The wild ride continues in the equity markets–and will likely continue all through the current week with the tariff uncertainty being front and center. The S&P500 moved higher last week by 5.6%–it didn’t feel like a big up week to me probably because I focus on interest rates which are remaining stuck at fairly high levels.

The 10 year Treasury closed the week at 4.49% which was a massive 50 basis points above the 3.98% close from the previous week. We had a number of treasury auctions last week and they all came off fairly good–just maybe at these higher rates there are buyers for our debt. We’ll see what kind of news comes out of the administration on the tariff front and whether we can get interest rates under control. At this moment (Monday 6 am) the 10 year Treasury is trading at 4.44%.

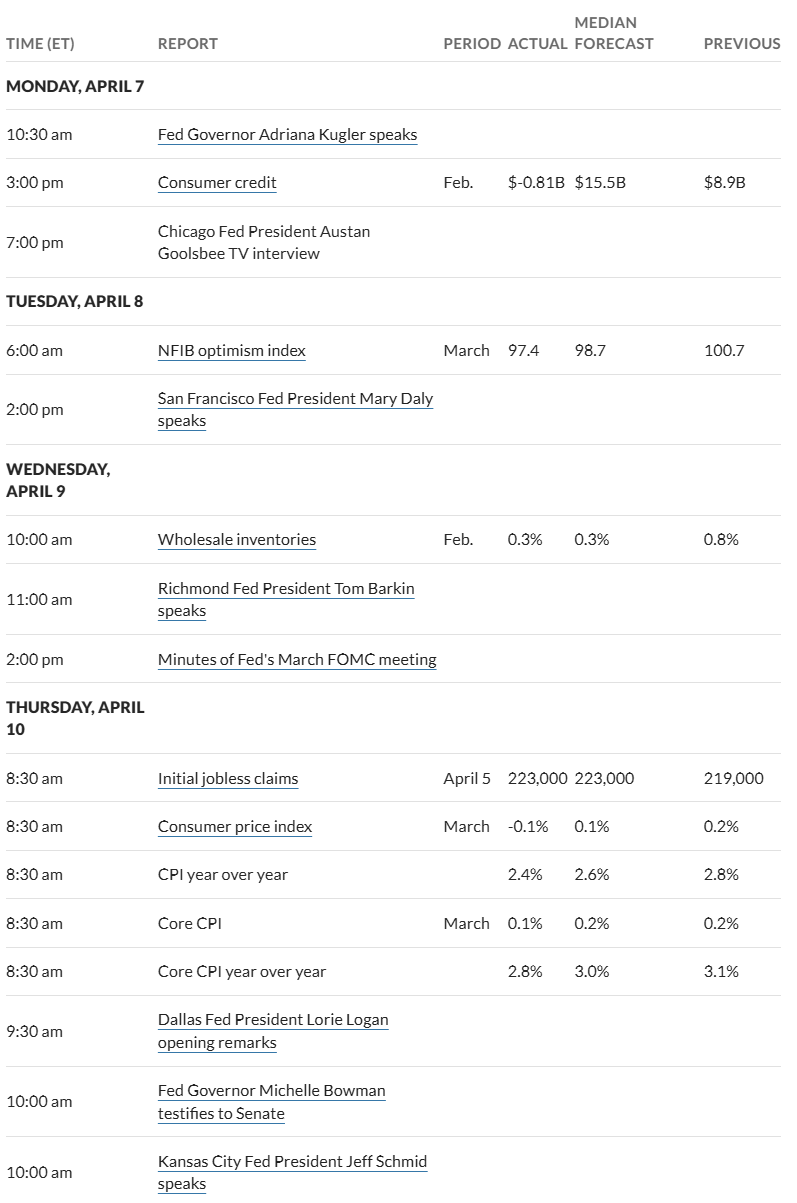

Last week had both consumer prices (CPI) and producer prices (PPI) announced and both came in fairly soft, but neither announcement moved interest rates lower and the numbers were perceived as ‘old news’–before tariffs start hitting.

