Last week was a trying week for pretty much all investors—only if you were in all cash did you escape the severe losses of Thursday and Friday. I know my losses were pretty minimal on a relative basis much less than 1%–BUT what lies ahead is a total unknown. So I needed to put together of spots I might ‘shop’ depending what occurs in the coming week.

Below are all investment grade issues which have been somewhat beaten down. They are not yielding huge amounts–yet. If markets go into a tailspin and these get beaten down further I may buy–I can’t even define what that means on Sunday afternoon until we see markets open up and trade.

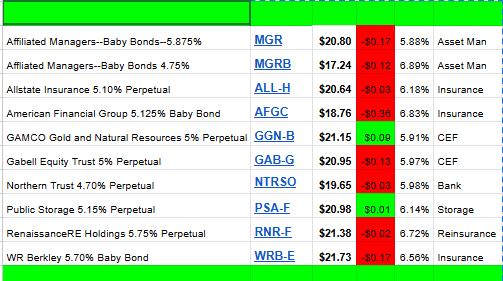

The purpose of this is to identify high quality issues that could have lots of capital gains potential if they get beaten down dramatically in the weeks ahead. This means if there IS panic selling these quality issues may bounce back nicely when the selling is over.

The spreadsheet below IS NOT LIVE—but go to this page for the live chart.

the thing to remember is – if inflation heads up, and interest rates head up (tariffs are inflationary)

then low yield quality preferreds and bonds won’t do well. They don’t pay enough + if they don’t get redeemed, you never get the face value.

Regarding the whole ‘tariffs are inflationary’ concept, I just checked the commodity futures charts and almost all of them are down significantly from a month ago. Energy, metals, lumber, grains, etc. are all pricing lower. If raw material prices keep going down with tariffs, I’m not quite sure how inflation goes up.

As was mentioned yesterday, Tariffs are inflationary but recession is deflationary. I guess a recession would probably win.

Most Americans are more concerned about the price of eggs, bread and gasoline than they are the cost of French wine or a new BMW, so I’m not sure the rhetoric around tariff inflation will resonate too widely. Perhaps the coming recession can be confined to the DC Metro area.

Tariffs increase cost in the here and now much as any tax increase would. I doubt they cause spiraling Inflation in the long run unless the Fed expands the money supply too much to compensate. More likely consumers buy less, and other downturn effects. Multi-faceted issue some pundits lke to reduce to one bullet point.

As long as Americans have jobs they’ll keep spending, and if their transportation costs and grocery bills are lower they’ll spend more on discretionary items. A question remains which discretionary items, but its a pretty good guess that food and entertainment are in the mix. I’m starting to kick the tires of some restaurant names that might benefit from that trend.

two different parts of the economy. The US is a service economy, so manufactured products need to come from somewhere else, and those will be more expensive from the tariffs.

And evading the tariffs is not easy, because setting up manufacturing domestically takes years to decades to implement.

With the exception of oil, in general commodity prices do not impact the inflation levels of the US because of their inherent volatility. (which is making me nervous, as the buildup on Diego Garcia means that actions in the middle east could occur soon)

When it comes to Iran, even a Superpower can have a glass jaw because the US economy could be crippled literally overnight if the Straits are blocked and oil goes up to 140 to possibly even 200 a barrel, setting an all time record for crude.

It’s going to be an interesting week for sure. You know the old saying, “may you live in interesting times”. It is certainly interesting at the moment.

I follow this site because of the interesting discussion although I personally have no interest in owning preferred stocks. I only invest in IG corporate bonds (mostly BBB+ or better) and only for the income stream, not capital gains.

Last week my portfolio was fractionally up but it was interesting to see that it was fractionally down on Friday even though treasury yields took a decent beating. Generally, when treasury yields fall corporate bonds follow suit. Not the case on Friday. I can only surmise that bond investors are either beginning to question the credit worthiness of some solid companies, selling to raise cash to deploy into equities or booking gains and waiting for a reversal in bond prices. Either way, I’m not swayed. I remain focused on my income stream.

Widening credit spreads between treasuries and corporates is something to keep an eye on. Harbinger of economic weakness ahead. So far it’s minor.

There doesn’t seem to be a correlation at the moment between which of my holdings took a slight loss Friday ( portfolio down .25%) and their IG rating. The 4 positions (out of 75) I hold with a rating of BBB- were all down but so were bonds like Johnson & Johnson (rated AAA) and Proctor and Gamble (rated AA3). I would consider adding not selling if spreads widen further. HF Sinclair took the biggest hit (-2.67%) Friday but even as a BBB- rated issue I might buy more. Low leverage (refinanced in January extending maturities) strong balance sheet, high liquidity, diversified refineries. Coupon is 6.25%, yield to maturity (2035) is 6.65%.

Just curious. For the live sheets, if you are tracking ALL-H, why not also track ALL-I? At the moment, ALL-H has a higher current yield, but couldn’t that change at any moment during the trading day? Same question for RNR-G. In each case, lower yield at the moment, but also higher capital gains potential if interest rates completely crater. (Not a prediction, but a possibility.) And aren’t there other investment grade preferreds that have similar current yields?

Good list. I have bought most of these Thur and Fri. I have an extended list of about 24 that I am shopping for next this week.

Mr Conservative–good for you. I could make a very long list–if was just kind of a quick scan.

Markets are open and off 4-5%.

MGRB CY is 6.89%

Thanks WAF–tweaked the formula so it is now correct. Will show the update in a few minutes.

mgr 7.06%