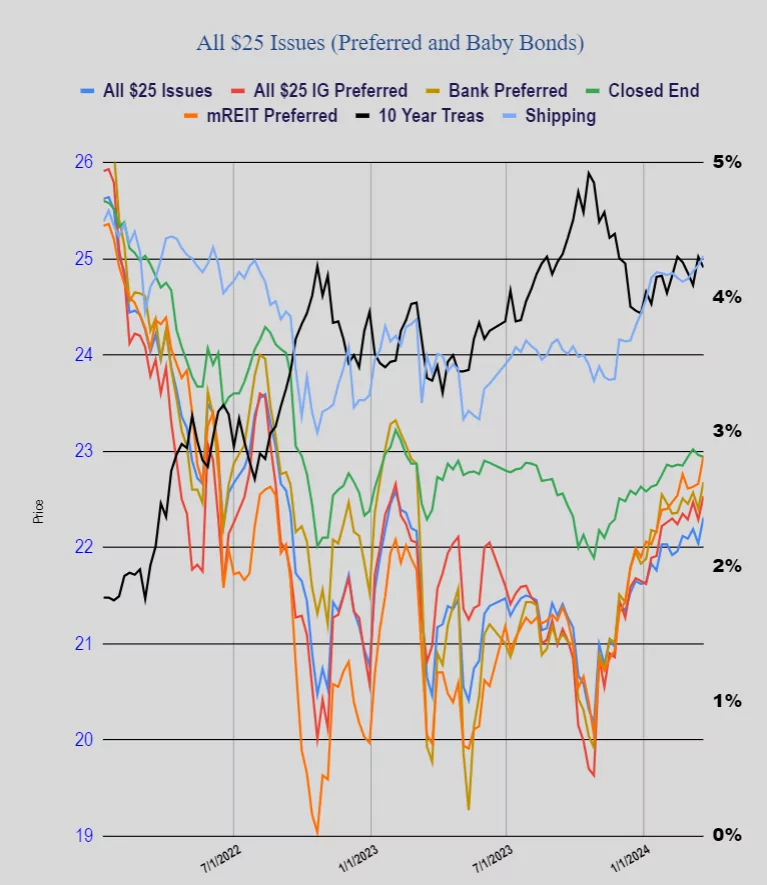

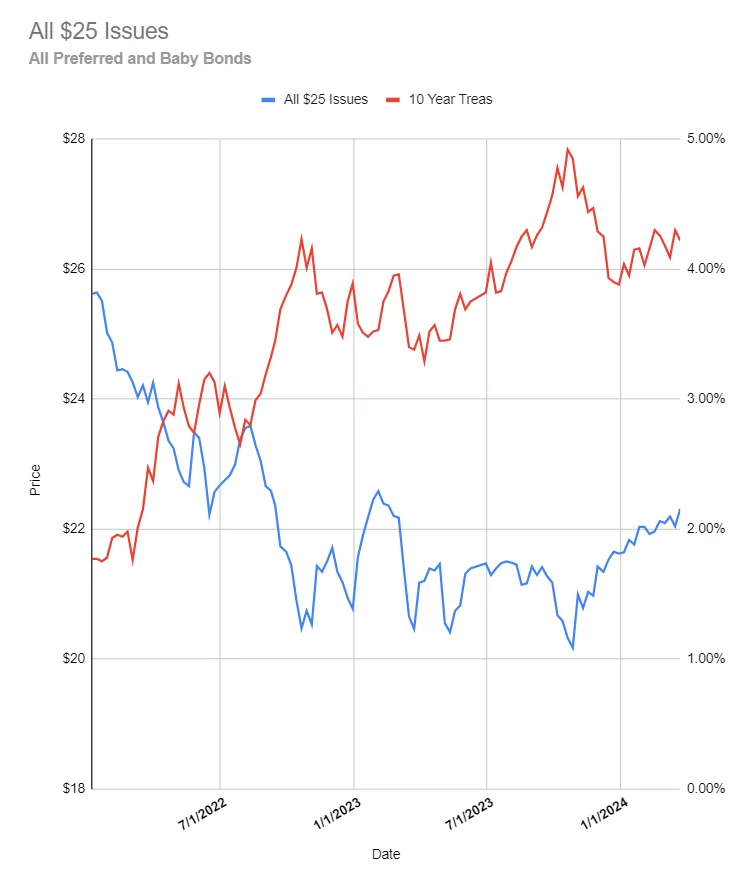

Last week was a surprisingly strong week for $25/share preferred stock and baby bonds. The average share price moved higher by 27 cents–I am fairly certain this gain was affected by the large number of ex-dividends the previous Friday—shares bounced up after being ‘marked down’ the previous Friday. Investment grade issues bounced 26 cents, banks moved up 28 cents, mREITS by 32 cents, shippers were higher by a dime. A very nice week for income investors.

Last week we had 1 new issue price as Brookfield BRP priced a new perpetual subordinated note at 7.25%.

rk160:

Speaking of ETFs, the monster $15B preferred ETF PFF received nearly $300M in inflows just in the last 10 days. That ETF has received almost $700M in inflows YTD.

Investors just can’t get enough of preferreds right now. PFF also has nearly $400M in cash (a very high number for them), so the end of this week with the quarterly rebalance and all that cash could be real whacky.

Hold onto you britches!

Is that the cause or effect of the newfound relationship between 10 Yr and Preferred shown above. Not inverse since the beginning of this year?

PCE and the rest being released on Good Friday when the stock and bond markets will be closed, that seems unusual but I guess it happens.

Also, that means that Thursday will be the etf end of month/quarter rebalancing day.