What a week! The S&P500 lifted off on Tuesday and never locked back all week long. The index closed up 4.7% on the week and now is at all time highs.

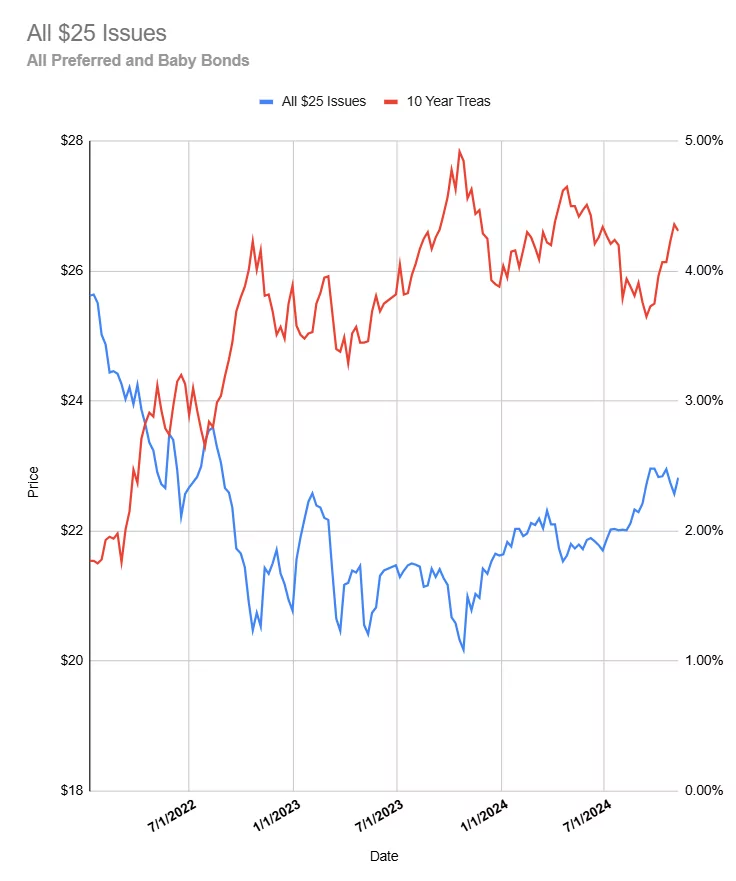

The 10 year treasury backed off from the high of the week of 4.47% all the way back down to a close Friday of 4.30%. We will have to see if the late week rally in bonds was simply a bounce or if there is more upside to bond pricing. We will have to wait another day to find out as the bond market is closed on Monday for Veterans Day.