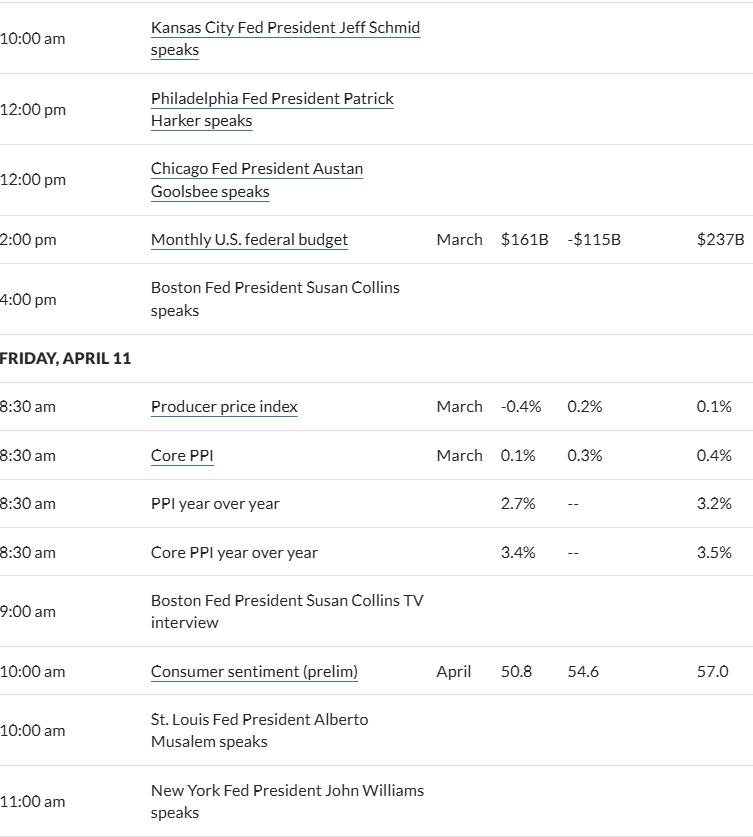

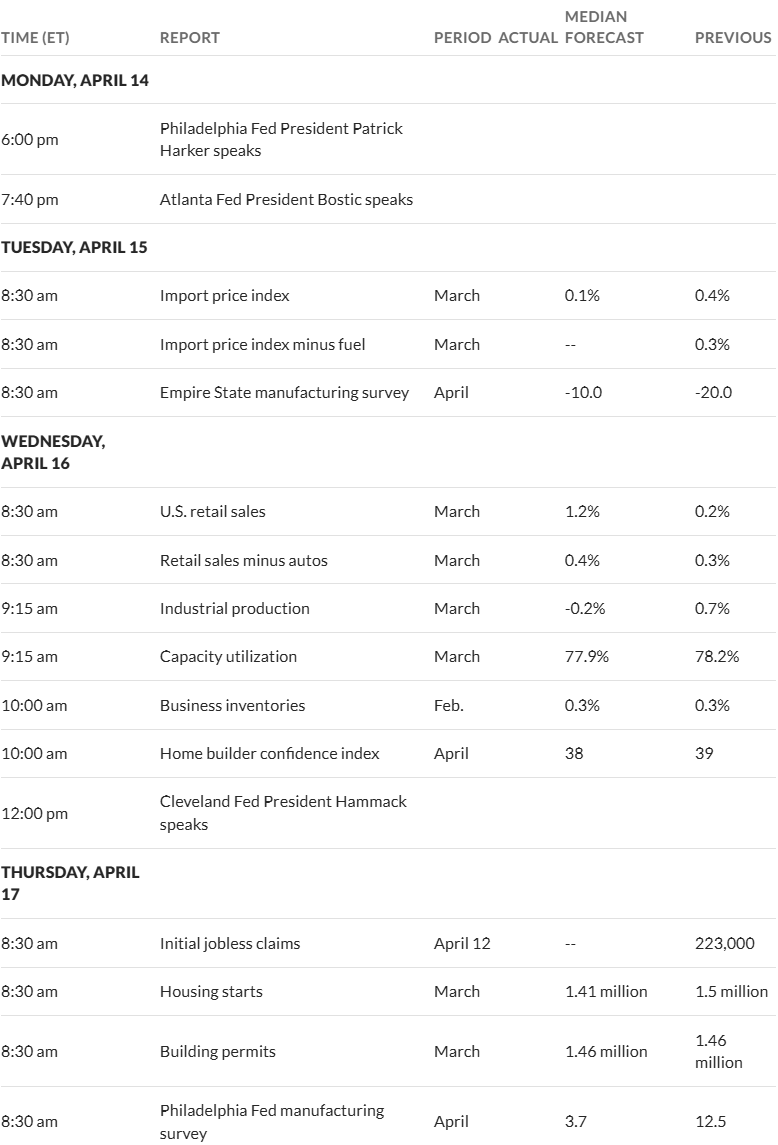

This week we have none of the most important economic news being released, although we have retail sales being announced on Wednesday–but it is old news being from March. Maybe we will see strong sales as folks moved to make purchases ahead of tariffs.

