I recapped my buy of the new Capital Southwest Corporation (CSWC) last week–now for my 2nd buy in this sector (BDCs).

I am buying a 1/2 position of the newer Saratoga Investment (SAR) 8.50% senior notes (SAZ). 5 years to maturity, although 2 years to 1st optional call so one doesn’t want to pay too much above $25 for the issue in case we see sharp rate drops next year.

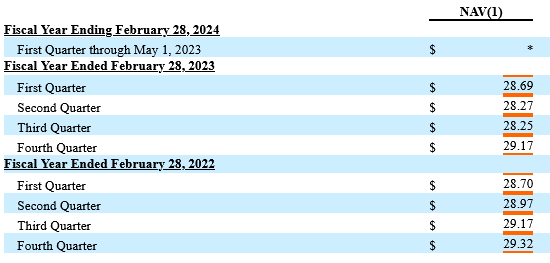

SAR is very similar to CSWC in many ways. They have assets under management of around $1 billion–so a decent sized business development company. Like CSWC they have maintained a relatively flat net asset value/share – always a good sign that they can maintain their NAV.

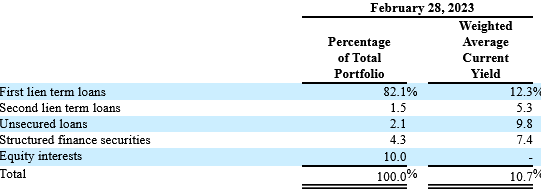

Also like CSWC the company invests primarily in 1st lien debt, although they do have 10% equity interests.

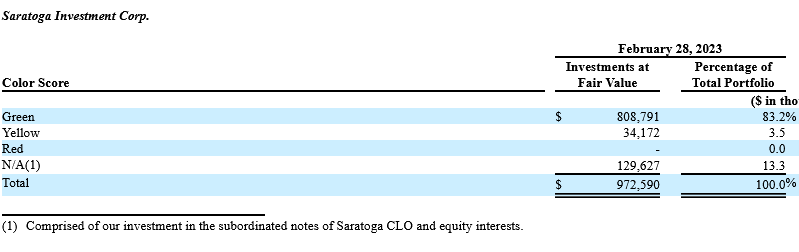

The company self grades their portfolio in colors green, yellow and red–obviously the red is the poorly performing issues of which the company claims to have none.

SAR has been around since 2007–while not as old as CSWC 16 years is ‘middle aged’ for a BDC and certainly they have seen the ups and downs in economic conditions in the U.S. In fact the company had issues in 2008 with a default on some debt–since then they have been straightened around and have performed very well in the last 10 years.

The 10-K (annual report) for the period ending 2/28/2023 can be found here.

Their latest presentation can be found here.

So this gives me 2 buys in the 8% area of what I believe to be 2 of the higher quality business development companies

I expect no capital gains of these issues–just a steady nice interest payment stream.

Former owner of SAR common, sold it on price strength but never got back in. However, replaced it with SAJ/SAY/SAZ (all bought at discounts after those were issued). Big owner of CSWC common, use some options strategies to hedge. Also an owner of RWAYZ, also bought at discount around the issuance period.

Looking at the CSWCZ issue. I suspect we will have a chance to buy below par shortly, so holding fire right now.

Although the future may be different, no BDC has ever defaulted on a bond/baby bond. Common shares can be risky (look up ACAS for an example), so any common shares I buy in the space are the blue chips like MAIN, TSLX. CSWC seems like a mini-MAIN, so willing to go out the risk curve a little.

Very interesting. I used to hold SAR as well. SAZ was my largest baby bond holding (did have SAY), but CSWCZ has now taken first place. A close third is RWAYZ (did have RWAYL). My top five common BDCs in order are TSLX, HTGC, CSWC, RWAY and ARCC.

