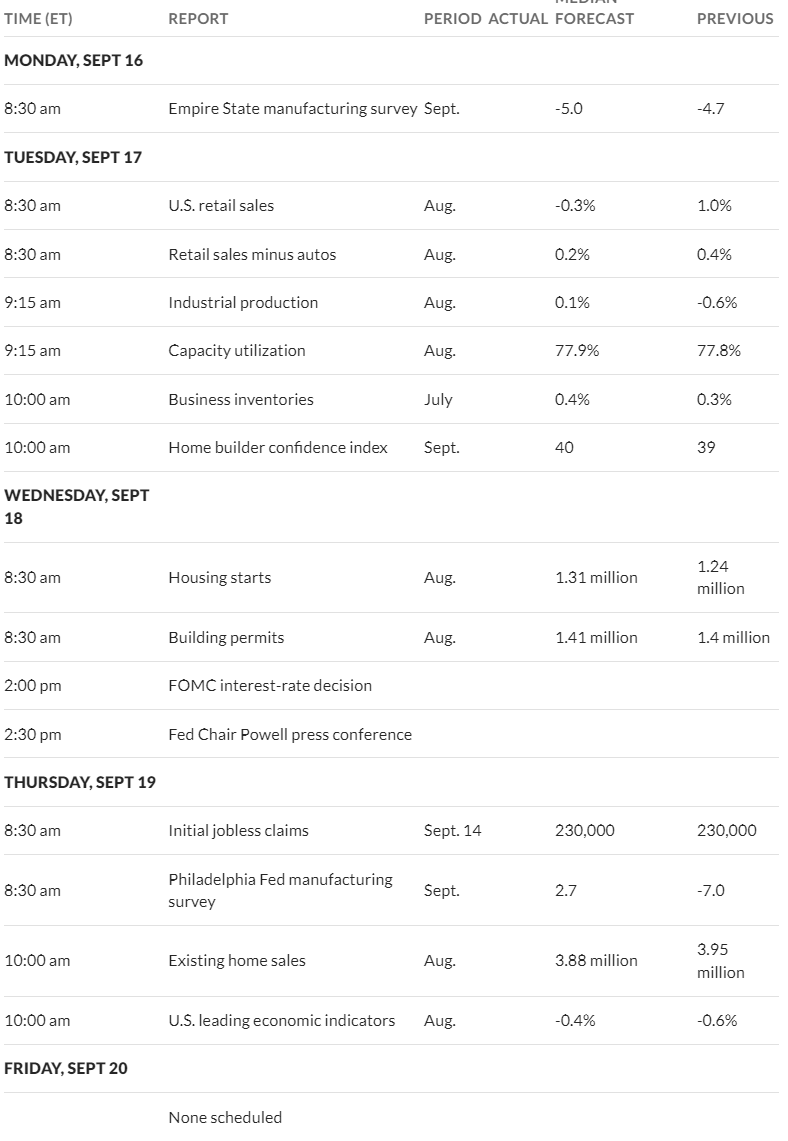

Well another big gain on the week for the S&P500 last week–with the index moving 4% higher. One has to wonder if we see the index setback this week in a ‘sell the news’ week on the back of a highly anticipated fed funds interest rate cut on Wednesday.

The 10 year treasury continued to drift lower closing the week at 3.65% which was 11 basis points lower than the close the previous week. The last time we saw the 10 year yield this low was the week ending 5/12/2023. One wonders how the yield will react to this weeks interest rate cut–obviously this is a very anticipated cut at some level (25 or 50 basis points?). Of course there is plenty of more minor economic news this week to go with the FOMC meeting, but most of it will be of minor concern as we got CPI, PPI, and employment in the last 10 days and those are the major market movers.

The Fed balance sheet assets position moved $3 billion higher last week–normal as we have occasional small reversals of the run-off–overall the trend lower continues.