Another item to note is that mortgage interest rates took a large jump last week which without doubt when coupled with consumer sentiment falling will hurt the housing market if these high rates remain in place for long. Housing is one of the most important numbers I watch after inflation and employment as an indicate of future economic health.

The Fed reserve balance sheet rose by $4 billion last week–a bounce that occurs about once a month as the Fed continues to runoff their assets–now at the reduced runoff rate of $40 billion a month– of which $5 billion is treasuries with $35 billion being Mortgage securities.

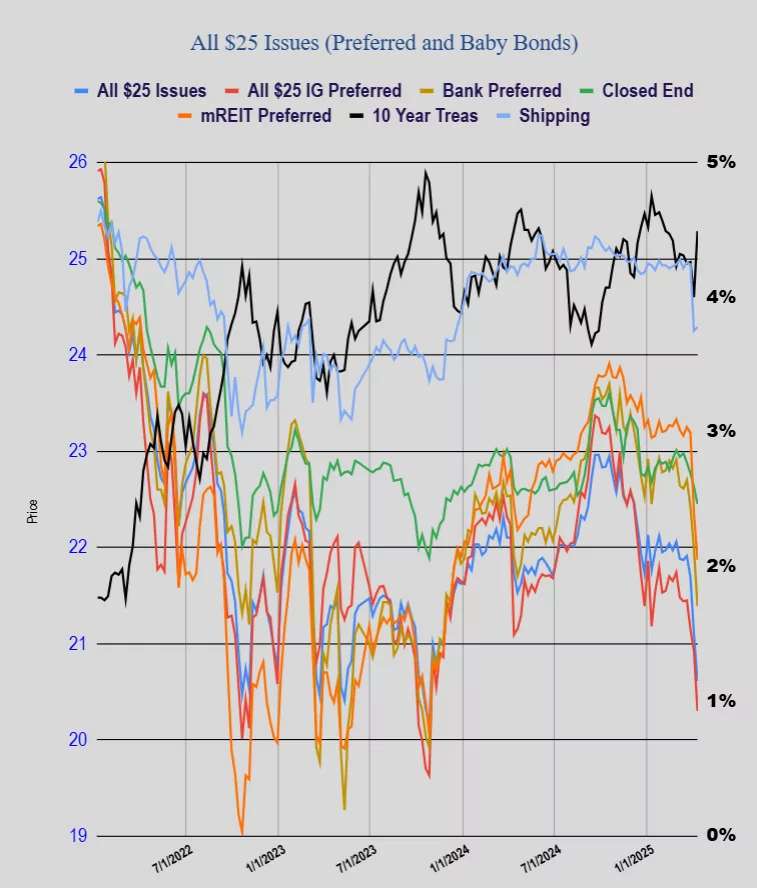

The average $25/share preferred stock and baby bond price took a shellacking last week with the average share falling by 49 cents. Investment grade issues fell 62 cents, banking issues fell 58 cents, CEF preferreds fell 18 cents, mREIT preferreds fell 48 cents and shippers actually rose by 4 cents.

What is everybody’s thoughts on MS+Q now trading at $25.10 ?? Seems like a pretty solid company & a pretty decent price with great call protection out to 10/15/2029. Coupon is a nice 6.625%. For those of you that are just building “Income Streams” for the rest of your life it seems to me that right now there are lots of bargains to be had.

Maybe a better idea Chuck is Morgan Stanley fixed the rates on all their floating preferred, so the MS-PE is about the same cost but is now fixed at 7.125% or do a mix of the two.

Another idea is MS.PRO & MS.PRL that are fixed with low coupons so maybe they will be the last to be redeemed and if they do their will be the cap gain. Maybe they won’t call anything for awhile with the way treasuries are being dumped and then it would make sense to have the higher yield 7%+ as Charles mentions with the E series.

I’ve been after these types lately WBS.PRG, WBS.PRF, MS.PRK (there is a website where MS lists all of the issues that were supposed to float but are instead fixed. One of our III peers had posted it), BAC.PRN, BAC.PRK, JPM.PRL

It would probably make sense to look at which companies have a history of calling issues and what their WACC is if it can be found.

