The S&P600 fell last week in a holiday shortened trading week last week–by about 1.5%.. Honestly not a hugely wild week, but the level of volatility in the marketplace is far from over as we still have tariff issues to deal with, then we have lots of budget issues to deal with. Then we have potential fireworks being caused by the administrations differences with the Federal Reserve over interest rates–and the independence of the Fed.

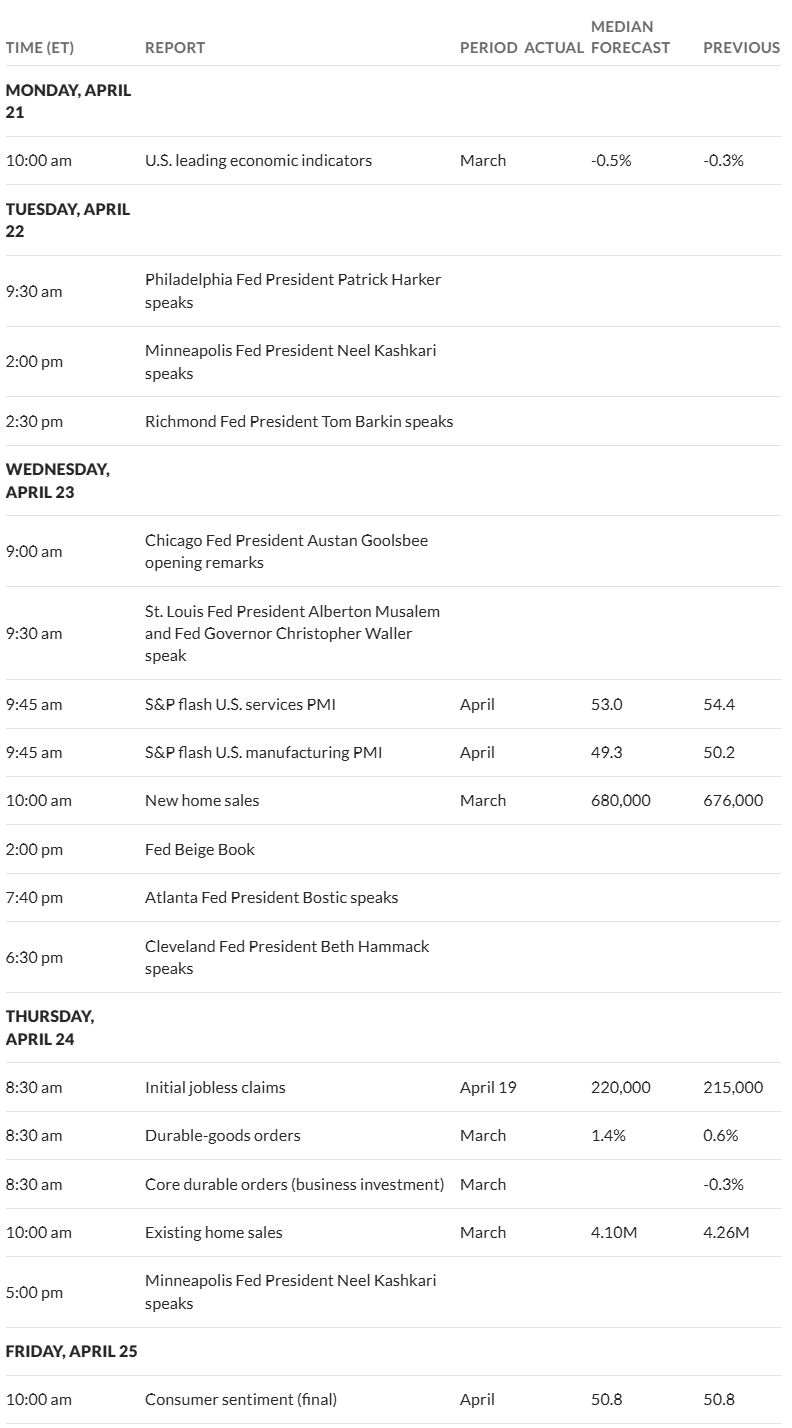

The 10 year Treasury closed the week at 4.33% which was 16 basis points lower than the closing treasury yield the previous week. The economic news last week was not of major importance and for the coming week we don’t have news that has historically been given a lot of importance, but in the current environment each piece of data is being scrutinized very closely and one can’t predict when news of a minor nature previously is assigned a high level of significance. Leading economic indicators is released today with the purchasing managers index (PMI) and durable goods orders later in the week have not been important in the past to markets–but now? We do have consumer sentiment being released on Friday–and personally I think this is an important indicator given that the consumer drives the economy. We’ll see.

The Fed balance sheet was basically flat last week. You can certainly see that the run-off has slowed and in theory this should be slightly supportive of somewhat reduced pressure on interest rates.