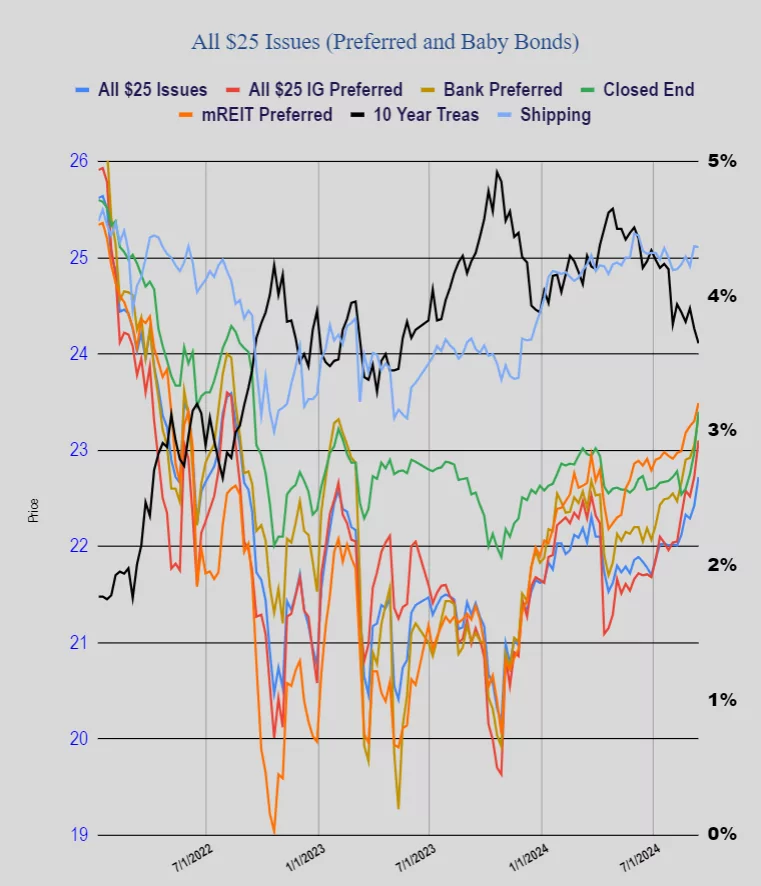

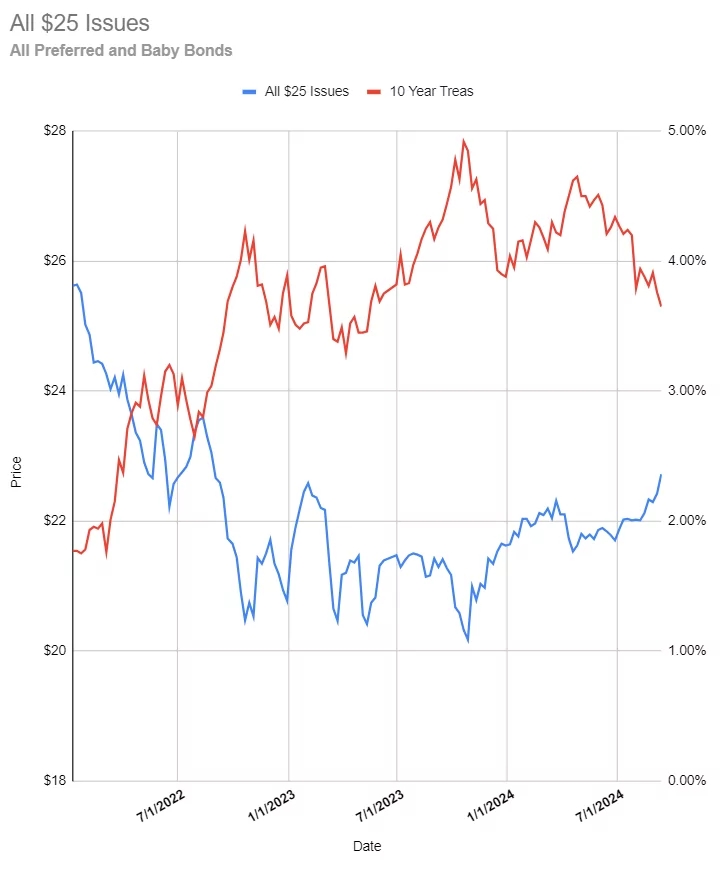

Last week the average $25/share preferred and baby bond moved sharply higher once again last week. The average share was up 30 cents–a giant move as these things go. Investment grade issues moved 38 cents higher, banks were up 30 cents, CEF issues were up 43 cents, mREIT issues were up 19 cents with shippers down 1 penny. Average prices are now at the highest level since August, 2022.

Last week we had one new income issue price with the pricing of a new Great Elm Capital (GECC) baby bond. The issue prices at 8.125%.

Big move past 48hrs with….

RIV A

Bought my second MREIT today RWTN. This one is in my high risk bucket, will see how it does.

Probably a little more risky than average. I have some RWT-A at 10% but no redemption date. I typically trade the higher yield unless the term issues are almost the same. I may sell at the upcoming ex-div if I get a good price.