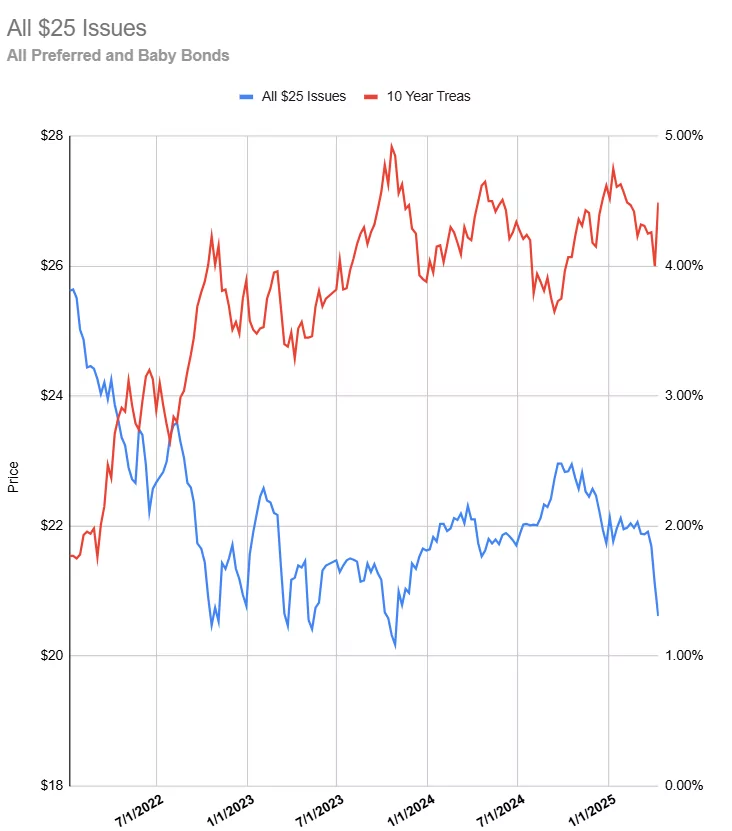

Tim, I like your simple chart on all $25.00 issues compared to the price of treasuries. The correlation of higher and lower yields of the treasuries to the rise and fall of the $25 issues is well shown.

As prices on the $25 issues drop, the yields go up. In a way this matches Treasury yields going up.

As a guess the spread to BBB- rated issues to T-bills is about 3%, we may get back to that 7% to 8% yield you were looking for last year.

The million dollar question is if the economy was doing ok last year then what are these Preferred and Baby bonds going to do if we slip into a recession or worse? Some, especially the REIT preferred are already at the lows I bought in 2023 and 2024 when there was the panic that REIT’s were walking away from properties and turning over the keys to banks because the income and value of the properties wasn’t worth what was owed on loans and it made no sense refinancing them. The banks that extended loans and pushed them out could still see problems.

Charles

Suggest keeping an eye on the link below for 1/2 of the answer to your question.

https://fred.stlouisfed.org/series/BAMLH0A0HYM2

Our pref yields will be directly impacted by the 10T rate PLUS the risk spread.

We all need to take into account what we expect the future to be for each one in determining our buys/sells

Westie, your guess is welcome.

is welcome.

I think you pointed out earlier T-bill auctions are still healthy, but I didn’t know some bidders are required to bid.

Just my uneducated guess not having a banking background is we may not see a steady climb in rates but certainly we will see spikes. On again and off again Tariffs just as one example. The general impression I am getting is the US is not to be trusted so why buy our debt or invest here unless the reward is worth the risk. Hence my guess we will higher spikes in rates.

I sold a couple things today and the last few days. A CEF equity fund, a REIT preferred at 5.25% paying 6.5% on cost that just went ex-dividend, Also a pharmaceutical common paying 4.8% on cost and a food company common yielding 3.3% on cost.

All of these had blow outs and went lower than what I had paid for them this past week. I broke even on some and pocketed capitol plus divy’s on others.

I also sold an energy stock at a loss but collected a divy and I sold a pipeline company at a capital gain plus dividends.

I expect oil demand to decline and overseas producers to flood the market with oil and gas. That’s a bad combination for energy stocks.

As I said at the beginning, I expect more volatility in this market and the opportunity to buy some of these back at lower prices.

I’m pessimistic about the direction of long rates. I fear we are going into a stagflationary scenario with rates going up and our perpetuals getting bombed as long bonds will offer a real alternative at less credit risk. I’m reducing exposure to all types of preferred (other than terms) even taking a loss on some.

This could be and is the biggest risk of locking in perpetual fixed rate issues. The less desirable the world finds US treasuries, the more pain we’ll feel in watching our yield on cost sit below market level of 10T + risk.

I’m taking some bites though. Tim’s move of term preferreds is solid.

Could also mix in some strong dividend growth commons and those can help with inflation and yield on cost should improve each year. Just my personal take.