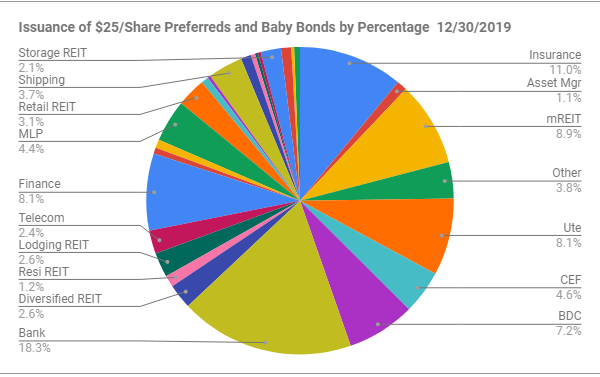

Just a bit of trivia into who issues $25 preferred stocks and baby bonds.

Below is a chart that breaks down the number of issues of $25 issues outstanding.

This is really nothing new for those that have been investing in these issues for years–but maybe newer investors aren’t aware of the breakdown.

This doesn’t show them by dollars–just by individual issues outstanding. The chart shows banks are the largest issuer–and if I listed by dollar value it would show banks are by far and away the biggest issuer since the big banks–i.e. JPMorgan and Bank of America tend to sell issues with 30, 40 or 50 million shares–while REITs etc are more in the 1-10 million area.