Have you looked at BSXL? They just raised the dividend 10% yesterday to 77 cents and I believe they have plenty of room to raise it more…. a relatively newer BDC which suffered initially from an overhang of locked up shares being released in the first 8 months after going public… They’re still fundamentally cheap I think………Closed at 26.99 today +2.66%

Its BXSL. I think it is a much safer choice, as nearly all of its loans are first lien, as opposed to many BDCs who have a significant amount of second lien and other securities lower in the capital structure

Ah nuts!!! I typo’d!

No prob. Its surprising that this one has such a low profile in BDC land, given its size and the Blackstone name

You bet. I really like it, and that dividend raise didn’t hurt. My timing on this has been terrible and I keep missing those few and not very deep dips that they had over the last few months. So still watching….

“In fact the company had issues in 2008 with a default on some debt–since then they have been straightened around and have performed very well in the last 10 years.”

Did they pay back their ‘Default’?

Yes. Also the default was under prior management. Saratoga bought the BDC that defaulted and paid back the debt.

Thank-you…So good to hear. I own both BBonds!

Hi PaydayInvestor–I see Landlord and 2wr got it covered below.

Important to note is that although what is now Saratoga has been around since 2007, it did not become Saratoga until 2010 when this management team took over to right the ship. Hence the 2008 defaults etc. were a part of the reason why this team took over.

We commenced operations, at the time known as GSC Investment Corp., on March 23, 2007 and completed an initial public

offering of shares of common stock on March 28, 2007. Prior to July 30, 2010, we were externally managed and advised by GSCP

(NJ), L.P., an entity affiliated with GSC Group, Inc. In connection with the consummation of a recapitalization transaction on

July 30, 2010, as described below we engaged Saratoga Investment Advisors (“SIA”) to replace GSCP (NJ), L.P. as our investment

adviser and changed our name to Saratoga Investment Corp.

As a result of the event of default under a revolving securitized credit facility with Deutsche Bank we previously had in place,

in December 2008 we engaged the investment banking firm of Stifel, Nicolaus & Company to evaluate strategic transaction

opportunities and consider alternatives for us. On April 14, 2010, GSC Investment Corp. entered into a stock purchase agreement

with Saratoga Investment Advisors and certain of its affiliates and an assignment, assumption and novation agreement with

Saratoga Investment Advisors, pursuant to which GSC Investment Corp. assumed certain rights and obligations of Saratoga

Investment Advisors under a debt commitment letter Saratoga Investment Advisors received from Madison Capital Funding LLC,

which indicated Madison Capital Funding’s willingness to provide GSC Investment Corp. with a $40.0 million senior secured

revolving credit facility, subject to the satisfaction of certain terms and conditions. In addition, GSC Investment Corp. and GSCP

(NJ), L.P. entered into a termination and release agreement, to be effective as of the closing of the transaction contemplated by the

stock purchase agreement, pursuant to which GSCP (NJ), L.P., among other things, agreed to waive any and all accrued and unpaid

deferred incentive management fees up to and as of the closing of the transaction contemplated by the stock purchase agreement

but continued to be entitled to receive the base management fees earned through the date of the closing of the transaction

contemplated by the stock purchase agreement

I’ve chosen to be in SAT and SAT rather than the new issue – willing to give up some current yield for better possible appreciation potential in a limited time span. The other thing to know is the greater participation in CLOs that SAR has which I believe comes thru JVs. I’ve followed SAR for 10 years now primarily because the team was born out of my old firm, Dillon Read.

Thanks 2wr!!

Thank you, 2wr. I ran the numbers, an your approach will yield an annualized return of over 8% by maturity, a chunk of which will be capital gains. Wise tactic.

I’ve also started buying some of the newer issues with yields near 8%. I’ve started picking up a few shares of RWAYZ, GAINL, CSWCZ and now SAZ. I’m hoping to see more of these coming to market with similar rates.

mrinprophet–was looking at the gladstone issue and runway growth and will keep them in mind if I add further BDC issues–I just think the risk/reward on Capital Southwest and Saratoga is slightly better.