BWBBP up like a bottle rocket today, up 11%, although this is on very low volume. Cannot find an explanation. Maybe someone forgot to make a iimit order?

donocash, What the ? one of the bank stocks I own. Only thing I can figure is someone is chasing yield. Another case of lower to mid dividend stocks seeing a price recovery as investors are worried or should I say scared that income returns are going to be going lower and they are rushing to lock in yield and income.

someone fat fingered a bid. Ask is only $21 so it will be coming down very soon

Sorry, should say limit order at the end.

Got some CDs maturing last week and am going to search for bargains this week. Probably going to wait after wednesday, because I want to hear Powell’s new rhetoric. There are some potential instruments I am looking at – ECC-D, ATHS and HOVNP. Last one I think is trading at 18 bucks and I think it’s destination is par. I listened to their recent transcript, the CEO said they are focused on lowering their debt-to-capital ratio and reducing their interest expense. It’s hard though without being able to have unsecured debt due to recent history but management expects that to change begining 2025 or mid 2025 . IMO with the housing shortage and the upcoming rate cuts, homebuilders are in a very good position.

yes I am long $HOVNP have a nice chunk w basis 17.95 pays 1.91/yr, I think it could ‘rerate’ from 18 to 22.50 which is about an 8.5% yield in line w most junky debt although it is certainly not that anymore. W the credit ratings upgrades this year on their debt and paydown from dangerous non compliant levels (which caused the non cum pfd divs to be suspended) I think there is decent buffer to pay pfds no sweat even in a recession. Ara Hovnanian the Chairman and son of founder has sold common into the huge stock rally from 80 to 240 but could just be planning or smart since it was near 0 in the pandemic! Bea

Yep I own HOVNP , since I dont think a C rating on S&P, is accurate.

Be a would know more about this than I do.

ok I looked at it and bought a small amount, I’ll send you the bill if it doesn’t work out, jk

HOVNP is not for the faint of heart especially the men on here with tickie tickers.. I thought it was odd in the big runup in the HOV common Ara H. was selling into the rally but he is getting older maybe just taking profits, they have been buying back common as well.. new article on SA not a bad piece by someone I don’t recognize…missed a few things imo. Hopefully Martin can read it if interested. Martin would do better article! lol. Mortgage rates coming down should help some.

I’m not an analyst I’m a numbers guy. I trade on price movement and patterns, after trying to figure out which analysts know what they are talking about. Reading comments section is sometimes a good way to gauge investor sentiment at least in the short term.

yes I appreciate that too sentiment is important or so says Avi the Gilbert..lol.. I use a combo never ignore technicals..ala Louise Yamada Gail Dudak and I guess Carter Worth today.

Bea- A bit past call.

A bit past call.

QOnline shows a 2/24 rating of CCC- for HOVNP– pretty sure I’ve never seen a junky-junk rating like that on QO.

Non-cumulative ! Sounds like they think they are a bank

well HOV got two upgrades this year of course still in the high risk ratings classes but Moody’s and S&P were ok with the substantial debt progress, of course as always DYODD https://finance.yahoo.com/news/hovnanian-enterprises-announces-credit-rating-130000259.html

today’s trades are tomorrow’s memories. Bea

BEA-

Thanks- I just thought it odd with the Co. debt getting upgrades, the p’frd was CCC- dated this Feb.

It does look they are making good progress –waiting now to see what Powell comes up with. Considering for my spec pile.

I have owned ATHS since it was issued in March and after some additions in April/May and it being a big part of my holdings, lately I have been reducing my holdings as i fail to understand why it does not trade at a higher price like other preferreds of APO like ATH-E. It cannot just be that ATH-E is QDI and ATHS is not. Also low

Anyone please try to explain?

mSquare, there is a lot of interest in yield and income right now but holdings that are out 40 years to maturity make me at least a little nervous. Could be others feel the same way especially since they were bought out by a PE company. I am not saying APO is bad, at least in my book they are better than Blackstone and Brookfield. I own it too and am ok with the risk as it trades in a certain range which is close to par.

mSquare,

I also own a large chunk of ATHS and have nibbled at more. It has a much better YTC than ATH-E (which I also own a smaller amount). I like it. Solid 7.25% until 2029. Not much else available to better it. The reset rate is not super high but you can’t win them all. Maturity date doesn’t bother me as I can dump it any time. I don’t expect much capital gain but we might see it as rates move lower. Anyway, I ain’t selling cause the market doesn’t like it. Just my 2 cents. Good luck.