Records continue to be set in the equity markets–even with a holiday right in the middle of the week. The S&P500 opened the week at 3226 before seeing a low of 3220, but turning higher on Friday and closing at 3240.

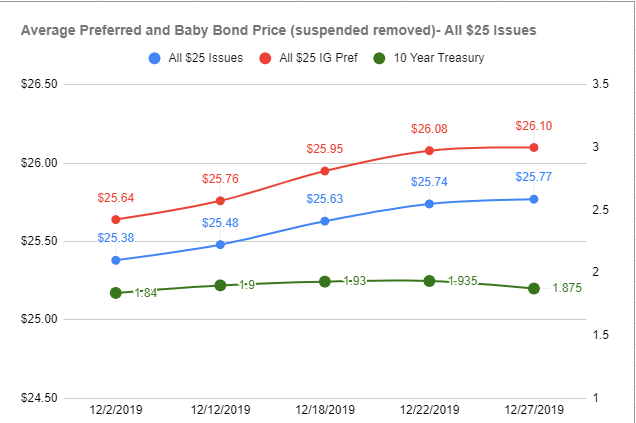

The 10 year treasury seems to have found a fairly “sticky” yield in the last few weeks–in the 1.85% to 1.95% area. Last week it opening at 1.91% before hitting 1.94%, but closed the week at 1.87% as it drifted lower last Friday. With the slow markets last week whether this is meaninfull at all is doubtful. I see that the yield has popped a bit this morning to be at 1.94% now.

The Fed Balance sheet popped again last week as it grew by $28 billion. This gives us total growth during December of an incredible $100 billion of Non quantitative easing (that’s what Powell says anyway).

Last week we didn’t have any new preferreds or baby bonds announced–probably will be the same this week with the holiday right in the middle of the week again.

Below you can see that pricing on shares of preferreds and baby bonds moved the tiniest amount higher for the week. Remember that ex-dividend dates occur during these period and distort the numbers a little, but with a larger sample size the distortions are minimized.