Last week was a bit like watching paint dry in equity markets with a trading range in the S&P500 of 4113 to 4169 with a close on Friday that was less than .1% lower than the close the previous Friday. In the olden days (i.e. 30-40 years ago) we would say that there is lots of tension building on the tape–meaning it will break higher or lower in a big way the longer the flat trading continues. Meaningless drivel I think–of course it is going to break sharply higher or lower–and it is likely this is the week we will see that break as many of the big tech companies will be reporting earnings this week–Microsoft, Alphabet, Meta, Amazon and Intel are all reporting. We’ll see.

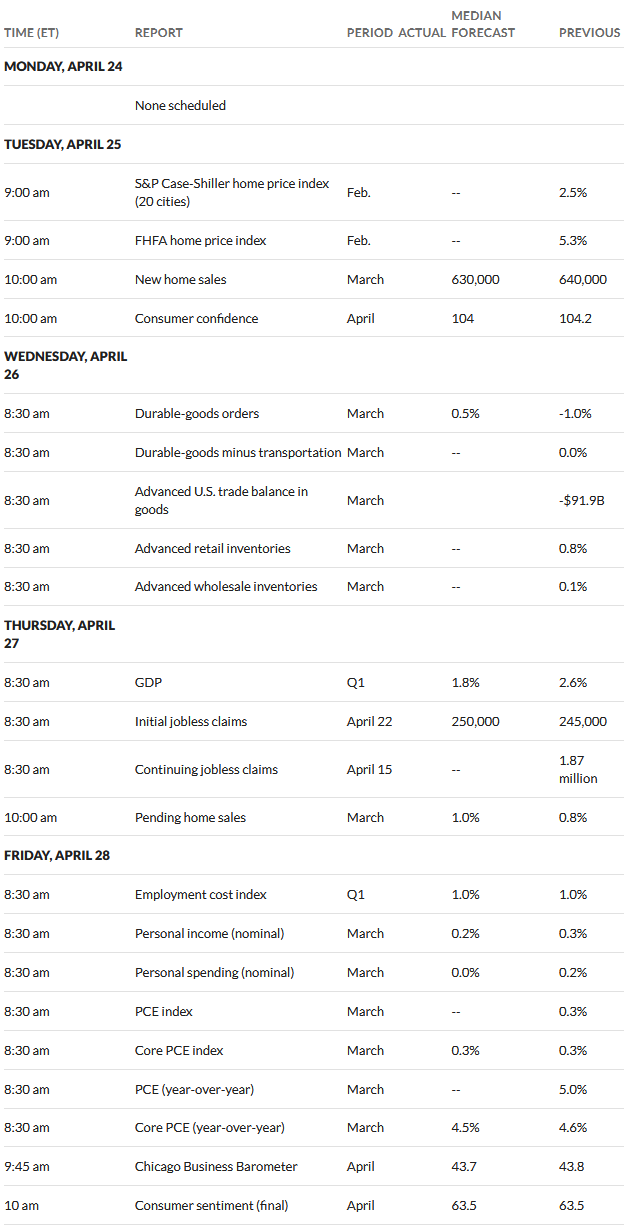

The 10 year treasury yield closed the week at 3.57%–5 basis points higher than the close the previous Friday—darned near as quiet as the equity markets. Economic news continues to be mixed–some soft and some hot. It is likely we will see mixed economic news this week in the run-up to the FOMC meeting starting next Tuesday. This week we have 1st quarter GDP being announced Thursday and then the important PCE (personal consumption expenditures index) being announced Friday. The PCE index will be the final important data point prior to the potential Fed Funds rate hike on Wednesday 5/3/2023

The Fed balance sheet fell by $21 billion last week after falling $18 billion the previous week–now at $8.59 trillion which is up about $250 billion from the low point on 3/8/2023, but below the high on 3/22/2033 which was because of the banking crisis and Fed lending programs to banks.

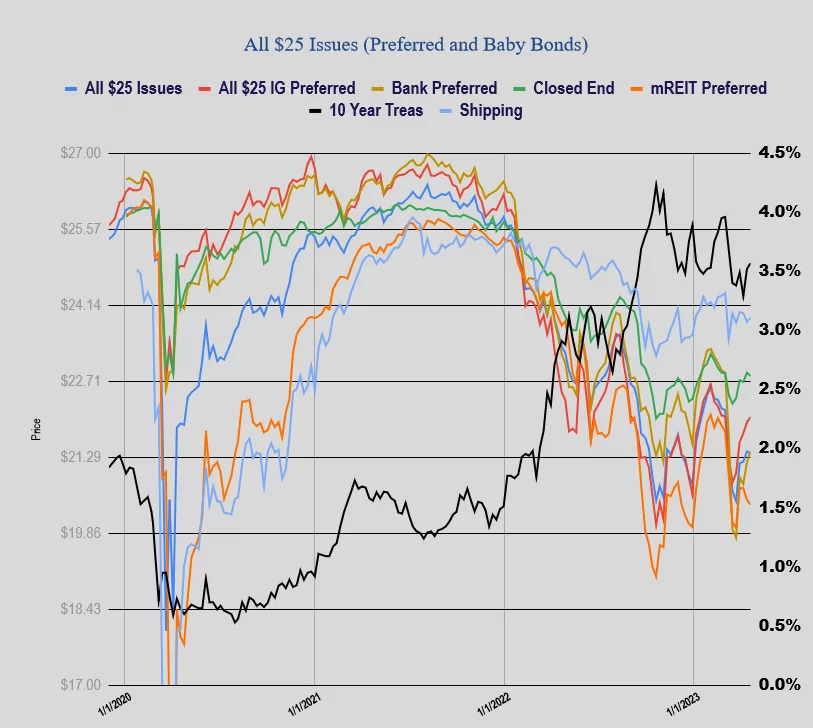

As might be expected the average $25/share preferred stock and baby bond moved very little last week. The average share fell 2 cents, with investment grades issues gaining 10 cents, banks up 14 cents, mREITs falling 9 cents and CEF preferreds off 6 cents.

Last week we had no new income issues priced.

FRC reports today. That should be interesting.