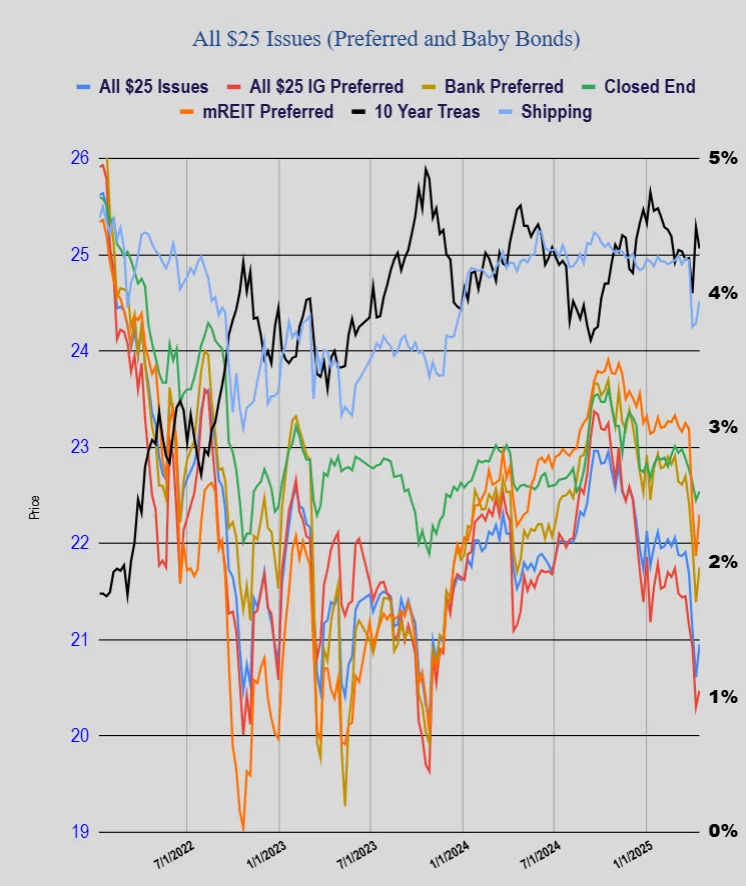

For a change we had the average $25/share preferred stock and baby bond move higher in price last week by 34 cents. Investment grade issues were up 17 cents, banking issues higher by 36 cents, CEF issues 8 cents higher, mREIT issues higher by 43 cents and shippers were 23 cents higher.

As we look at economic data, there are some “sleepers” coming.

Interesting article in the NY Time today about how student loans have come roaring back as a challenge to a lot of borrowers, and how the default rate is expected to skyrocket.

https://archive.ph/5kJSH

Of course, we taxpayers will get his with most of the default cost and that will presumably impact the federal budget/debt.

Oh the joy of “interesting times”

A couple of ideas for you to look at. I already own both in a big way. 1. RF+F is quoted at $24.14. Its a 6.95% coupon & not callable till 9/15/2029. 2. AGM+E is quoted at $21.89. Its a 5.75% coupon & callable in July of 2025. I say if they call it thats FANTASTIC as you get a ton of capital appreciation in addition to the coupon.

S&P 600, inflation is a hell of a drug. (Couldn’t resist).

You haven’t mentioned when the struggle to sack Powell really gets underway and ends of course with SCOTUS giving Trump the right to sack him. 2500-3000 on the S&P?

That’s my biggest concern by an order of magnitude- wondering if the markets, treasuries, US dollar, and any confidence in the US govt & monetary system will ever recover. Control of the govt and SCOTUS would have to flip completely.

It appears to have already started based on Trump’s comments over the past few days and the market’s and dollar’s reaction today.

Or Powell could get off his cushion and cut the rates…there’s really no justification for the delay. The ECB has cut rates seven times since last summer without a problem.

Powell is waiting for labor market weakness, as stated. Good idea? Labor market data is lagging. There is no chorus of FOMC members calling for rate cuts, so it’s not just Powell.

What part of the economy would function better with lower rates at the front end? Aren’t tariffs on China the big threat to small business? Can rate cuts fix that? And should they be used to counteract possibly misguided fiscal policy? If inflation picks up in the coming months (and who can say?), would that justify not cutting now?

I have to believe Fed governors are actively discussing rate cuts in private. They can’t say that publicly because markets will assume it’s going to happen.

When the Fed cut rates 0.5% in Sept 2024 CPI was 2.5%, the GDP was growing at 3.1 % and unemployment was 4.2%. Their rationale then was it was a proactive move to prevent a broader economic downturn.

April 2025…CPI is 2.4%, GDP is now only 2.3% and unemployment is 4.2%.

There is really no excuse for the Fed to keep rates where they are if the conditions under which they cut last time are the same or worse than before!

Citadel-

Does the Fed judge inflation by CPI? The target is 2%…not there yet. The Fed sees tariffs as an inflation threat. The Fed is aware of slowing growth. Growth is not one of its mandates. We all have opinions on what the Fed should do. If you want to know what they will do, then look at the world as they do.

The Fed is owned by its banks. Its unstated #1 mandate is to protect the banks and the functioning of the financial system.

With the tariffs beginning to hit soon it’s entirely possible we see a big bump in prices. They aren’t going to cut rates into oncoming inflation.