Time to close out the month of September today and move into what has historically been a rough month for stocks. One would be quite foolish to think this is really meaningful right now—folks are bullish and there continues to be more than enough ‘dry powder’ to make each set back a buying opportunity for the bulls. Every day we have maturities of fixed income products where decisions have to be made by investors whether to deploy into equities or accept 50 or 100 basis points less coupon by rolling their CDs. Additionally each day money market funds will tick down a bit in return as short maturity treasuries mature and the fund has to accept a lower return–today you can still get 5.xx% in a money market, but very soon you will have to accept something in the

Last week we saw equities move higher—barely. The S&P500 moved higher by 63 basis points–not large, but at this point after significant gains one shouldn’t be too greedy.

The 10 year treasury was pretty darned steady on the week–closing on Friday at 3.75% after moving in a range of 3.73% to 3.82% all week. It is pretty rare to have a week moved in just a 9 basis point range–in particular with news such as the personal consumption expenditures (PCE) inflation numbers. With the PCE inflation numbers being friendly to interest rates one would have thought we might have seen a bigger drop in the 10 year yield on Friday–but we didn’t get it–just down 4 basis points lower than the Thursday close.

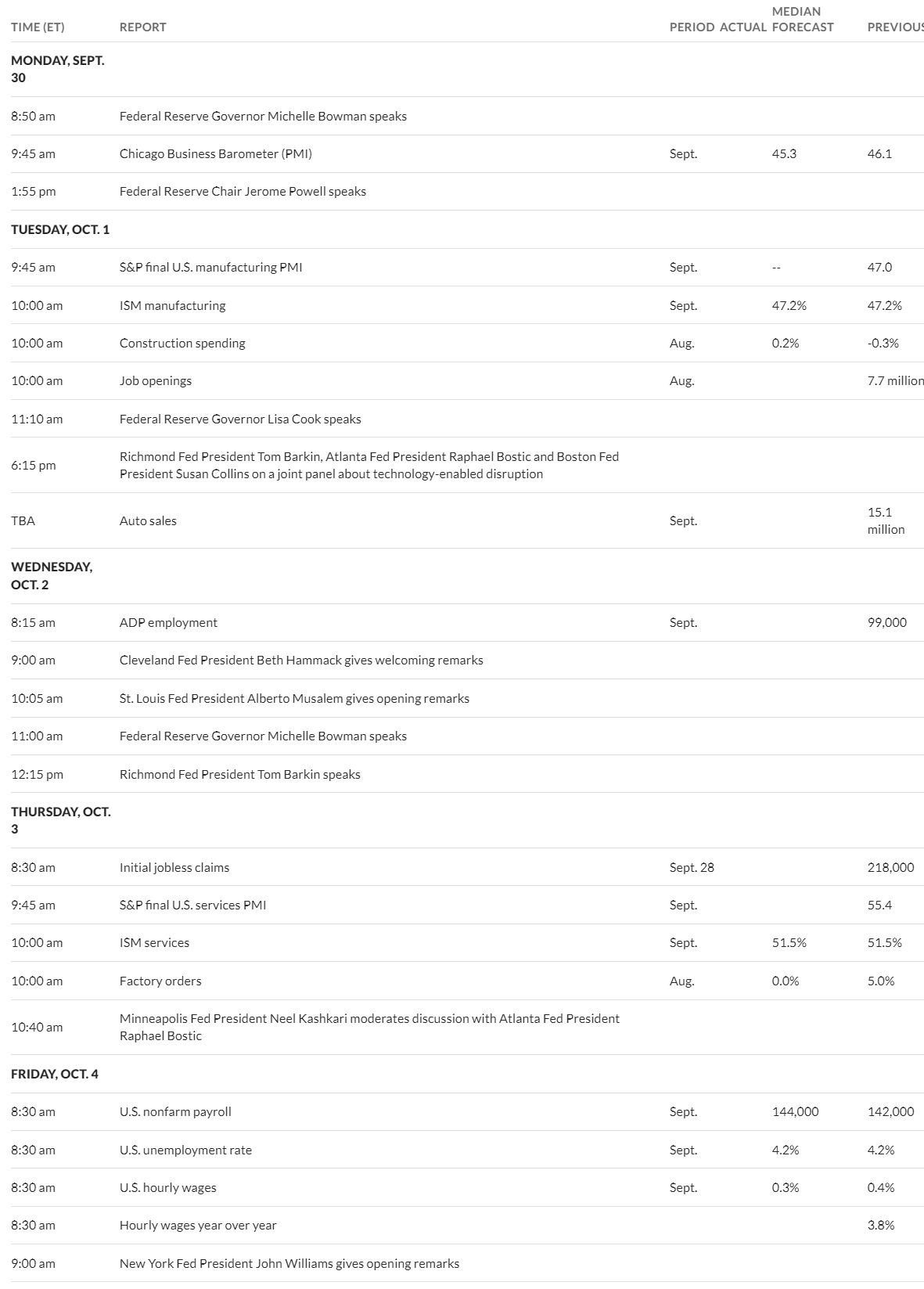

This week brings another important number in the employment numbers on Friday (the ‘official’ government numbers)–preceded by the ADP employment numbers on Wednesday. We have other bits of economic news and Fed yakkers, but if it isn’t an inflation number, an employment number, or a 1st read on GDP it isn’t meaningful to this market.

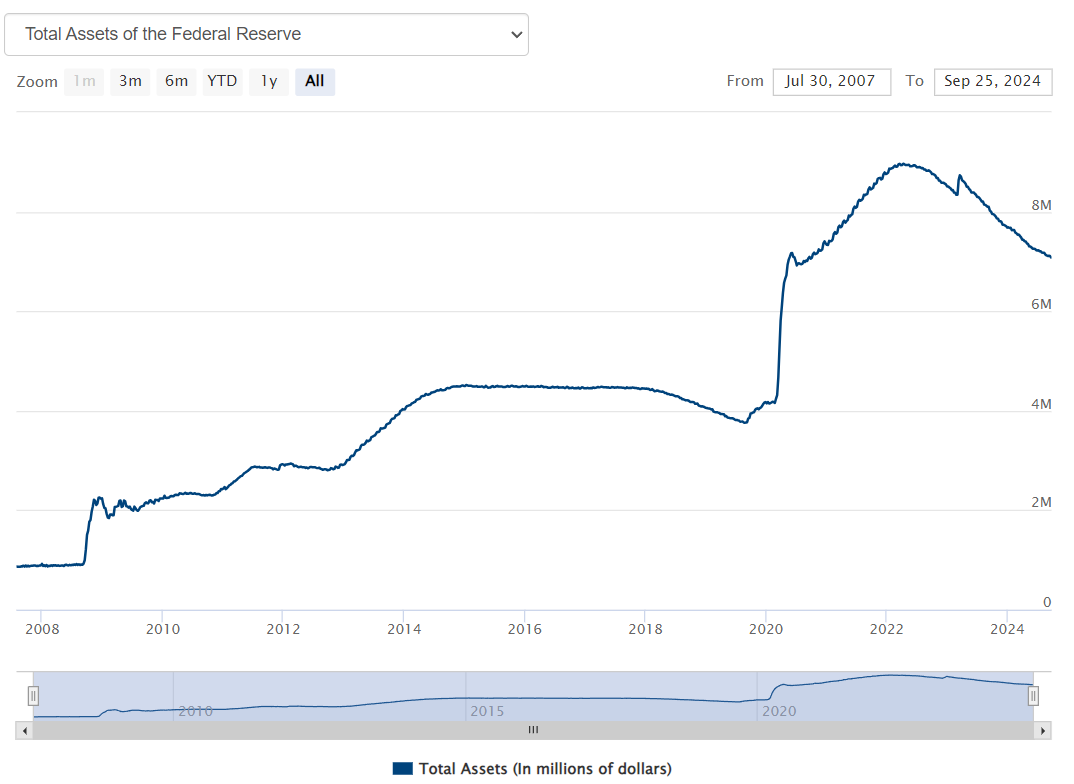

The Federal Reserve balance sheet assets took a nice sized tumble last week–down by $29 billion. The direction is correct but obviously there is a very long ways to go to get back to the time before the financial crisis in 2008-2009.