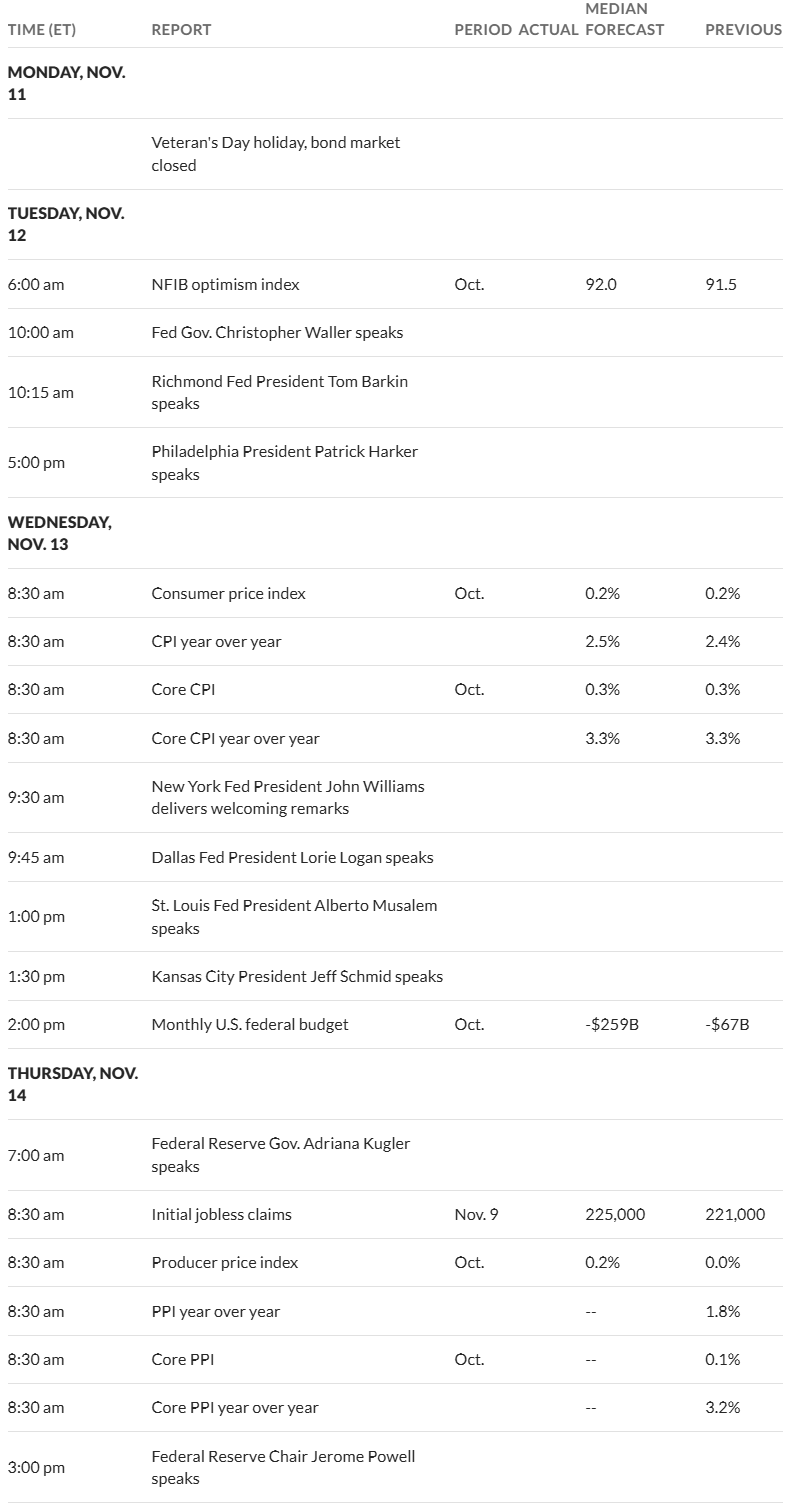

This week we will have a continuation of economic news (it never ever stops) when we have the CPI being released on Wednesday and PPI released on Thursday. The we will have retail sales released on Friday. The case for a December rate cut (or pause) will be being built. Right now the expectations remain for a December rate cut of another 1/4%–we will have to wait and see if the data backs this expectation or if we get a pause.

The Federal Reserve balance sheet finally reached $6.99 trillion with a fall of $14 billion last week–this 1st time under $7 trillion July 2020.

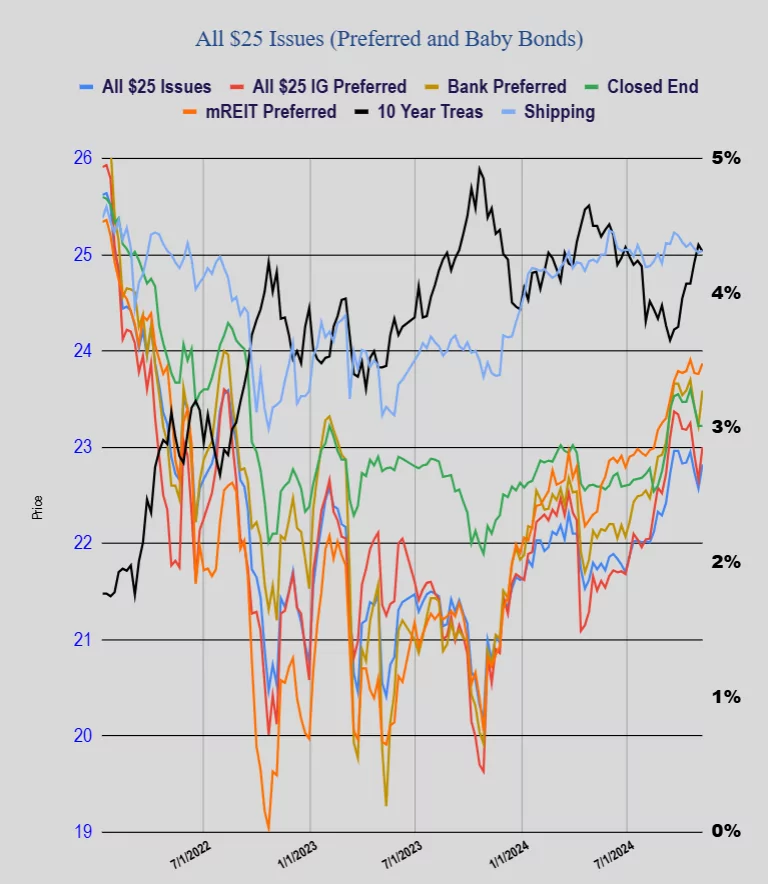

The average $25/share preferred or baby bond moved higher last week for the 1st time in 3 weeks–share prices moved up by 25 cents. Investment grade issues moved up by 33 cents, banks moved 27 cents while the lower quality issues moved less. mREITs moved 11 cents higher while shippers moved up 2 cents.

Happy Veterans Day to all of my fellow Vets…