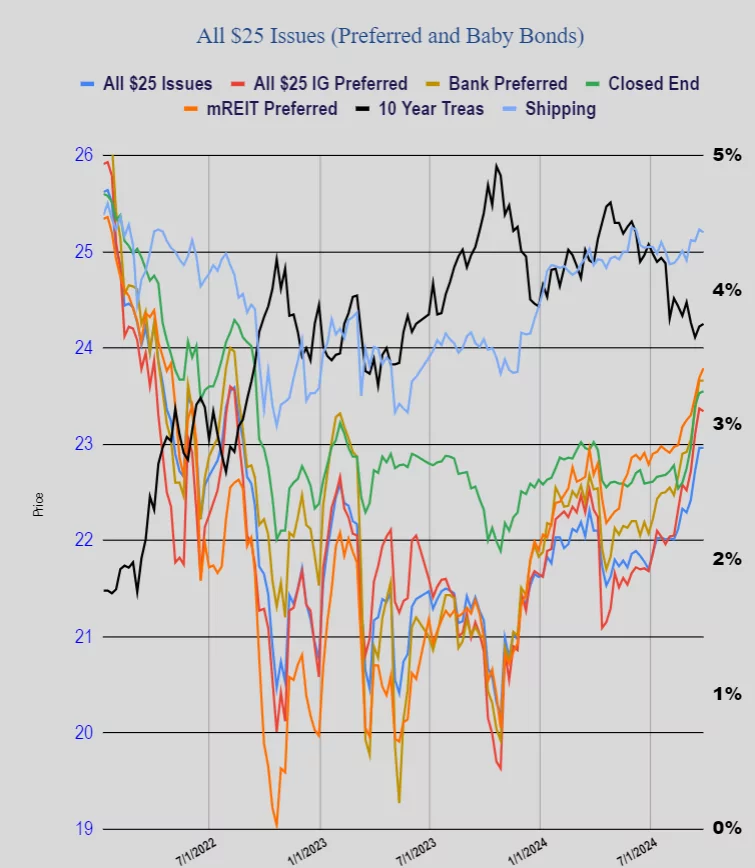

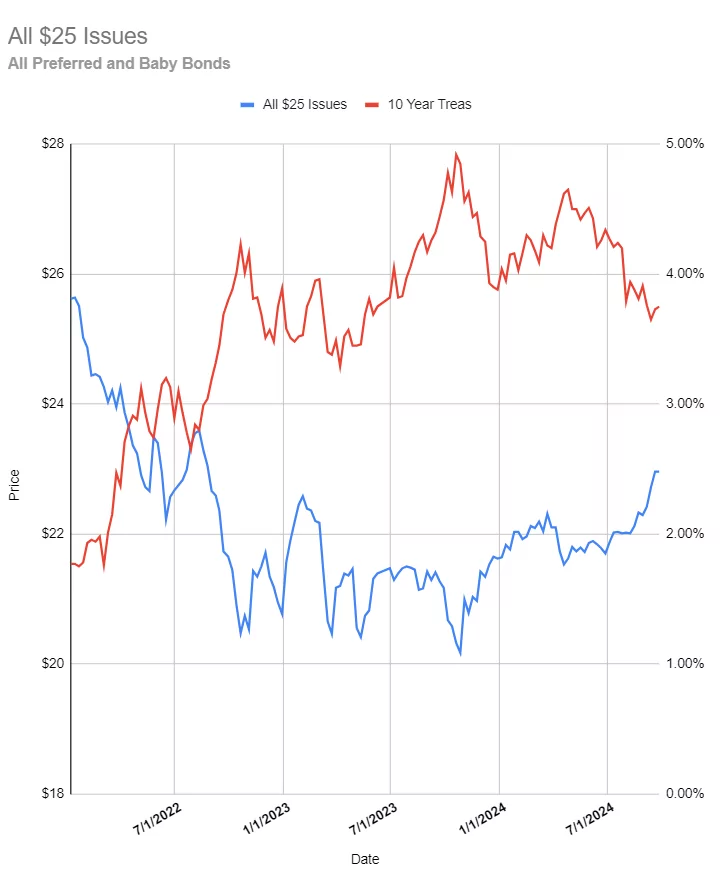

Last week was extremely quiet in income issues as the average $25/share preferred and baby bond was dead flat–no movement. Investment grade issues fell by 3 cents, banks didn’t move any, mREIT preferreds up a dime and shippers fell by 3 cents.

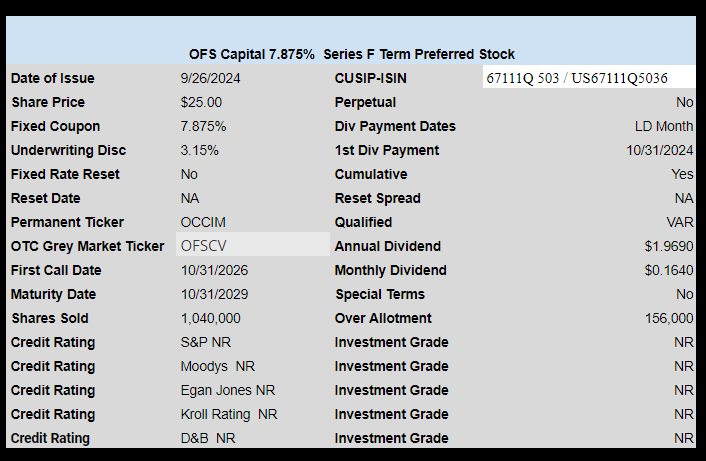

Last week we had 1 new income issue price as closed end fund OFS Credit Company (OCCI) priced a new issue of monthly paying term preferred with a coupon of 7.875%.

I was listening to Powell who confidently confirmed the strength of the economy and the easing of supply bottlenecks. No mention of port strikes will rain on the bull’s parade this week, maybe ours too.

I have huge chunks of treasuries coming due in the next 3 months, the first batch tonight. I guess I’ll take more dregs of bank preferreds and PSAs.

Hi Tim,

looks like your first paragraph got truncated.

The likely floor for Fed Balance sheet is $5T – $6T given the growth in currency in circulation, reserves, and now including the treasury’s ‘checking account’. (The treasury’s account moving from a bank to the Fed was due to the financial crisis).

Vix moving up the past week. Does it matter?

Charles – never mind the VIX. How about this 2%+ inflation environment?

I just got hit with a 12.4% increase in my healthcare insurance premiums for 2025, and an 8% increase in auto insurance premiums. On November 1st, my 80-year old mother will get blasted with an 8.2% increase in the monthly rental costs at her senior living community. Too bad her social security income is likely to go up less than 3%.

But hey, I can buy one of those Chinese-made washing machines that comes with a GE logo a little cheaper than last year.

Ain’t 2% inflation just grand?

Doc, no disagreement here. Basically you are a captive audience when it comes to necessities and the providers of a product can charge you whatever they want. With commodities like a car or washing machine the manufacturer can produce it wherever they can make the best margin but they are subject to limits on price increases because of competition. But then we are the ones supporting this system because we want to pay less.

Hey you hear about the upcoming dock workers strike? They don’t want more automation and say they are not being paid enough.

BTY, China is already shipping to Mexican ports and then trucking imports into the US.

That’s one way to get illegal drugs & or components into Mexico & the US.